Michael Rondel

Audit & Assurance Partner

IFRS 15 Revenue from Contracts with Customers fundamentally changes the financial reporting landscape for how entities recognise revenue.

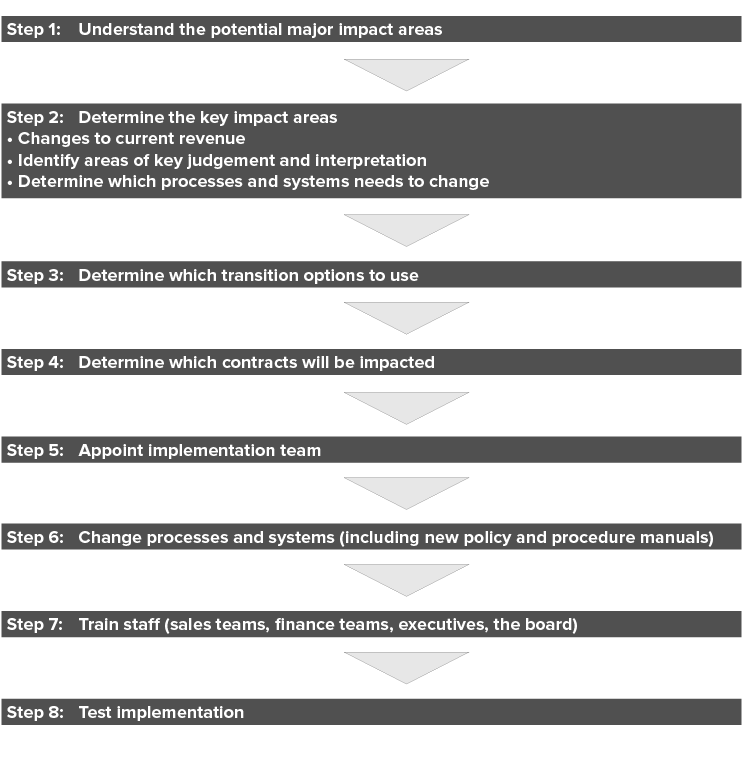

Most entities will face significant challenges when they prepare their financial statements using this new accounting standard. The changes can be complex and can have effects beyond just the accounting treatment. When adopting IFRS 15, including deciding which transition route to apply, entities need to consider both the commercial impacts on their business as well as any changes that need to be made to business processes and accounting systems.

Our IFRS 15 experts can help you determine the impact of the new standard on your reported earnings.

As a guide the heat map below considers the relative level of impact and complexity when adopting IFRS 15.

| Red denotes a high level of potential impact and complexity. |

| Amber denotes a medium level of potential impact and complexity. |

| Dark teal denotes a low level of potential impact and complexity. |

Industry | Scope | Step 1 | Step 2 | Step 3 | Step 4 | Step 5 |

Retail | | | | | | |

FMCG | | | | | | |

Software | | | | | | |

Telcos | | | | | | |

Licensors | | | | | | |

Building and construction | | | | | | |

Residential real estate construction | | | | | | |

Manufacturing | | | | | | |

Mining | | | | | | |

Professional Services | | | | | | |

More information on IFRS 15 can be found under Accounting Standards Training and IFRS Publications.

The effect of adopting the new revenue standard raises many questions such as:

Michael Rondel

Natalie Tyndall

James Lindsay