Kimberley Symon

Advisory Partner

Kia ora and welcome to the ninth BDO Business Performance Index (BPI) report. This six-monthly report shares the latest survey insights from New Zealand business leaders, summarises the leading issues impacting business performance, and provides practical business tips to help you navigate the months ahead.

In addition to the insights on this page, this edition also features a dedicated section exploring sector insights for business leaders operating across a range of key industry groups; from agribusiness and construction to retailing and tourism.

In many cases, the challenges encountered within your business are often shared by others in your industry. We encourage you to consider the insights and recommendations outlined in the report and how you can use them to navigate the path ahead.

Our latest report is based on a nationwide survey of 537 business leaders during April 2026. In the lead up to the Government’s annual Budget unveiling on 28 May, the report provides timely insights on the big issues facing business leaders now, and over the coming six months as we head into the NZ General Election (7 November 2026).

The April 2026 BPI survey highlights that more businesses are showing signs of improved underlying financial resilience, but their overall business performance positivity remains weighed down by economic and political uncertainty - handbraking potential near-term growth and investment. |

We invited a panel of experts to discuss the findings in our latest report and share practical tips for business leaders, along with insights into ways the Government might respond to the topical issues; both in this year’s Budget and in their Election policies.

Watch the video below featuring an interview with Kimberley Symon, BDO Advisory Partner, Alan Scott, BDO Tax Partner and Jason Shoebridge, NZIER Chief Executive.

Kiwi business leaders are facing daily uncertainty – impacted by global conflict, fuel price inflation, fluctuating economic fortunes and advancing AI. In this dynamic context, it’s no surprise that the issues which NZ business leaders face today look different to when our last BPI survey was undertaken in September 2025. Notably, the onset of war in Iran from late February 2026 has shaped much of our current macroeconomic landscape

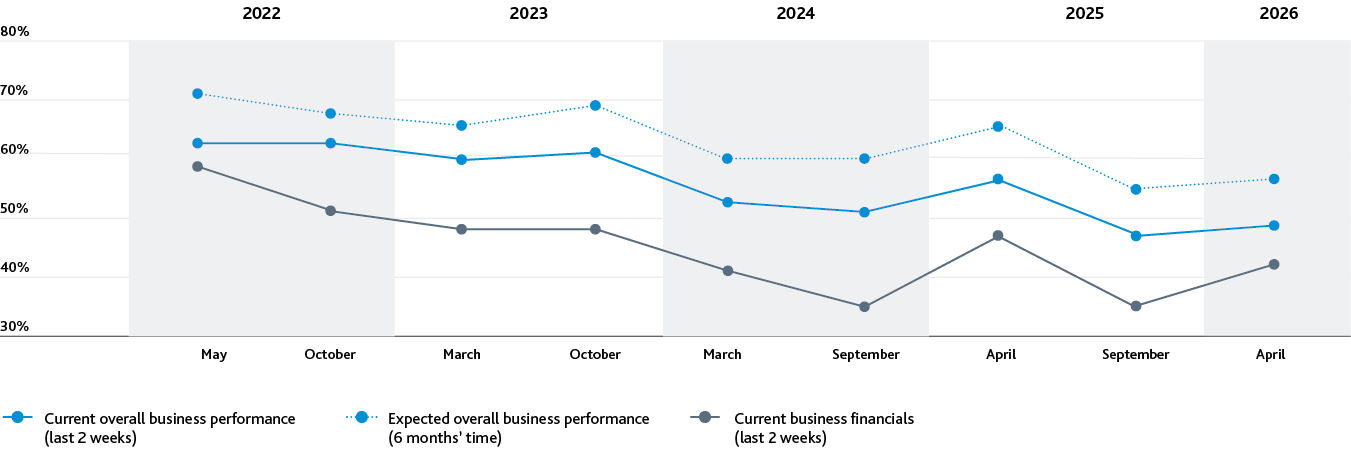

Despite this changing context, overall business performance sentiment among NZ business leaders remains at similar levels to our September 2025 BPI survey, sitting only one percent higher than the record low at that time – with 49% of business leaders feeling positive (all or most of the time) regarding their overall business performance in the past 2 weeks. Expectations for the next six months also remain subdued, with 57% expecting to feel positive about their overall business performance in the next 6 months, lifting only 1% since September.

Looking beyond overall business performance however, the differences between six-monthly survey insights, industries, markets and regions become clearer - highlighting that for many business leaders, their priority issues and outlook has changed.

“The latest BPI survey findings suggest some businesses are starting to see early signs of financial resilience after several difficult years, but market conditions remain fragile and the international macroeconomic environment is still highly uncertain. Business conditions are moving at different speeds across regions and market segments, with business performance, investment and hiring intentions closely tied to economic exposure, inflationary impacts and industry mix.” – Kimberley Symon, BDO Advisory Partner

% Business leaders feeling positive (all or most of the time)

Some positive news comes when looking specifically at current business financial performance – with 7% more business leaders feeling positive about this than in September (42% in April 2026 vs 35% in September 2025). This is only the second time an improvement in this measure has been recorded. In fact, current financial performance (the third lowest ranking issue in September) now sits just outside of the five lowest-scoring issues for business leaders, indicating a growing degree of resilience for some – during the short term at least – in navigating inflationary pressures driven by rising global fuel prices.

Auckland business leaders are most positive about their current financial performance (57%), higher than those in the rest of the North Island (39%) and South Island (18%). Agribusiness and Māori business leaders are most positive about their current financial performance (both 54%).

Business leaders are even more positive when looking ahead six months, with 49% nationally expecting to feel positive regarding their business financial performance.

Further encouraging news comes when looking at business growth. 57% of business leaders expect to be positive about their business growth in six months’ time, significantly higher than at present (42%), and higher than any other business performance attribute. This optimism regarding business growth is also notably higher than recorded in September (46%).

“Business leaders have had to make a large number of tough calls in the last few years. What we’re seeing now is a growing group of New Zealand business leaders who are learning to operate in an environment of continued uncertainty, by planning ahead, watching cash flow acutely, and building teams that can adapt.” – Rees Logan, BDO Business Restructuring National Leader

Further reflecting the uncertain business context, external economic (27%) and political factors (28%) are now the two business performance measures which business leaders currently feel least positive about, among the 19 attributes surveyed. Positivity with external political factors has declined 7% since September, now ranking second lowest (previously fourth lowest) – likely influenced by the war in Iran, persistent inflation and an uncertain policy climate in the face of New Zealand’s upcoming General Election.

On top of these external headwinds, businesses are grappling with tight cash flow, supply chain disruptions, and soft sales pipelines. Fewer than two in five leaders are positive about their cash flow position or supply chain reliability, and a similarly low share are optimistic about future bookings and demand.

% Businesss leaders feeling positive all or most of the time (last 2 weeks).

To view all of the issues facing business leaders click here.

Looking ahead 6 months, business leaders expect to continue feeling least positive about economic and political issues, followed by cash flow. However, labour supply and cyber risk emerge are expected to move into their five lowest-scoring issues.

“The geopolitical uncertainty and flow on economic impacts have resulted in businesses feeling uncertain about future demand and cost pressures currently. This has reversed the lift in confidence reported at the start of the year. Given these concerns, it is not surprising to see businesses report in the BPI that their biggest concerns are the economy, political factors and their cash flows.” –Jason Shoebridge, Chief Executive NZIER

A range of topical factors stand out as top-of-mind for business leaders in successfully navigating our economic landscape over the year ahead. Together, these provide a clearer picture of how businesses are balancing cost pressure, financial risk and investment decisions as economic conditions remain challenging.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to

meet financial obligations

or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

We take a closer look at these issues in the sections below.

The April BPI survey highlights uneven business performance across regions and markets in New Zealand.

% Business leaders feeling positive all or most of the time (last 2 weeks)

Mid-market businesses are holding up better than small businesses, with their added scale offering a further buffer against rising costs and tighter margins. 61% are positive about their overall business performance and 39% expect net profit margins to lift over the next 12 months, compared to 29% among all businesses nationally. 48% of mid-market business leaders are currently positive about their business growth, compared to 42% among all businesses and 31% expect to be actively hiring staff in the coming year, compared to 17% among all businesses. Fewer report they are likely to be unable to meet financial obligations, or become insolvent, in the next 12 months. Labour supply and workload are currently in their top five issues.

| All Businesses | Mid-Market | Auckland | Rest of North Island | South Island | |||||

|---|---|---|---|---|---|---|---|---|---|

| Economic factors | 27% | Economic factors | 31% | Economic factors | 34% | Economic factors | 26% | Political factors | 7% |

| Political factors | 28% | Political factors | 35% | Political factors | 40% | Political factors | 26% | Cash flow | 12% |

| Cash flow | 37% | Supply chains | 40% | Supply chains | 47% | Business pipeline | 34% | Economic factors | 13% |

| Supply chains | 39% | Workload | 40% | Cash flow | 47% | Labour supply | 35% | Financial performance | 18% |

| Business pipeline | 40% | Labour supply | 41% | Business pipeline | 48% | Supply chains | 37% | Supply chains | 25% |

Lowest scoring business performance attributes (% of leaders feeling positive in last 2 weeks)

Auckland businesses are generally more positive about their overall business performance (56%), future business performance (62%) and current finances (57%) than other regions, potentially driven by their proximity to markets, supply chains and transport links. 51% are currently positive about their business growth, higher than any other region (38% among business leaders in the rest of the North Island and 35% in the South Island). Only 5% of Auckland businesses reported that they were very likely to be unable to meet financial obligations or become insolvent in the next 12 months – lower than reported nationally (22%) or in any other region.

“The latest BPI shows that Auckland businesses are weathering current economic uncertainty better than most. Leaders here are more positive about overall performance, future outlook and finances, with stronger positivity around growth and a lower risk of insolvency than any other region. Proximity to customers, ports and transport infrastructure appears to be helping Auckland firms manage supply chain pressure and adapt more quickly, including lifting confidence around technology and AI adoption. That resilience reflects both scale and connectivity, but it does not make these businesses immune. Cost pressures, fuel price inflation and political uncertainty are still front of mind, which means Auckland leaders are staying tightly focused on cash flow, scenario planning and building flexibility for the months ahead.” – Andrew Bathgate, Advisory Partner, BDO Auckland

Businesses in the rest of the North Island continue to face a more challenging operating environment than Auckland, with confidence sitting below the national average across performance, financials and future outlook. Fewer than half (44%) of business leaders in this region report feeling positive about their current overall business performance - a 13% decline since September, and the only region to track down. Concerns around cash flow, supply chains and future demand remain prominent. Looking ahead, while sentiment about future overall business performance improves (55%), the focus for many seems to be focused on resilience rather than growth.

“Businesses across the country are navigating a tougher trading environment, and our latest BPI results show margins and profitability remain under pressure. As a major population centre, Wellington has an influence on the rest of North Island responses. Changes in public sector employment and government spending can flow quickly through confidence and demand, particularly for professional services, supply chains, and client-facing businesses. Outside the capital, many regional centres are also feeling the strain, whether through softer demand, higher operating costs, or tighter labour availability. In this environment, the fundamentals matter more than ever. We are encouraging leaders to stay close to their key financial metrics, stress-test multiple scenarios rather than just one static budget, and make deliberate decisions about targeting new customers and retaining existing, capability including AI readiness, and seeking value from their overhead cost base so they can remain resilient over the months ahead.” – Justin Martin, BDO National Advisory Leader

South Island business leaders are currently least positive regarding political, economic and financial factors, with positivity notably low across current financial performance, cash flow and external economic and political conditions. Despite this, a higher share of South Island business leaders (37%) expect their net profit margins to improve over the next year compared with other regions, suggesting active cost control, restructuring and repricing strategies may be underway. Recruitment activity over the past six months has also been relatively strong, suggesting that some businesses are positioning themselves for recovery. While the near-term environment remains difficult, these signals point to cautious optimism and preparation for an eventual lift in conditions.

"Despite softer business performance positivity, more South Island business leaders expect net profit margins to improve over the next 12 months, suggesting many are actively adjusting cost structures and positioning themselves for a lift in conditions. For these businesses, the focus is firmly on managing cash flow, controlling risk and preparing for recovery, rather than chasing growth before demand stabilises.” – Kimberley Symon, Advisory Partner, BDO Christchurch

| All Businesses | Mid-Market | Auckland | Rest of North Island | South Island | |

|---|---|---|---|---|---|

| Current overall business performance (last 2 weeks) | 49% | 61% | 56% | 44% | 44% |

| Current overall business performance (6 months' time) | 57% | 58% | 62% | 55% | 50% |

| Current business financials (last 2 weeks) | 42% | 49% | 57% | 39% | 18% |

| Expected net profit margin (next 12 months) – significantly/slightly higher | 29% | 39% | 26% | 28% | 37% |

| Expected impact of fuel price inflation (next 12 months) – significant/moderate | 64% | 73% | 62% | 66% | 67% |

Very likely to be unable to meet financial obligations or experience insolvency (next 12 months) | 7% | 2% | 5% | 8% | 8% |

| Recruitment intentions (next 12 months) – actively hiring | 17% | 31% | 14% | 18% | 21% |

Mid-market includes businesses with $5M+ average annual revenue (last 3 years) and 20+ full-time employees

Early commentary ahead of Budget 2026 suggests the Government is walking a fine line between fiscal restraint and the need to invest in essential infrastructure. While ministers have pointed to a sizeable capital allowance in the coming Budget, there has been little clarity to date on exactly where that funding will be directed. The emphasis appears to be on core public assets and long‑term needs, including hospitals, schools, transport and other nationally significant infrastructure, rather than widespread new spending initiatives.

“Budget 2026 is shaping up as a fiscally constrained Budget, with the Government clearly focused on getting back to surplus by 2028/29. For businesses, that likely means fewer bold spending initiatives and more emphasis on setting the economy up for longer‑term success. Clear signals around infrastructure investment and lifting productivity would be welcome, particularly given ongoing global uncertainty and domestic cost pressures.” – Alan Scott, BDO Tax Partner

For businesses, this points to a Budget that prioritises discipline and long‑term planning over short‑term stimulus. The lack of detail reinforces that Budget 2026 is likely to be about setting direction rather than delivering immediate relief. Clearer infrastructure pipelines and a focus on productivity‑enhancing investment could support confidence over time, but with public finances under pressure, businesses should expect targeted decisions rather than bold, broad‑based measures.

“NZIER’s expectation is that we will see inflation increase and economic growth slow. There is however considerable uncertainty about the size of these impacts given the uncertainty that exists on how long the fuel crisis continues and the price of oil. In late April, Treasury produced three scenarios based on different conflict durations and different oil prices. Their best-case scenario was the conflict was relatively limited in duration and oil would average $110 per barrel. Under this scenario inflation reaches 3.9%, growth slows to 2% per annum and unemployment remains at 5.3%. These compare with a prolonged conflict and oil hitting $180 a barrel where inflation climbs to 7.4%, economic growth falls to 0.8% and unemployment grows to 6.6% by next year. NZIER’s next forecast will be published at the start of June but our preliminary forecasts are closer to Treasury’s best-case scenario. We will also get Treasury’s latest view when the budget is released on May 28.” – Jason Shoebridge, Chief Executive, NZIER

“BDO’s Business Performance Index (BPI) reveals a picture of relatively weak confidence in the future prospects for the economy, although businesses still expect the economy to improve over the next 12 months. It also shows confidence at similar levels to the last release of the BPI in October. This is consistent with both NZIER’s forecasts for the New Zealand economy and the findings of its most recent Quarterly Survey of Business Opinion (QSBO).

NZIER believes the fuel crisis will reduce economic growth this year and increase inflation. The QSBO found that the proportion of firms that reported facing higher costs remained steady at 37%, while the proportion of firms that reported they had raised prices picked up to a net 22 percent in the quarter. The details of the survey suggest weak demand is limiting the ability of firm to pass on cost increases, particularly in the construction sector. It is significant in this regard that the BPI shows that 64% of respondents expect fuel price inflation to have a moderate or significant impact on their net profit margins, which indicates that most businesses do not feel they can pass on the impacts of these cost increases at least in their entirety. This is also reflected in only 29% of respondents to the BPI saying they expect higher profit margins in the next 12 months.

The Reserve Bank indicated in its April Monetary Policy Review that it is mindful of inflationary pressures from global supply chain disruptions and fuel price shocks as a result of the Iran conflict. Prior to the conflict NZIER was expecting the Reserve Bank to start tightening monetary policy in July with a 25 basis point OCR increase. We still expect this to be the case.

With rising costs, higher interest rates and the expectation of weaker demand, it is not surprising that respondents are rating external economic factors as their biggest concern in the BPI, followed by their cash flow being their third biggest business concern.

An interesting finding in the BPI is that labour supply is in the top five business concerns of respondents in the next six months, despite what appears to be weakening demand and the potential for unemployment to rise. This is consistent with what businesses told us in the QSBO. A net 9% of businesses reduced headcount in the March quarter but businesses are finding it more difficult to hire skilled workers. Businesses report it has become easier to hire unskilled workers, however.

In summary, the geopolitical uncertainty and flow on economic impacts have resulted in businesses feeling uncertain about future demand and cost pressures currently. This has reversed the lift in confidence reported at the start of the year. Given these concerns, it is not surprising to see businesses report in the BPI that their biggest concerns are the economy, political factors and their cash flows.”