Clearly, inflationary pressure is already taking its toll on some sectors and markets before others. Construction and retail business owners are currently feeling the pressure most acutely, with cost-of living inflation and softer consumer demand undoubtedly squeezing margins. 40% of business leaders in these sectors are positive about their overall business performance - the lowest across New Zealand’s major sectors and a notable decline since the September 2025 survey.

% Business leaders feeling positive in last 2 weeks (all or most of the time)

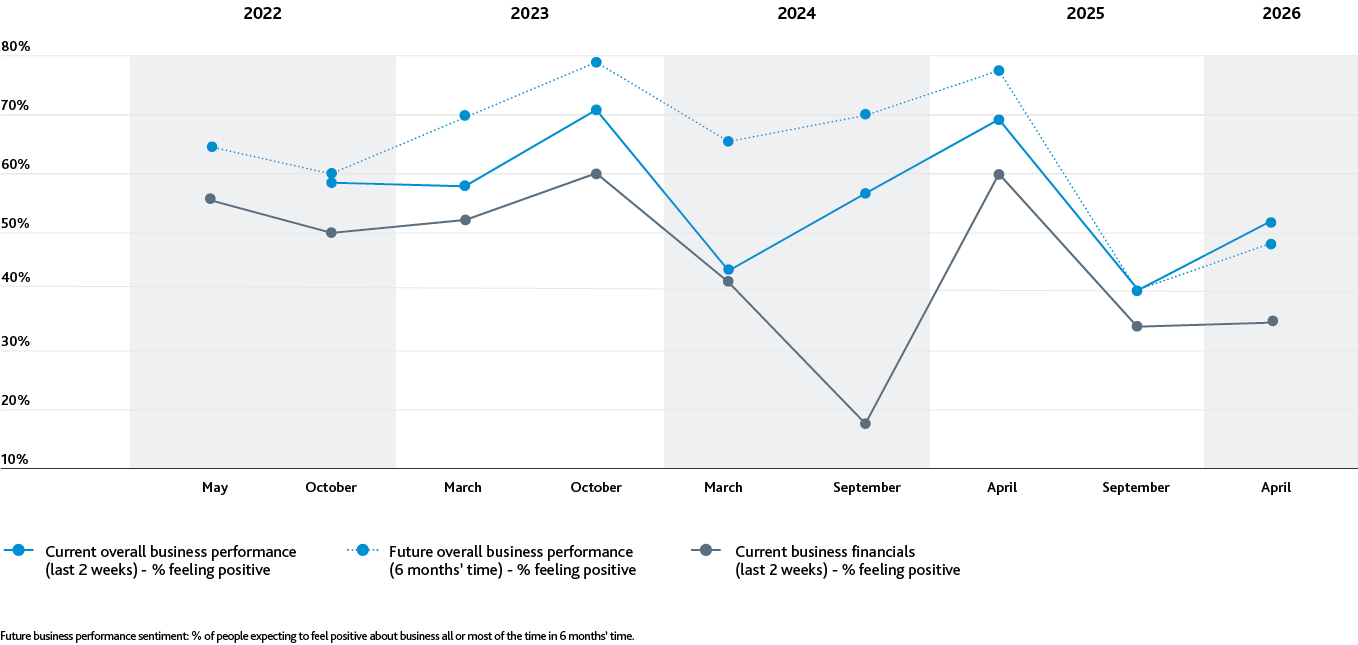

After a record fall in overall business performance sentiment in September, tourism business leaders’ current positivity has rebounded 12% in April, now at 52%. This may be influenced by a seasonal lift in business over the summer period, prior to global fuel price inflation from March.

Current overall business performance (% feeling positive, last 2 weeks) | Future overall business performance (% feeling positive, 6 months’ time) | Current business financials (% feeling positive, last 2 weeks) | |

|---|---|---|---|

| Agribusiness | 80% | 83% | 54% |

| Construction | 40% | 48% | 42% |

| Not-for-profit | 55% | 39% | 40% |

| Māori business | 77% | 71% | 54% |

| Retail | 40% | 65% | 19% |

| Technology | 48% | 51% | 49% |

| Tourism | 52% | 48% | 36% |

Retail (19%), tourism (36%) and construction (42%) business leaders are least positive about their current business financials. 19% of construction business leaders and 3% or retail business leaders report that they are very likely to not being able to meet financial obligations, or become insolvent, in the next 12 months.

Meanwhile, Agribusiness (80%) and Māori businesses leaders (77%) continue to show most positivity about their business performance, supported by stronger export conditions for agricultural products including dairy, benefitting their rural communities.

We unpack further insights specific to each key sector from our April BPI survey in the sections below.

This year, the Business Performance Index introduced a new set of forward‑looking measures to better understand how business leaders are approaching the next six to twelve months.

Together, these measures provide a clearer picture of how businesses are balancing cost pressure, financial risk and investment decisions as economic conditions remain challenging.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to

meet financial obligations

or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

The results above for all businesses establish a national baseline, before the sector breakdown below highlights where pressures and opportunities are most concentrated across industries.

| Expect net profit margins to improve (slightly and significantly higher) | Expect fuel prices to impact net profit margins (significant and moderate impact) | Very likely to be unable to meet financial obligations or become insolvent | Recruitment intentions (% actively hiring) | Expect to feel positive about leveraging new tech & AI (% expecting to feel positive all or most of the time) | |

|---|---|---|---|---|---|

| Agribusiness | 17% | 56% | 0% | 6% | 47% |

| Construction | 31% | 87% | 19% | 25% | 48% |

| Not-for-profit* | NA | NA | NA | NA | 73% |

| Māori business | 44% | 73% | 1% | 28% | 68% |

| Retail | 33% | 63% | 3% | 20% | 49% |

| Technology | 33% | 55% | 0% | 26% | 45% |

| Tourism | 31% | 63% | 1% | 32% | 37% |

*Further data for Not-for-Profit sector unavailable due to sample size.

When we look at the current business financials, retail business owners are already feeling the brunt of the ongoing cost-of-living crisis and now fuel pressures, with just 19% reporting that they are feeling positive about their current business financials.

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

Alongside Agribusiness leaders, Māori business sector leaders (54%) are the most positive about their current financials, with their continued correlation likely due to their connection to aligned industries and regional economies often vested in agriculture, horticulture, fisheries and forestry.

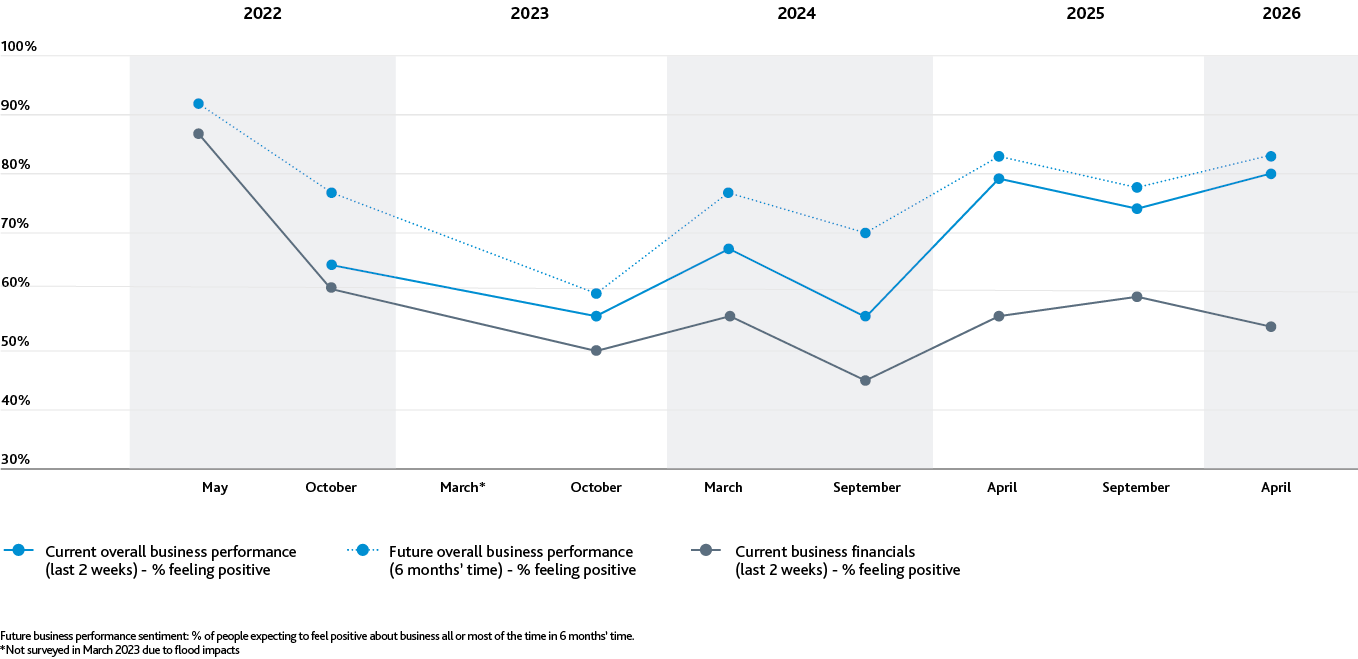

After several challenging years, agribusiness leaders are now more positive about their current business performance, likely buoyed by improved commodity prices and a favourable export climate. Approximately three-quarters felt positive in late 2025, already the strongest of any sector, and the April 2026 data shows further gains on that level.

Compared to May 2025 (when sentiment was recovering post-drought) agribusiness business performance optimism has climbed even higher, reflecting sustained farmgate returns, a lower NZ dollar, and easing interest rates.

“While rising input costs and margin pressure remain real challenges, many operators are continuing to perform, adapt and make practical decisions that support long‑term sustainability. There’s a strong focus on managing cash flow, controlling costs and investing where it makes sense, which reflects a sector that is resilient, grounded and looking ahead with measured optimism rather than complacency.” – Dallas Peters, BDO National Agribusiness Sector Leader

While rising on-farm costs like fuel and fertiliser remain a watch point, overall agribusiness is on an upswing, marking a clear improvement on both six months and one year ago. Compared with most other sectors, fewer agribusiness leaders anticipate fuel price inflation will have a sizeable impact on net profit margins over the next 12 months, which may indicate greater margin resilience due to recent returns. More than 8,000 farmers, who are shareholder-suppliers to the Fonterra co-operative, benefited from a recent $3.2 billion capital return and payout in April 2026, resulting from the sale of its Mainland Group business.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

While returns have been strong of late for agribusiness leaders, off the back of stronger commodity prices for dairy, sheep and beef, fewer are expecting net profit margins to significantly increase over the next 12 months. This suggests they either feel commodity prices are peaking or beginning to be offset by other aspects of inflation such as rising fuel costs.

“The relative positivity shown by the agribusiness sector reflects the high commodity prices that many in this sector are receiving for their products. Given the high proportion of primary sector production that is exported, a relatively weak New Zealand dollar will also increase their New Zealand dollar returns. It is however interesting that agribusiness is the sector that is least likely to think that fuel price inflation will have at least a moderate impact on their business, although in absolute terms 56% of agribusiness still expect it to have an impact. Respondents in the agribusiness sector are the least confident that they can improve their margins over the next twelve months. This indicates that they may be expecting commodity price reduction over the next twelve months.” – Jason Shoebridge, Chief Executive, NZIER

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

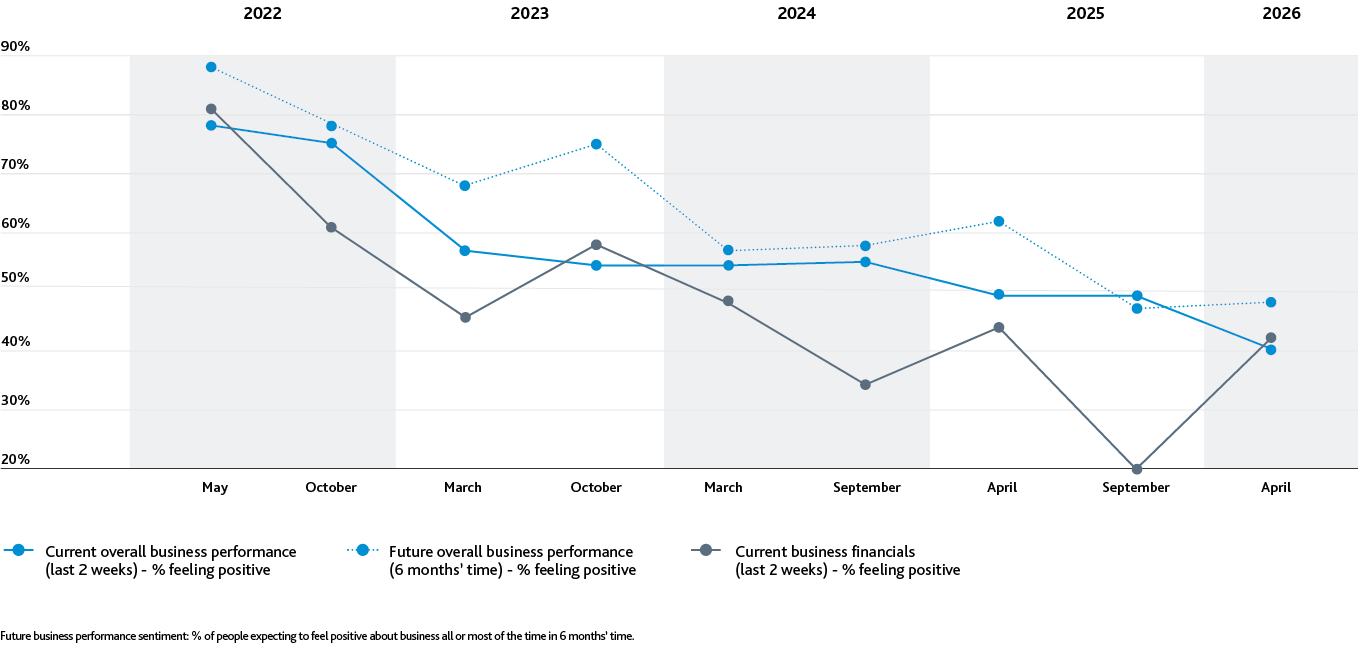

Only around 40% of construction business leaders now feel positive about overall business performance, down from 49% in Oct 2025 – and now the least optimistic sector surveyed.

Stagnant pipelines, a soft housing market, and tight margins have heavily impacted construction business owners.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to meet financial obligations or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

Financial strain in the sector is acute, with 19% of construction business leaders reporting that they are very likely to be unable to meet financial obligations or potentially become insolvent in the next 12 months. This is significantly higher than any other sector.

“Cost pressure, margin tightness and labour challenges remain real for the construction sector, we can see that many leaders are adapting by focusing on delivery discipline, protecting cash flow and strengthening core capability. Rather than pulling back completely, they are being pragmatic – prioritising the work they know they can deliver well and making measured decisions that support longer‑term sustainability.” – Nick Innes-Jones, BDO National Construction Sector Leader

While fewer construction business leaders are feeling positive about their current overall business performance, twice as many are feeling positive about their current business financials when compared to our previous survey in September 2025 (42% vs. 20%). This indicates that issues beyond their immediate financial performance are of concern, including economic and political factors, supply chains and business pipeline.

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

“The BPI shows that confidence in the construction sector continues to be low which is consistent with what the QSBO is showing. NZIER’s QSBO shows that a net 28% of building sector firms expect a deterioration in economic conditions over the next 12 months, which is a sharp turnaround from the net 54% of firms that were feeling optimistic in the previous quarter. A net 73% of building sector firms reported higher costs in the last quarter while a quarter of building sector firms cut prices. The BPI provides some useful context to this result with 87% of construction firms expecting fuel price inflation to have a moderate or significant impact in the next 12 months.” – Jason Shoebridge, Chief Executive, NZIER

Our 2025 BDO Construction Sector Report highlighted some distinct variation in business performance sentiment across key regions and markets. We look forward to sharing more detailed insights into New Zealand’s construction sector in our upcoming 2026 BDO Construction Sector Report, which also includes observations from BDO’s Construction specialists and practical tips for business leaders.

“Māori businesses are standing out for their positivity with adapting to change, particularly when it comes to technology and new ways of working. While cost pressures and margin challenges remain, the outlook reflects a pragmatic, long‑term approach – focused on sustainability, capability‑building and making measured decisions that support resilience in a challenging environment. That said, SMEs, particularly in the regions, have taken a real hit - and those with limited capital and resources are under the most pressure.” – Solomon Dalton, BDO National Māori Business Sector Leader

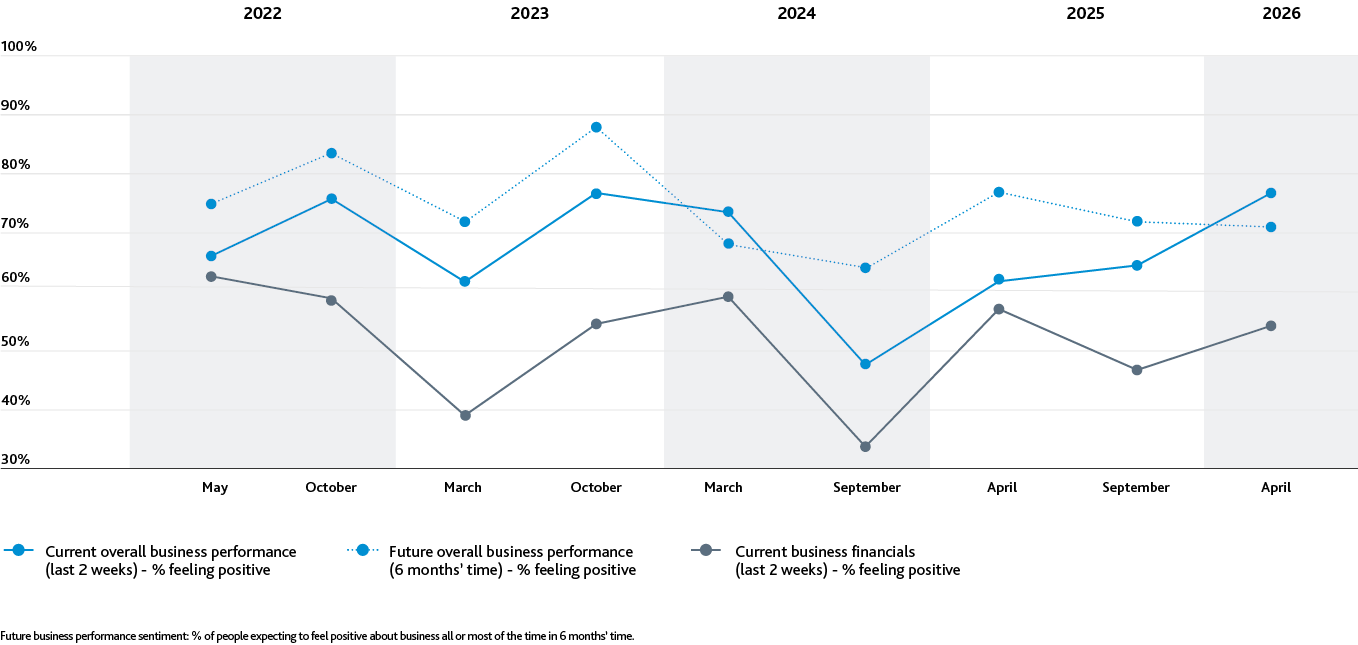

In our September 2025 BPI survey, 64% of Māori business leaders felt positive about their overall business performance, one of the most optimistic across all sectors. The latest results highlight their optimism has risen further to 77%, approaching the highs seen among agribusiness leaders. This trend marks a sizeable upswing versus their low point recorded in September 2024, when their positivity had dipped amid widespread economic challenges.

Many Māori enterprises are tied to agribusiness (along with the rural communities they are invested in) and export markets, so it’s likely that stronger commodity revenues and regional economies have lifted their outlook. Māori businesses still feel that there’s growth in net profit to come in the next 12 months, likely due to expected flow-on spending from farm business leaders in the rural communities where they're based.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to meet financial obligations or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

Businesses in this sector report some of the highest levels of positivity about their ability to leverage and adapt to new technologies, including AI, over the next six months.

However, there is uncertainty on the horizon with regards to fuel inflation. Second only to construction business leaders, more Māori business leaders are expecting a significant impact on their net profit margins due to fuel price inflation in the next 12 months. This is likely tied to the added transportation requirements for businesses operating in rural and regional communities.

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

Leaders are reporting that they feel most concerned about external political factors that impact their business, like local and international elections, government policy direction, geopolitics and global trade dynamics.

55% of not-for-profit leaders are reporting positivity with their current overall business performance (in the past two weeks), up 11% when compared to our September 2025 survey. However, looking ahead to the next six months, there is a noticeable decline in positivity. Current business financial performance sentiment has also declined, signalling emerging pressure on financial sustainability.

Encouragingly, many not-for-profit leaders remain optimistic about technology and leveraging AI, likely reflecting a continued focus on doing more with limited resources.

“While cost pressures and funding uncertainty remain front of mind, the sector continues to show strong operational resilience. Organisations are continuing to deliver impact, supported by highly engaged teams and a strong compliance discipline, but workload, financial positivity, cash flow and growth opportunities remain key pressure points. Increasingly, leaders are focused on strengthening capability in existing teams, particularly around technology and risk, to ensure they can sustainably deliver on their mission.” – Vanessa Rowe, BDO National Not-for-Profit Sector Leader

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

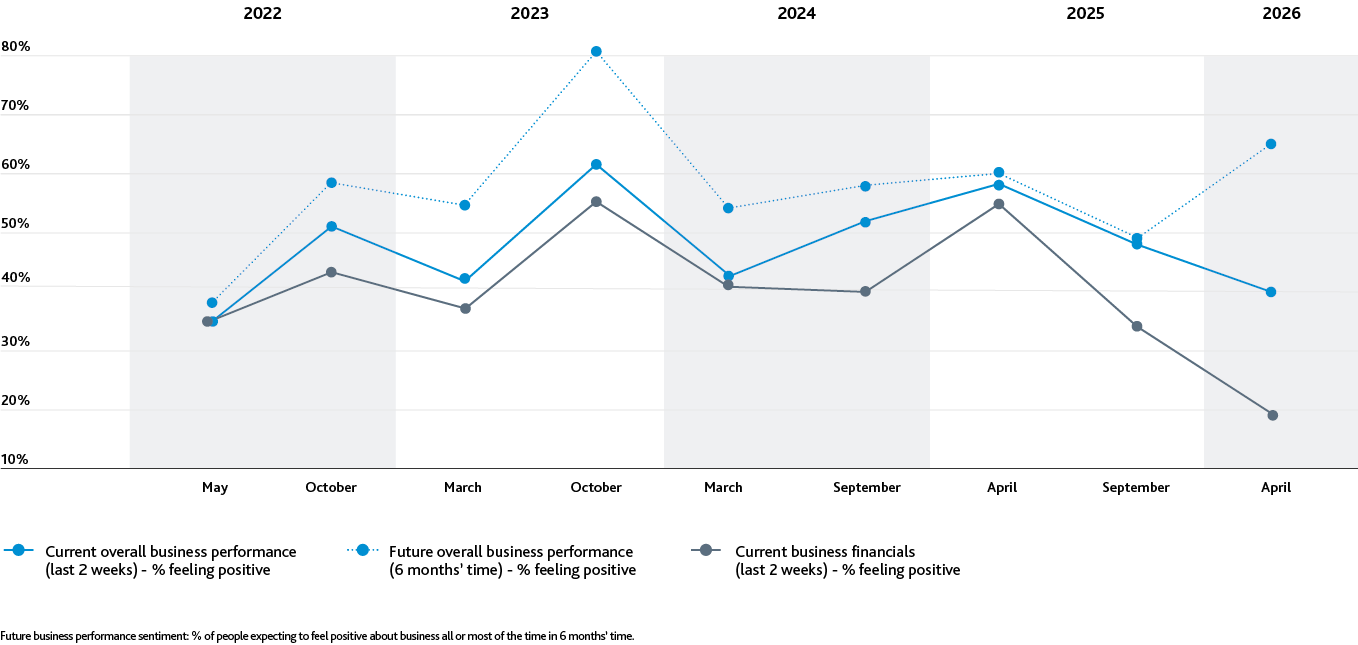

Just 40% of retail business leaders reported feeling positive about their current business performance in the April BPI survey, down from 48% in September 2025. That September figure was down sharply from around 58% in May 2025, reflecting the hit from rising costs and weak consumer spending.

Cost-of-living inflation and soft consumer demand continue to squeeze retail margins. Many retailers note that shoppers are price-sensitive and buying less, which keeps optimism in check.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to meet financial obligations or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

There has been a sharp drop-off in current business financial performance sentiment among retail business leaders since our last six-monthly survey, with only 19% of business leaders feeling positive about this - the lowest of all sectors reported. Additionally, 3% businesses in this sector reported that they are very likely to be unable to meet financial obligations or become insolvent in the next 12 months.

“The BPI also shows that there has been a turnaround in future outlook in the retail sector between October 2025 and April 2026. The QSBO shows that although retailers continue to expect better economic conditions over the coming months, this confidence was less than it was in December. However, the QSBO shows retailers are expecting demand to increase, while the BPI does show that 33% of retailers expect to improve their margin which underpins their relatively high confidence compared to other sectors.” – Jason Shoebridge, Chief Executive, NZIER

Retail business leaders are feeling the least positive (14%) about external economic factors that impact their business, including inflation, interest rates and cost of living.

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

“While consumer demand remains uneven and cost pressures are continuing to squeeze margins, many retailers are adapting by staying close to cash flow, managing inventory carefully and making disciplined decisions around pricing and staffing. Rather than chasing growth, the focus is firmly on resilience and sustainability in a challenging retail environment.” – Divya Pahwa, BDO National Retail Sector Leader

In summary, the retail sector’s outlook for the next 6 months has improved considerably (up from 49% to 65%). However, their positivity with current financial performance (19%) remains the lowest across all sectors, with economic pressures still dampening this.

The technology sector is New Zealand’s third largest export earner, behind dairying and tourism. The May BPI Report includes insights for New Zealand’s technology sector for the first time – and the results reflect a sector where business leaders remains optimistic about growth and innovation, while operating in an environment of heightened operating and financial risk.

“In New Zealand, many technology businesses continue to show positivity in their ability to leverage AI and new technologies to drive efficiency and scale. At the same time, the elevated concern around cash flow, financial performance and insolvency risk highlights the pressure created by subdued capital markets, longer sales cycles and increased cost discipline across customers.” – Liam Walker, BDO Business Advisory Services Partner and Technology sector specialist

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

Technology business leaders report mid-range positivity in early 2026. In the April 2026 BPI survey, just over half of respondents in IT and digital services felt positive about their overall business performance, broadly in line with the national average and well ahead of construction.

“The rise of cyber risk management as a top short‑term issue is also telling. As tech businesses accelerate digital adoption and AI enablement, governance, resilience and security maturity are becoming just as important as innovation itself. For many founders and leadership teams, this is prompting a renewed focus on fundamentals - balance sheet strength, forecasting discipline and risk management - alongside growth ambitions.” – Liam Walker, BDO Business Advisory Services Partner and Technology sector specialist

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

Overall, the data points to a sector that is pragmatic rather than pessimistic. Technology leaders are adapting to tougher market conditions, prioritising resilience and sustainability, while positioning themselves to move quickly as positivity and investment conditions improve.

“Tourism businesses are feeling more positive than they were six months ago, but leaders remain cautious. Improving activity is being met with careful cost control, margin protection and a strong focus on cash flow. The sector is rebuilding deliberately, with resilience and flexibility guiding strategy in 2026.” – Richard Timpany, BDO National Tourism Sector Leader

After plummeting to just 40% positive in our last report, an historic low (following a 29‑point drop from May 2025), business performance optimism among tourism business leaders has rebounded markedly in the April BPI survey. Just over half of tourism and hospitality operators now report feeling positive about their current business performance, which is a sizeable improvement, though still shy of the very positivity levels seen in mid‑2025. Improving travel conditions following the late‑2025 downturn, alongside seasonal (summer peak) factors, appear to have supported sentiment. However, looking ahead six months, tourism business leaders expect their business performance optimism to be lower than at present.

Alongside business leaders in the retail sector, 63% of tourism business leaders are expecting fuel price inflation to have a significant impact on their net profit margins in the next 12 months – the second highest across all sectors – impacted by increased travel costs (including flights) and overall cost of living increases.

Expect net profit to improve

(next 12mths)

Expect fuel prices to impact net profit

(next 12mths)

Very likely to be unable to

meet financial obligations

or experience insolvency

(next 12mths)

Actively hiring

(next 12mths)

Expect to feel positive about leveraging new tech & AI

(next 6mths)

More tourism business leaders intend to actively hire in the next 12 months than any other sector. Interestingly, of all business leaders surveyed, those in the tourism sector feel least positive about their ability to leverage and adapt to new technologies, including AI – perhaps a reflection of the (human) staff-dependent nature of their industry.

That said, tourism positivity remains cautious. Forward bookings are improving but not fully secure. High operating costs and margin‑pressured activities continue to challenge tourism businesses. Labour shortages are easing only gradually, and fuel price spikes continue to hit transport and tour operators hard. These factors mean that although tourism leaders are feeling better than in late 2025, their outlook remains guarded.

% Business leaders feeling positive (all or most of the time) in the past 2 weeks.

Overall, the trend for tourism is clearly upward compared to late 2025. Any further lift in positivity is likely to depend on improvements in economic conditions later in 2026, as well as operators’ ability to manage costs, protect margins, and stabilise cash flow.