2018 sees the start of the roll-out of three new accounting standards (the “Big Three”) for for-profit entities that apply NZ IFRS and NZ IFRS (RDR) (“NZ GAAP”).

Also, the Big Three may result in certain “non-large” for-profit companies, partnerships and limited partnerships, becoming “large (1) ”, by pushing them over the asset and revenue thresholds, thus triggering a NZ GAAP preparation requirement.

This Cheat Sheet has been produced as a high-level, helicopter view introduction to these new standards, to get entities thinking about how they might be impacted, and what they need to do.

Need assistance with your transition?

BDO’s IFRS Advisory department is a dedicated service line available to assist entities with their transition projects onto these new standards. Further details are provided on the following page for your information.

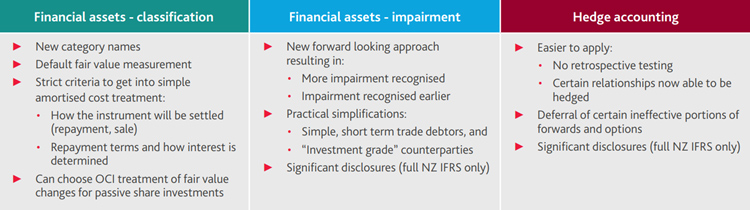

NZ IFRS 9 Financial Instruments (Replaces NZ IAS 39 - Effective from 1 January 2018)

NZ IFRS 9 addresses a number of long-standing practical criticisms regarding some of the “hard lines” that the previous standard took with respect to hedging, and the classification and impairment of financial assets (i.e. cash and cash equivalents, trade debtors, other receivables, advances (including those to related parties, employees, associates and joint ventures etc.), derivatives, investments (bonds, debentures, and passive share holdings).

A high-level summary of the key changes are detailed in the table below:

NZ IFRS 15 Revenue from Contracts with Customers (replaces NZ IAS 18 & 11 – effective from 1 January 2018)

NZ IFRS 15 consolidates revenue treatment into a single, comprehensive standard, following a principle-based 5-step model.

However it is important to note that there are several fundamental changes in principles, criteria, and characteristics which may mean that the current status quo will change in the new NZ IFRS 15 world, for example:

The impact of NZ IFRS 15 will differ from entity-to-entity, as the devil really is in the detail of an entity’s individual contractual arrangements and business practices with its customers.

However, it is anticipated that entities in certain sectors are likely to be more impacted by specific aspects of NZ IFRS 15 than others. These are detailed in BDO’s Industry Specific Publications.

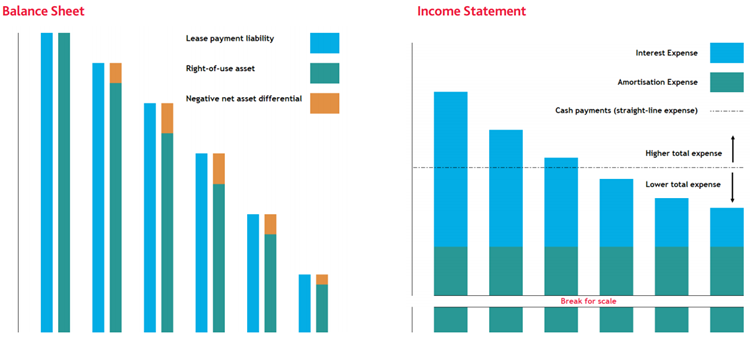

NZ IFRS 16 Leases (Replaces NZ IAS 17 - Effective from 1 January 2019)

NZ IFRS 16 eliminates the current operating lease and finance lease distinction for leases of a lessee.

What this means is that most operating leases whose current treatment is to simply book a straight-line expense over the life of the lease, will now have a lease liability and right-of-use (RoU) asset come on balance sheet which will be treated like a loan (and incur an interest expense) and an asset (and be amortised) respectively.

Exemptions are available for leases of 12 months or less, and for leases of “low value” items. However, in practice, leases of property, vehicles, heavy machinery, and high-value office and IT equipment will all now be on balance sheet.

The impacts of NZ IFRS 16 will affect an entity’s balance sheet, income statement, cash flow statement, and all associated sub-totals and financial metrics which an entity might refer to for other business areas such as earn-outs, employee bonuses, and banking covenants (i.e. EBIT(DA), NPAT, gearing, times interest etc.).

Because the lease liability is treated like a loan (i.e. incurring interest on the outstanding balance, with loan payments then reducing the balance), it generally unwinds more slowly than the RoU asset (unless it is required to be amortised over a period longer than the lease term). This (typically) results in:

- A negative net asset position over the life of the lease

- Higher interest cost (and therefore total cost) in the early years of the lease

- An improved EBIT, and significantly improved EBITDA (as lease expense is now interest cost & amortisation)

- No change to total cash out flow (but now presented primarily in financing activities)

This is presented visually in the diagrams below (based on a simple, vanilla lease example).

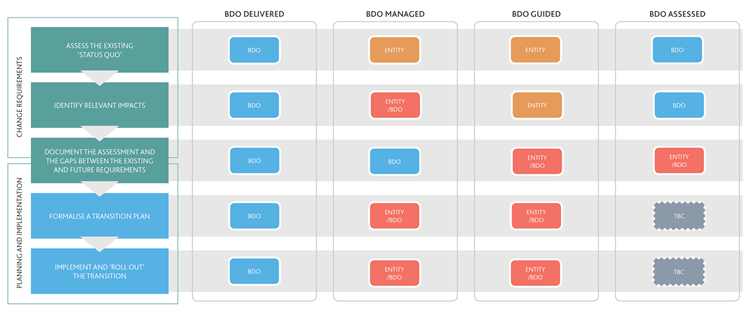

BDO IFRS Advisory - Tailored “Big Three” Transition Assistance

BDO adopts a flexible approach to assisting entities with their transition to the Big Three, meaning we can be as involved as an entity requires, based on their own in-house resourcing and expertise at their disposal.

Often entities don’t know exactly where to start or focus their energies, and are just wanting to get the ball rolling.

We have found our BDO Guided and BDO Assessed approaches fit well to accommodate this, whilst also retaining the ability to scale up involvement quickly if need be – either way, we work WITH you.

Contact:

For more information as to how BDO IFRS Advisory might assist with assessing the impact of your transition to the Big Three, please contact James Lindsay or visit our IFRS Advisory homepage.

BDO has also a number comprehensive Need to Know and IFRS in Practice publications relating to the Big Three, in addition to the popular IFRS at a Glance summary publications.

These can be accessed, together with other publically available publications, via the BDO Global webpage.

1. NZ companies: $60m assets, $30m revenue; Foreign owned companies: $20m assets, $10m revenue; in thepreceding two years.

Get in touch with our team to find out more

Contact us