Background

For year ends 31 December 2019 and onwards, the long awaited new accounting standard regarding leases (NZ IFRS 16 Leases) comes into effect.

NZ IFRS 16 is a nuanced accounting standard, with various practical complexities to navigate through. Many of these present themselves in property leases, even though, at first glance, these may appear to be fairly “simple”.

This Cheat Sheet has been produced as a high-level overview of the practical complexities that property leases may create for those entities adopting NZ IFRS 16.

Need assistance with your adoption of NZ IFRS 16?

BDO IFRS Advisory Services is a dedicated service line available to assist entities in adopting NZ IFRS 16. Further details are provided on the following page for your information.

What is covered in the Cheat Sheet

In order to navigate through this area of NZ IFRS 16, this Cheat Sheet is broken down into the following sections:

- Why the focus on Property leases?

- Multi-faceted aspects to Property leases

- Complexities in determining the Lease Liability

- Complexities in determining the Right-of-Use Asset (RoU Asset)

- Other application complexities to consider

- Concluding thoughts and comment

1. Why the focus of Property leases?

Property leases typically have a longer stream of higher-value lease payments compared to other types of leases. These two elements result in much larger (i.e. material) asset and liability balances to be accounted for, with corresponding impacts across an entity’s financial statements and other financial metrics (i.e. EBIT(DA), gearing, interest expense etc.).

As such, property lease are likely to get more attention from an entity’s stakeholders, particularly bankers and other funders, external auditors and/or regulators.

Also, even fairly straight-forward “vanilla” property leases can contain terms and features which result in areas of management judgement, management estimation, and recalculation – all highlighted in the following sections.

2. Multi-faceted aspects to Property leases

Property leases can include (i) multiple leased items, and (ii) non-lease items.

(i) Multiple lease items

Property leases can include leases of (separate) buildings, land, car parking, plant and equipment etc.

Also, with respect to car parks, a lease may not technically exist for these in situations where the agreement does not assign specific car park spaces to the entity (i.e. as there is no identifiable asset). In these cases, the portion of the agreement related to car parking (including an allocation of the payments to the lessor) is accounted for as a "non-lease item" (see below)."

As far as practicably possible, it is advisable that an entity record and account for these separately (i.e. as separate leases), so that the consequential accounting impacts of any changes in the scope or nature of the items (i.e. floor area, number of carparks etc.) can be isolated to only those items.

(ii) Non-lease items

Only payments (or portion thereof) that relate to the item(s) being leased are subject to NZ IFRS 16’s on-balance sheet accounting requirements.

However, property leases typically incorporate (directly, or inherently) payments for non-lease items, such as: cleaning; maintenance, security, utilities, rates etc. – these are commonly referred to as “OPEX” payments.

Payments for OPEX might be: (i) fixed in the contract; (ii) paid on an as-incurred basis; or, (iii) embedded in the lease payment (i.e. not specifically separated out).

However, rather than trying to identify what needs to be separate out (and then, how to do this – which has its own complexity to deal with) NZ IFRS 16 contains an option to just simply include OPEX payments (and other non-lease payments) as part of the lease payments brought on to balance sheet.

Depending on the number of Property leases an entity has, and the different OPEX payment structures, the use of this option may ultimately be a practical necessity, rather than an option of choice.

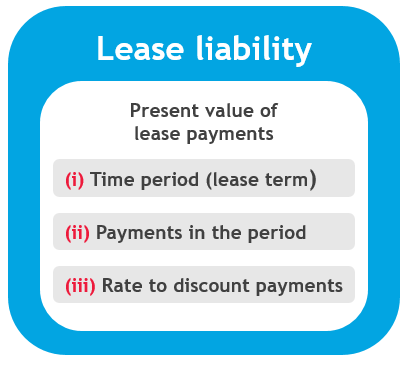

3. Complexities in determining the lease liability

The lease liability represents the present value of the lease payments over the lease term, and therefore requires three core inputs in order to execute the calculation. Property leases, by their nature, typically include features that can make the determination of these three inputs less than straight forward.

(i) Time period (lease term)

- Property leases typically include renewal options, termination options and/or roll-over options.

Where such options are “reasonably expected” to be used (or not) they are included (excluded) in determining the lease term – based on an unbiased assessment of the relevant financial and non-financial penalties.

(ii) Payments in the period

- Property leases typically include payments that change as a result of inflation (CPI) and/or rent reviews. Once such changes in payments occur, recalculations are performed and adjustments recorded.

- Property leases typically include rent-free periods. These are “zero” value lease payments in the lease payment schedule.

- Payments for non-lease OPEX (see 2. above).

- Property leases do not typically include purchase options or residual value guarantee payments, but if so, these need to be estimated and included.

- Property leases can include usage-based payments. Depending on specific facts and circumstances, payments of this nature may need to be excluded from the lease payment schedule (in full, or in part).

(iii) Rate to discount payments

- Property leases don’t typically specify the lessor’s finance rate in the arrangement.

If so, the entity’s incremental borrowing rate(s) will need to be determined.

This can occur, for example (a) for inter-company, inter-group, and/or related party leases (i.e. where lease payments may be denominated in the lessor’s currency), or (b) in certain developing or hyperinflationary countries (i.e. where lease payments will be denominated in a more stable currency, such as USD).An additional area of complexity related to the lease liability is in situations where the lease payments are denominated in a currency that is different to the functional currency of the lessee, which is more commonly seen in property leases.

(iv) Lease payments denominated in a foreign currencies

As lease payments are made, the foreign currency impacts should be accounted for with respect to (i) the value of the interest expense recognised, and (ii) the closing balance of the lease liability.

4. Complexities in determining the Right-of-Use Asset (RoU Asset)

On day-one, the RoU asset is the sum of the lease liability, plus/minus a number of initial adjustments, all of which are more prevalent in Property leases.

(i) Direct costs

- Property leases typically have real estate commissions and other incremental costs that will need to be added to the RoU asset.

(ii) Restoration (i.e. “make-good” costs)

- Property leases typically include requirements for entity’s to restore (i.e. “make-good”) the property upon exit of the lease.

The cost of this needs to be estimated, added to the RoU asset, and then reassessed at reach reporting date.

(iii) Prepayments

- Amounts paid to the lessor prior to the lease commencing (i.e. those not in lease liability payment schedule) will need to be added to the RoU asset.

This includes any “reverse incentives” – i.e. lease sign-on payments.

(iv) Incentives

- Property leases typically include cash or other asset contributions made by the lessor to the lessee to “entice” them into the lease.

These will need to be deducted to the RoU asset.

.png?lang=en-NZ)

(v) Impairment

However, the complexity does not stop there for the RoU asset associated with property leases. Various other factors that impact subsequent measurement of the RoU asset that will need to be considered.

Like other assets, the RoU asset is subject to an impairment assessment at each reporting date.

The basis of this assessment will be similar in nature to the onerous lease assessments that were previously undertaken under the old accounting standards.

Onerous leases (aka impairment) with respect to property leases are greater and more frequent than other types of leases.

(vi) Fair value measurement

Depending on an entity’s other accounting policies, operations, and the nature of use of its property leases, the RoU asset may need to be continuously measured at fair value (revalued amount).

|

If the entity:

|

If the entity:

|

| The RoU asset MUST be measured at fair value. | The RoU asset CAN also be measured under the revaluation method, if the entity so chooses. |

If the property lease includes a Purchase option that the entity “reasonably expects” to utilise (i.e. has included the purchase option price in the lease payment schedule – refer 3(ii) above), then the amortisation period of the RoU asset is based on the expected useful life of the property - including its useful service life post-lease.

(vii) Longer period of amortisation

5. Other application complexities to consider

(i) Sub-leases an on-leases

Property leases are often more likely to be subject to sub-lease or on-lease.

While there are no significant changes to lessor accounting under NZ IFRS 16, there is a subtle but significant change to the assessment as to whether a (sub-, or on-) lease is an operating lease, or a financing lease – i.e. the assessment is made against the value of the RoU asset recognised on balance sheet for the original lease as lessee.

This will be particularly relevant when the (sub-, or on-) lease is for substantially all of the original: leased item; lease term; and/or, lease payments.

(ii) Different accounting treatment under US GAAP

While the equivalent new lease standard under US GAAP was initially intended to “mirror” that of [NZ] IFRS 16, this ultimately did not eventuate. Instead the US has adopted a different on-balance sheet approach for property leases.

As such, entities with a parent, subsidiary, or other group entities that have property leases and applies US GAAP will need to be conscious of this difference, and apply an appropriate work-around to address this.

(iii) Lease modifications

Property leases are typically more likely to be subject to subsequent modification and (re)negotiation between the parties.

NZ IFRS 16 has strict and clear requirements as to how lease modifications must be accounted for. Some situations will result in more complex recalculations and/or will require updated inputs (i.e. discount rates) to be determined.

(iv) Adopting NZ IFRS 16 – addressing previous lease-related balances

Property leases typically result in other balances having been previously recognised in the balance sheet, including (a) lease payment accruals and prepayments (b) straight-line accounting accruals (i.e. for past lease incentives, increasing lease payments; (c) deferred gains or losses from previous sale and leaseback transactions; (d) intangible assets from previous business combinations (i.e. (un)favourable lease payments compared to market).

Depending on the adoption approach an entity elects, NZ IFRS 16 will have specific treatment requirements for addressing these balances upon adoption of NZ IFRS 16.

6. Concluding thoughts and comments

(i) Management judgements, management estimation, and recalculations

From the areas highlighted above, it should be clear that applying NZ IFRS 16 to property leases may not be a straight-forward exercise. Property leases are more-likely-than-not going to require areas of management judgement, management estimation, as well as ongoing (re)calculation.

(ii) Documentation and supporting evidence requirements

| Management judgement | Management estimates | Recalculation required |

|

|

|

This, together with additional time and resource required with adopting NZ IFRS 16, may mean an entity needs to consider the services of external experts to assist them through this process.

Where an entity is subject to external audit and/or regulator oversight, there may be additional emphasis needed on documenting and providing supporting evidence for each of the above points in 6(i).

BDO’s IFRS Advisory team has real life practical experience dealing with property leases when adopting NZ IFRS 16, and stands-ready to assist entities in whatever capacity necessary.

(iii) Lease management software solutions – a necessity or a nice-to-have

|

BDO LEAD Lease management software |

The nature and extent of an entity’s property lease portfolio is typically a key point in deciding whether an entity should investigate investing in a specialised lease management software solution (such as BDO LEAD), rather than defaulting to a manual, spreadsheet approach (which is more time consuming, and vulnerable to error and manipulation). In addition, external audit fees are expected to increase for those entities who choose to utilise manual spreadsheets in situations where the property lease population (i) is moderate – large (no “magic number”, however 10+ typically is the level we find entities wanting to have the conversation), and/or (ii) require frequent recalculation. Therefore, an entity may decide one-off sunk costs being paid over to its external auditor would be better spent towards investing in a long-term software solution that (i) ensures accuracy, (ii) is easier (and therefore, cheaper) to audit, and (iii) mitigates down time of staff (i.e. they are not buried in spreadsheets at month and year end). |

BDO IFRS Advisory – Tailored Adoption Assistance

BDO adopts a flexible and fully customisable approach to assisting entities with their adoption of new accounting standards. This allows us to be as involved as an entity requires, so that this can be built around an entity’s own existing in-house resourcing and expertise.

Often entities have an idea of what needs to be done, but don’t know exactly where to start or focus their energies, and just want to get the ball rolling.

We have found our BDO Guided and BDO Assessed approaches fit well to accommodate this, whilst also retaining the ability to scale up involvement quickly if need be – either way, we work WITH you.

Members of BDO’s IFRS Advisory department come ready with real life experience in adopting NZ IFRS 16 and are therefore well placed to provide entities with the expertise and assistance they require.

For more information as to how BDO IFRS Advisory might assist with assessing the impact of your adoption to new accounting standards please contact James Lindsay or visit our Financial Reporting Advisory webpage.

Get in touch with our team to find out more

Contact us