Background

For year ends 31 December 2019 and onwards, the long awaited new accounting standard regarding leases (NZ IFRS 16 Leases) comes into effect.

Part of the day-1 (and adoption) accounting requires the lease payments over the lease term to be discounted. Where the discount rate is not provided in the lease agreement (which is the case for most leases not formally constructed as “Finance leases” currently), NZ IFRS 16 requires an entity to use its incremental borrowing rate (IBR).

This Cheat Sheet has been produced as a high-level overview of what an entity’s IBR is, how it is applied, and avenues to seek to determine it.

Need Assistance with your adoption of NZ IFRS 16?

BDO IFRS Advisory is a dedicated service line available to assist entities in adopting NZ IFRS 16. Further details are provided on the following page for your information.

What is covered in the Cheat Sheet

In order to navigate through the topic of IBRs, this Cheat Sheet is broken down into the following sections:

- Reminder – Where discount rates fit into NZ IFRS 16

- The flow-on impacts of the IBR

- What the IBR is, and is not

- What parameters need to be included when determining the IBR

- How many IBRs does an entity have – General application

- How many IBRs does an entity have – Upon adoption to NZ IFRS 16

- How is an Entity’s IBR calculated

1. Reminder – Where discount rates fit into NZ IFRS 16

Discount rates are one of the three key inputs required when applying NZ IFRS 16, with the other two being (i) determining the lease term, and then (ii) determining the lease payments over that lease term.

The discount rate is then applied to the lease payment profile to get to a day-1 present-value, which represents the value of the opening Lease liability, which in turn forms the basis of the corresponding Right-of-use Asset (RoU Asset).

With respect to the discount rate, NZ IFRS 16 requires that an entity use (in order of hierarchy):

|

Other than leases that have been specifically structured as Financing leases, this is expected to be rare (Also, note that this is not the payment-default interest rate in the agreement). |

|

In order to do this correctly, an entity would need full and transparent financial information regarding the LESSOR. In practice, this is almost certainly unlikely to be obtainable. |

|

Therefore, for leases where the discount rate is not explicit, nor determinable, an entity must use the IBR associated with the lease. |

It is important to note that as IBRs will need to be determined by an entity, based on its unique facts and circumstances, they will represent a key management estimate in applying NZ IFRS 16, which will likely be of interest to senior management and the entity’s auditor.

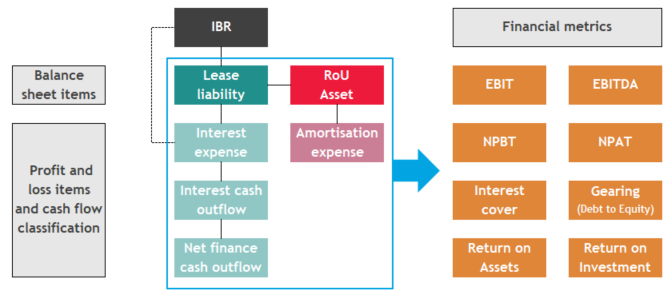

2. The flow-on impacts of the IBRs

IBRs directly and indirectly impact (i) the initial values of balances in an entity’s balance sheet, (ii) the subsequent line items in an entity’s profit or loss, (iii) the split of cash flows in an entity’s cash flow statement, and, consequentially, (iv) the value of various financial metrics

For example, the higher (lower) the IBR:

- The lower (higher) the initial day-1 value of the Lease liability (i.e. the heavier it is discounted)

- The lower (higher) the initial day-1 value of the RoU Asset (i.e. as this is based on the Lease liability)

- The higher (lower) the value of subsequent Interest expense

- The lower (higher) the value of subsequent Amortisation expense.

- The higher (lower) the value of subsequent Interest cash outflows (i.e. as this is based on the Interest expense), and lower (higher) the value of Net finance cash outflows (i.e. as this is the difference between the lease cash payment, and Interest cash outflow).

- Financial metrics will be lower or higher depending on the aggregate impact of all of the above.

What should be clear, is that the IBR has extensive flow-on and on-going impacts across an entity’s entire financial statements and reported results. As such, accurately determining the IBR should be a priority for all entities.

3. What the IBR is, and is not

The definition of IBR in NZ IFRS 16 is:

The rate of interest that a lessee would have to pay to borrow over a similar term and with similar security, the funds necessary to obtain an asset of similar value to the right-of-use asset in a similar economic environment.’

Other than this, NZ IFRS 16 does not contain any additional significant guidance on how IBRs are determined.

However, we can clarify definitively what the IBR is NOT:

| IBR is NOT | Reason and additional details |

|

WACC (Weighted average cost of capital) |

An entity’s WACC includes the cost of equity. However, the IBR is a cost of debt only. |

|

WACD (Weighted average cost of debt) |

An entity’s WACD is measure of the cost of its existing debt. However, the IBR is a cost of additional (i.e. incremental) debt. |

|

Cash rate (OCR, LIBOR etc.) |

The cash rate is not specific to the entity’s own cost of debt. However, the IBR is specific to an entity. |

|

Inter-company rate (i.e. the rate charged between group entities to advance/borrow funds) |

An entity’s (group’s) inter-company lending rates are typically fixed, and set to achieve the cheapest possible cost of debt available (i.e. borrowing from a low-interest jurisdiction to then disseminate across the wider group). However, the IBR must be based on various parameters (i.e. those highlighted above), one of which being the market rate of borrowing in the jurisdiction where the lessee operates. |

4. Parameters that need to be included when determining the IBR

To ensure that an entity is determining the correct IBR for a lease, an entity must ensure the following parameters are represented:

- Jurisdiction: The country the lessee is operating in (Economic environment)

- Lease term: The duration of the lease payment profile (Term)

- Amount: The total lease payments[1] over the lease term (Amount)

- Asset type: The nature of the underlying item being leased (Security)

For example:

If a New Zealand subsidiary (entity) of an Australian parent leased an office in Auckland for five years, with total lease payments of $500,000, the IBR that the entity would need to determine would be the rate that would be charged, in New Zealand, to borrow $500,000 to be paid back over five years, secured against property (i.e. office space).

Changing one or more of these parameters would result in a different IBR being determined, e.g.:

- A longer (shorter) lease term should result in higher (lower) IBR.

- A higher (lower) total lease payment amount should result in a higher (lower) IBR.

- If the asset type was more “risky” in terms of holding its value (i.e. equipment), the IBR should be higher

- If the jurisdiction were not New Zealand, then the IBR may be different (depending on the specific jurisdiction’s economic environment).

5. How many IBRs does an entity have – General application

Unless an entity has only one lease, or, multiple leases with EXACTLY the same IBR parameters (refer 4. above), an entity will have more than a single IBR. That being said, it does not mean that an entity will need to determine unique IBRs for each and every lease that it holds.

NZ IFRS 16 allows an entity to group leases with “similar characteristics” into “portfolios”, and then determine a single IBR for that portfolio.

In terms of the IBR parameters (refer 4. above), such grouping will be limited to only Lease term, and, Amount (i.e. it is unlikely that grouping leases from different Jurisdictions, or for different Asset types, would be appropriate).

In practice, an entity would likely establish an IBR policy with “bands” for Lease term, and, Amount – the number and range of which would be specific to the entity.

An entity’s IBR policy is an area of management judgement, for this reason it will be important to obtain consensus on its structure from senior management, as well as the entity’s auditors.

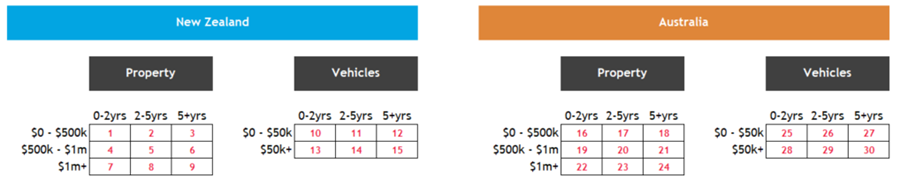

For example:

Entity A operates in New Zealand and Australia, and leases both property and vehicles.

Entity A determines that for its property leases, both in New Zealand and Australia:

- There will be three Lease term bands: 0 – 2 yrs , 2 – 5yrs , 5+yrs

- There will be three Amount bands: 0 - $500k , $500k - $1m , $1m+

Entity A determines that for its vehicle leases, both in New Zealand and Australia:

- There will be three Lease term bands: 0 – 2 yrs , 2 – 5yrs , 5+yrs

- There will be two Amount bands: 0 - $50k , $50k+

Entity A determines that it will set and update IBR’s annually.

Accordingly, Entity A’s IBR policy will result in it having 30 potential IBR’s to be determined for its leases (i.e. assuming Entity A enters into a lease within each of the below parameters, which may not necessarily be the case).

Note, that if Entity A’s IBR policy was to set ant update IBR’s on a more frequent basis (i.e. quarterly) then the number of potential IBR’s to be determined for a single year would increase by that factor (i.e. by 4 times, resulting in potentially 120 IBRs to be determined for Entity A)

6. How many IBRs does an entity have – Upon adoption of NZ IFRS 16

The number of potential IBRs that an entity will need to determine upon adoption to NZ IFRS 16 will depend on which adoption option an entity elects to use.

|

Method 1 – Fully Retrospective Method (FRM) |

Method 2 – Modified Retrospective Method (MRM) |

|

This method requires that NZ IFRS 16 is applied retrospectively as if it had always been applied, with fully restatement of prior period comparatives. Because of this, a further parameter needs to be factored in when determining the IBRs… and that is the lease origination Year (i.e. the start date of each and every lease). An entity’s IBRs change over time as a result of changes in the economic environment, and the entity’s own credit risk, and therefore when applying the FRM the start date of the lease is relevant. This will expand an entity’s potential IBR’s to be determined subject to the age of the Entity’s lease population (i.e. from the example in 5. above, based on Entity A’s IBR policy, if the oldest lease in Entity A’s population commenced 10 years ago, then potentially 300 IBRs would need to be determined for Entity A). This is one of a number of reasons why the FRM is a more complicated adoption option, as this option requires an entity to have access to very detailed historical economic data in addition to its own historical data. |

Unlike the FRM, this method is applied on a “look-forward” basis. As such, an entity uses only current IBRs (i.e. at adoption date), and doesn’t need to look-back and determine the IBR that existed at the commencement of each lease. Therefore the Year parameter is nullified. This is one of a number of reasons why the MRM is a less complicated adoption option. Also, the MRM also has an additional option which with respect to the Term parameter, which permits and entity to only consider the remaining term of a lease (not the total original term). Accordingly, all other parameters being equal, leases that may have had vastly different original terms can at adoption be grouped in the same IBR portfolio so long as their remaining term is similar (i.e. fits within an entity’s IBR policy Term band). This another reason why the MRM is a less complicated adoption option. |

7. How the IBR is calculated

As noted in 3. above, NZ IFRS 16 does not provide any specific guidance on how IBRs are to be calculated.

Rather, per its definition, NZ IFRS 16 indicates what should be considered when determining IBRs.

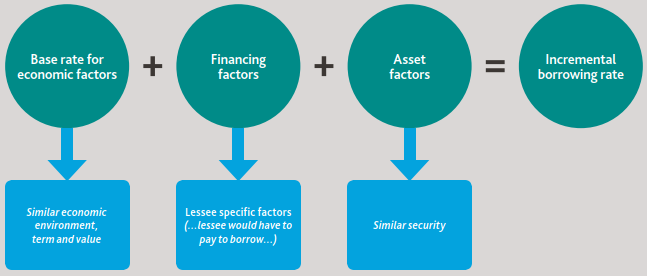

Practicably, an appropriate methodology for determining IBRs is to take the underlying economic base rate applicable to the lease, overlay the lessee specific financing cost, and then adjust for the nature of the underlying leased item:

For example:

Entity A has a 5 year office lease in New Zealand with total lease payments of $500k.

Per the methodology above, Entity A would determine the IBR associated to this lease the following way:

- Base rate: Risk-free-rate (i.e. 5 year, $500k, New Zealand Government Bond rate).

- Financing factors: Add a margin for Entity A’s specific, unsecured credit-risk of borrowing.

- Asset factors: Deduct the amount associated to the “protection” (security) the underlying leased item has to the financer in a secured lending arrangement.

Each of these elements, and illustrative examples, are discussed in detail in BDO’s comprehensive IFRS in Practice 2019 publication (pages 37 – 44), available at the link below:

BDO IFRS In Practice

Alternatively, and entity may be able to approach its external financer (i.e. bank), and simply ask the question:

Because of this, the use of external experts may be necessary to determine an entity’s IBR, such as Corporate Finance specialists.As noted in the sections above, the IBR represents a key management estimate (which will need to be disclosed), with far reaching consequential impacts across a wide range of balances, amounts, and financial metrics.

“What interest rate would you charge [ENTITY] to borrow $[X], to be paid back over [Y] years, secured against [LEASED ASSET]?”

Whatever approach an entity decides to take to calculate its IBRs, the “Who” and “How” should be explicitly included in an entity’s internal IBR policy.

The IBR policy should then reviewed and confirmed by senior management and the entity’s auditor (including confirmation of that nature of support and evidence required to substantiate the IBRs determined).

BDO IFRS Advisory – Tailored Adoption Assistance

|

BDO adopts a flexible and fully customisable approach to assisting entities with their adoption of new accounting standards. This allows us to be as involved as an entity requires, so that this can be built around an entity’s own existing in-house resourcing and expertise. Often entities have an idea of what needs to be done, but don’t know exactly where to start or focus their energies, and just want to get the ball rolling. |

|

|

We have found our BDO Guided and BDO Assessed approaches fit well to accommodate this, whilst also retaining the ability to scale up involvement quickly if need be – either way, we work WITH you. |

|

|

Members of BDO’s IFRS Advisory department are well placed to provide expertise in the adoption of NZ IFRS 16, and BDO’s Corporate Finance team is available to assist entities in navigating the determination of their Incremental Borrowing Rates as part of this process. |

|

|

|

For more information as to how BDO IFRS Advisory might assist with assessing the impact of your adoption to new accounting standards please contact James Lindsay or visit our IFRS Advisory webpage. |

[1] Note that this excludes any non-lease payments under the lease, even if the entity has elected to apply the option in NZ IFRS 16 permitting lease payments and non-lease payments being accounted for together.