Civil infrastructure, residential and commercial projects

Civil and infrastructure firms report the strongest current sentiment and forward work position. While their six-month outlook is more cautious, more of these firms expect gross profit margins to improve over the next year.

Budget 2026 has since added further context to this outlook, with the Government announcing a $7 billion capital investment package for hospitals, schools, roads, rail and other public infrastructure. Because our survey closed before this announcement, the results do not yet capture how that investment may affect confidence, work pipelines or construction activity over the year ahead. The key question for civil and infrastructure firms will be how quickly announced funding flows through to funded, consented and deliverable projects.

Read more about what the infrastructure could mean for construction business leaders here.

The stronger civil and infrastructure outlook is consistent with wider market commentary, revealing infrastructure as one of the more resilient parts of the sector. However, resilience does not remove risk. Government funding decisions, procurement timing, fuel costs and civil construction cost inflation can all influence tender pricing and project viability. For firms in this subsector, the opportunity is significant, but so is the need for strong cost control and disciplined contract management.

Survey responses show civil and infrastructure firms are the most positive about their current business performance, although their positive sentiment eases when looking six months ahead. By contrast, residential and commercial respondents are more positive about the next six months than they are today, suggesting some expectation of gradual improvement from a lower base.

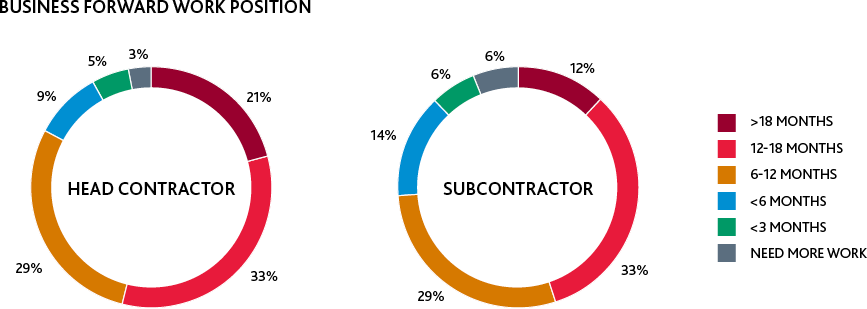

Longer pipelines are concentrated in civil and infrastructure

The forward work data reinforces that civil and infrastructure firms have a stronger pipeline than other subsectors. Fifty-seven percent of civil and infrastructure firms surveyed have sufficient confirmed work for more than 12 months.

Residential and commercial recovery remains fragile

Residential construction firms have the highest reported need for more work, at 8%, compared with 5% of commercial businesses. The heightened expectations of positive business performance sentiment in 6 months’ time among residential and commercial firms may reflect expectations that lower interest rates, improving economic sentiment or delayed projects will support activity over time. However, the data also suggests these subsectors remain commercially exposed. Residential firms report the greatest need for more work, while both residential and commercial businesses are more likely than civil and infrastructure firms to expect margins to fall. That points to a recovery that may be gradual and uneven, rather than a broad-based rebound.

Work secured does not always mean margin protected

The margin data highlights one of the most important messages for 2026; having work secured is not the same as having profitable work secured. Civil and infrastructure firms are the most optimistic about margin growth, with 28% expecting gross profit margins to increase over the next 12 months.

Businesses with increased gross profit margin

(last 12 mths vs expectation for next 12 mths)

By contrast, commercial and residential firms are more likely to expect margins to fall, despite some improvement in forward sentiment. This suggests competitive tendering, cost escalation, scope changes and client affordability are still weighing on profitability.

Labour demand follows pipeline visibility

Labour demand is strongest where pipeline visibility is strongest. Civil and infrastructure firms are the most likely to be looking for staff, with 34% expecting to actively recruit over the next 12 months. This reflects stronger forward work, but also creates a challenge: Firms need sufficient capacity to deliver confirmed projects without overcommitting in a market where timing can still shift. Residential firms are less likely to be recruiting, with most saying current staffing levels meet their needs, which aligns with their shorter pipelines and greater need for new work.

Hot topics by subsector

Across each subsector, there is continued variability in how construction businesses are experiencing the current market. However, consistency is evident in business leaders maintaining focus on the practical issues that will shape resilience over the year ahead; protecting margin, managing cash flow, securing the right people and deciding where technology can genuinely improve productivity.

Civil and infrastructure firms appear better positioned on margin expectations and hiring intentions, reflecting their stronger pipeline visibility. However, they are less likely than other subsectors to identify technology and AI adoption as a priority. That creates an opportunity: As larger and more complex projects move through the pipeline, better use of technology could help improve estimating, project management, procurement, workforce planning and reporting.

By contrast, the residential sector’s higher exposure to financial stress and insolvency risk highlights the pressure still facing businesses where demand is more sensitive to household confidence, funding conditions and affordability.