When is a lease not a lease?

IFRS 16 Leases (“IFRS 16”), which comes into effect for financial reporting periods beginning on or after 1 January 2019, will fundamentally change the manner in which lessees account for leases, by requiring them to bring the majority of their operating leases onto their statements of financial position.However, only leases, as defined in IFRS 16, will be impacted, and this article addresses one of the common difficulties faced in relation to accounting for leases under IFRS 16, which is determining whether a lease exists.

IFRS 16 requires an entity, at the inception of a contract, to assess whether the contract is, or contains, a lease.

Determining whether a lease exists

Under IFRS 16, a contract is, or contains, a lease if it conveys the right to control the use of an identified asset for a period of time in exchange for consideration.Therefore, in determining whether a lease exists under IFRS 16, we need to consider:

- Whether there is an identified asset; and

- Whether the contract conveys the right to control the use of the identified asset.

Identified asset

An asset is typically identified by being explicitly specified in a contract, but can also be identified by being implicitly specified at the time that the asset is made available for use.Portion of assets

Where an agreement gives an entity a right to use a capacity portion of an asset rather than a whole asset, it is an identified asset if it is physically distinct (for example, a floor of a building). If it is not physically distinct (for example, a capacity portion of a fibre optic cable) it is not an identified asset, unless it represents substantially all of the capacity of the asset, and thereby provides the entity with the right to obtain substantially all of the economic benefits from using the asset.No identified asset if supplier has substantive substitution rights

Even if an asset is specified, an entity does not have the right to use the identified asset if the supplier has the substantive right to substitute the asset throughout the period of use. A supplier’s right to substitute an asset is substantive only if both of the following conditions exist:- The supplier has the practical ability to substitute alternative assets throughout the period of use, and

- The supplier would benefit economically from exercising its right to substitute the asset.

Example:

A currency exchange service enters into a contract with an airport to use a space in the airport. The contract states:

- The amount of space to be leased (square metres)

- That the space may be located at any one of several international boarding areas within the airport

- That the airport operator has the right to change the location of the space at any time during the period of use.

Although the amount of space the currency exchange service uses is specified in the contract, there is no identified asset because the airport operator has a substantive right to substitute the asset throughout the period of use, i.e.:

- It has the practical ability to change the space used by the currency exchange service, and

- It would benefit economically from substituting the space.

Right to control the use of the identified asset

A contract conveys the right to control the use of an identified asset throughout the period of use if the entity has both of the following:- The right to obtain substantially all of the economic benefits from using the identified asset, and

- The right to direct the use of the identified asset.

Generally, an entity has the right to direct the use of the identified asset if it has the right to direct how and for what purpose the asset is used throughout the period of use. However, there may be instances where judgement is required to determine whether the customer or supplier directs the use, including where decisions about the use of the asset are pre-determined.

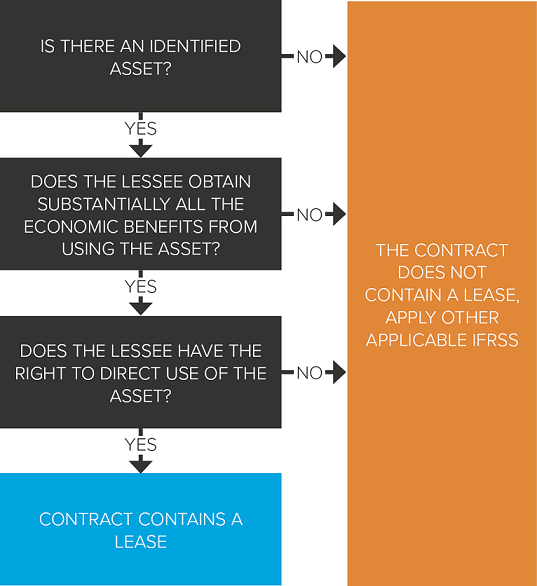

The decision tree below, from IFRS 16, paragraph B31, illustrates how to determine if a contract is, or contains, a lease:

Concluding thoughts

It is possible that some contracts that are currently accounted for as leases will not meet the requirements to be accounted for as leases under IFRS 16. As companies prepare for their adoption of IFRS 16, finance teams will need to obtain copies of all lease contracts that will be in effect at the date of IFRS 16 adoption and determine whether those leases will be within the scope of IFRS 16. As many entities enter into substantial numbers of lease arrangements, this is likely to be a complex and time consuming task. For that reason, it is important that companies commence the process as soon as possible.For more on the above, please contact your local BDO representative.

Subscribe to receive the latest BDO News and Insights

Subscribe