What’s hot in 2023 for CFOs and finance teams

What’s hot in 2023 for CFOs and finance teams

The deteriorating economic conditions and geopolitical uncertainties we saw in 2022 and the unprecedented weather events leading to the flooding that New Zealand has experienced in early 2023 continue to impact businesses during 2023. There are several ‘hot’ issues that are likely to impact CFOs from a strategic perspective, and also their finance teams who must apply appropriate accounting in this uncertain economic environment. Some of these ‘hot’ issues or challenges include:

- A looming recession – earnings pressures and need to optimise cost structures

- Inflationary pressures

- Exorbitant energy prices

- Rapidly increasing interest rates

- Continued supply chain issues

- A persistent skills shortage

- The need for additional capital

- Ability to obtain new finance or refinance existing loan facilities

- Insurance claims from the recent flooding events.

What’s hot for CFOs?

As a result, the top three priorities for CFOs from a strategic perspective are likely to be the following:

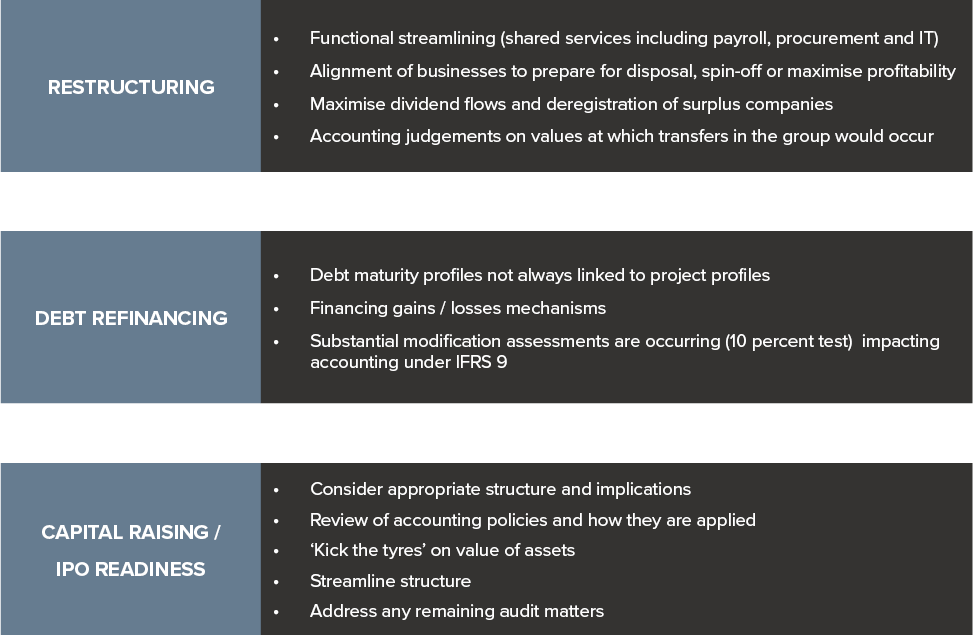

Restructuring

Functional restructuring may be required or desirable for your business to reduce the organisation’s cost structure and obtain efficiencies, including adopting a shared services model for payroll, procurement and IT. We are also seeing CFOs looking at how to align businesses to prepare for a disposal or spin-off, or merely to maximise profitability. In this regard, any restructuring should maximise dividend flows and enable deregistration of surplus companies.

Debt financing

Given the current state of the economy, many CFOs will be looking to refinance their borrowings, either to obtain better terms, or because their existing financier is looking to de-risk its loan book. In addition, debt maturity profiles for long-dated projects may require refinancing during 2023 because the maturity profile does not always line up with the timeline for project construction. Given the higher interest rate environment, we expect financiers to make businesses ‘jump through hoops’ to obtain new and extended finance, including meeting stringent covenants, and also ESG benchmarks.

Capital raising/IPO readiness

In order to prepare for a capital raising or IPO, CFOs should consider the appropriate structure and implications, including tax and accounting. Regardless of whether you are looking at private or public capital, make sure your house is in order.

Focus on energy

Some industries are more sensitive to increasing energy prices than others, but few are immune. In addition, CFOs will need to ensure new projects consider transition to green energy and are also still viable.

CFOs should consider the impact of entering into Power Purchase Arrangements (PPAs) to ensure energy security. Accounting for these can be complex. Depending on the structure of the agreements, PPAs can include embedded derivatives and have a big impact on optimal balance sheet structure.

What’s hot for the finance team?

- Knock-on effects of the recent flooding

- Interest rate and exchange rate volatility

- Rising energy prices

- Supply shortages

- Inflation

- Ongoing war and unrest between Russia and Ukraine

BDO has produced a publication - Accounting in Times of Uncertainty that discusses some of the implications and considerations for entities when preparing financial statements for the year ended 31 December 2022 and beyond.

Finance teams need to consider:

- Going concern

- Judgements, estimates and estimation uncertainties

- Impairment of non-financial assets

- Discount rates

- Events after the reporting period

- Assessment of control, joint control and significant influence

- Effects of inflation

- Financial instruments

- Disclosures.

We recommend finance teams review the detailed discussion on all of the above in our publication. However, we would like to point out some key takeaways you may not have considered previously.

Disclosing estimation uncertainty

This continues to be a focus area for regulators worldwide, including the Financial Markets Authority (FMA). Many entities provide minimal detail quantifying key assumptions that have a significant risk of resulting in a material adjustment to the carrying amounts of assets or liabilities in future periods. Providing less information may actually result in more questions from the FMA. Our publication sets out expectations of regulators with regard to disclosure of estimation uncertainty:

| Regulator expectations |

| Clearly specify which estimates have a significant risk of material adjustment to the carrying amount of assets and liabilities in the next financial year. |

| Clearly distinguish the disclosure of other estimates, and associated sensitivities, from significant estimates and explain their relevance. |

| Quantify the specific amount at risk of material adjustment (i.e., the carrying amount). |

| Provide sufficient granularity in the descriptions of assumptions and/or uncertainties to enable users to understand management’s most difficult, subjective or complex judgements. |

| Provide meaningful sensitivities and/or ranges of reasonably possible outcomes for significant estimates. For example, sensitise the most relevant assumptions, and choose alternate assumptions that are considered reasonably possible. |

| Quantify the assumptions underlying significant estimates when investors need this information to fully understand their effect. |

| Explain any changes to past assumptions if the uncertainty remains unresolved. |

| Sources of estimation uncertainty and the related disclosures should be updated at the balance date. |

It should be noted that the above expectations around estimation uncertainty do not just apply to entities that fall under the FMA’s jurisdiction. These requirements apply equally to all Tier 1 and Tier 2 entities reporting under NZ IFRS and Public Benefit Entity Standards (PBE Standards).

Discount rates

Discount rates used in the past may no longer be appropriate given recent interest rate increases in New Zealand. The requirements for determining the discount rate varies between NZ IFRS Standards (and PBE Standards for Public Benefit Entities (PBEs), as shown in the table below.

|

IFRS Standards |

Discount rate |

|

NZ IAS 36 Impairment of Assets |

Pre-tax rate that reflects current market assessment of the time value of money and the risks specific to the asset for which cash flow estimates have not been adjusted. |

|

NZ IAS 19 Employee Benefits (PBE IPSAS 39 Employee Benefits) |

Market yields on high quality corporate bonds. For currencies for which there is no deep market in high quality corporate bonds, the market yields on government bonds denominated in that currency shall be used. |

|

NZ IFRS 16 Leases |

Incremental borrowing rate (when the interest rate implicit in the lease cannot be readily determined). Refer to our article - What recent interest rate increases mean for discount rates used for lease accounting for more information. |

|

NZ IAS 37 Provisions, Contingent Liabilities and Contingent Assets (PBE IPSAS 19 Provisions, Contingent Liabilities and Contingent Assets) |

Pre-tax rate that reflects current market assessment of the time value of money and the risks specific to the liability for which cash flow estimates have not been adjusted. |

|

IFRS 2 Share-based Payment |

Risk-free rate used in option pricing models such as Black-Scholes (following the principles in NZ IFRS 13 Fair Value Measurement). |

When determining the appropriate discount rate:

- Avoid double counting – if cash flow estimates are adjusted for certain risks, the discount rate should not also reflect that risk

- Where pre-tax discount rates are required, simply grossing up a rate derived from weighted average cost of capital (WACC) may not give you the right answer, particularly in complex scenarios or where multiple tax rates are involved

- If using nominal cash flows, which include the effect of inflation, use a discount rate that includes the effect of inflation

- You may need to involve a specialist to help you determine an appropriate rate

- Provide clear, entity-specific disclosure as to how the discount rate was determined, including assumptions used.

Effects of inflation

Given that most major economies have experienced rising inflation over the past year, finance teams need to be cognisant that the following areas could be affected:

| Accounting area | Implication of rising inflation |

| Discount rates | As noted above, the discount rate may be impacted by rising inflation. |

| Share-based payments | Inflation may lower demand for goods and services, and poorer performance may mean that the likelihood of achieving internal performance conditions may be reduced. |

| Derivatives | Inflationary clauses embedded in revenue or supply contracts may need to be separated and accounted for as a derivative. |

| Expected credit loss calculations | Rising inflation may lead to an increase in the risk of default. |

| Debt modifications | An increase in the occurrence of these are expected and will require application of the ’10 percent test’ to determine whether there has been a substantial modification for accounting purposes. |

| Leases |

Variable lease payments dependent upon inflation requires remeasurement of lease liabilities. Any modifications to lease contracts as a result of inflationary pressures requires a reassessment of the incremental borrowing rate used to discount the lease liability. |

| Inventories | Estimated costs necessary to make a sale are expected to increase and this could result in higher inventory obsolescence if higher costs are not passed on to customer through higher selling prices. |

| Employee benefits | Inflation affects actuarial assumptions used to measure defined benefit plans and other long-term employee benefits, such as assumptions about future salary increases and discount rates. |

| Government grants | Governments may provide below-market interest rate loans which need to be accounted for under NZ IAS 20 Accounting for Government Grants and Disclosure of Government Assistance. |

| Impairment of assets | Higher discount rates lower the value of assets or cash-generating units which may be a possible indicator of impairment and entities need to reassess their estimated cash flows used in value in use calculations. |

| Provisions | Contracts may become onerous due to increasing costs without a corresponding increase in revenues, for example, in the case of long-term fixed rate revenue contracts. IAS 37 was recently amended to clarify which costs are included when assessing whether a contract is onerous. |

Need assistance?

Please contact our IFRS Advisory team if you require assistance with any financial reporting matters during 2023.

For more on the above, please contact your local BDO representative.

This publication has been carefully prepared, but is general commentary only. This publication is not legal or financial advice and should not be relied upon as such. The information in this publication is subject to change at any time and therefore we give no assurance or warranty that the information is current when read. The publication cannot be relied upon to cover any specific situation and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact the BDO member firms in New Zealand to discuss these matters in the context of your particular circumstances.

BDO New Zealand and each BDO member firm in New Zealand, their partners and/or directors, employees and agents do not give any warranty as to the accuracy, reliability or completeness of information contained in this article nor do they accept or assume any liability or duty of care for any loss arising from any action taken or not taken by anyone in reliance on the information in this publication or for any decision based on it, except in so far as any liability under statute cannot be excluded. Read full Disclaimer.