IFRS 9 could lead to earlier (and frequently greater) impairment recognition

One of the major changes introduced by IFRS 9 Financial Instruments (“IFRS 9”) relates to the impairment of financial assets.Incurred loss model

Currently, the incurred loss impairment model for financial assets under IAS 39 Financial Instruments: Recognition and Measurement (“IAS 39”) recognises impairment losses on financial assets only when there is objective evidence of impairment as a result of a past event that occurred subsequent to the initial recognition of the financial asset.Expected loss model

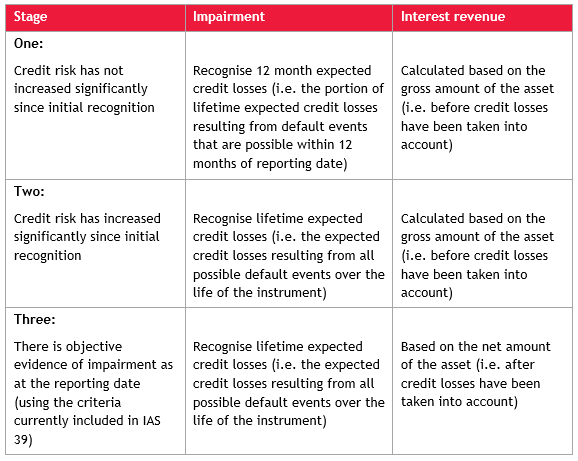

In contrast, IFRS 9 uses a forward looking expected loss model to determine the impairment of financial assets.The IFRS 9 expected loss model is a three stage model that recognises impairment based on whether there has been a significant deterioration in the credit risk of a financial asset. The stage that the asset is in determines the amount of impairment to be recognised (as well as the amount of interest revenue):

Lifetime expected losses are the present value of expected credit losses that arise if a borrower defaults on its obligation at any point throughout the term (i.e. the weighted average of losses multiplied by the probability of default during the term of the financial asset).

The recognition pattern for impairment and interest revenue is therefore:

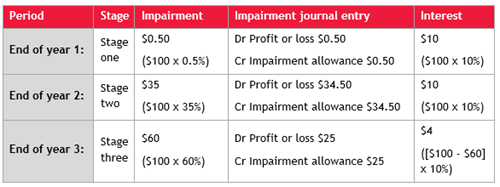

Example

Company A lends $100 to Company X for five years at 10% interest; the loan is unsecured.

At the end of:

- Year one, the probability of default over the life of the loan is unchanged since initial recognition and there is 0.5% probability of the loan defaulting in the next 12 months with a 100% loss

- Year two, Company X is expected to have cash flow problems due to a deterioration in economic conditions and is expected to breach its loan covenants; the probability that the loan will default over the remaining life of the loan is 35%

- Year three, Company X breaches its banking covenants; Company A estimates that the probability that the loan will default over the remaining life of the loan is 60%.

The following table shows Company A’s calculation of impairment and interest revenue on the loan, and the impairment journal entries at the end of each of the first three years of the loan period:

Simplified approach

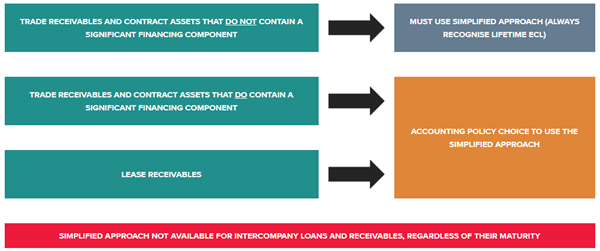

IFRS 9 establishes a simplified approach to impairment in certain circumstances, as the diagram below illustrates:

The simplified approach allows an entity to always recognise lifetime expected credit losses (ECL), rather than having to work through the three stage model. It is only mandatory for trade receivables and contract assets under IFRS 15 Revenue from Contracts with Customers where there is no significant financing component (which is usually the case where maturity is one year or less).

For long-term trade receivables, contract assets and lease receivables, entities can choose to apply the simplified approach as an accounting policy choice.

Lifetime expected losses are the present value of expected credit losses that arise if a borrower defaults on its obligation at any point throughout the term (i.e. all possible default events during the term of the financial asset are included in the analysis).

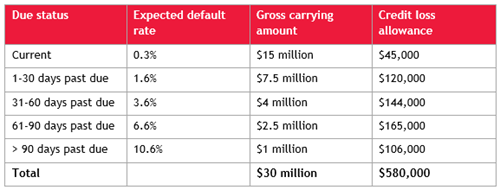

To determine the impairment allowance under the simplified approach, trade receivables are grouped based on their due status or other attributes (e.g. geographical location, customer credit rating, industry etc.). Impairment losses are then calculated based on a weighted average of expected credit losses, with the weightings being based on the respective probabilities of default – these probabilities must reflect both historical and forecast credit conditions.

IFRS 9 is not prescriptive in how balances should be grouped when assessing impairment and the standard includes extensive guidance in this area.

The table below sets out a provision matrix, which is one way of applying the simplified impairment approach, to a trade receivables portfolio of $30 million:

In this instance, impairment of $580,000 would be recognised on the portfolio of receivables. The main differences compared to the provision that would have been recognised under IAS 39 are:

- It includes a provision for trade debtors that are current (i.e. not yet past due), and

- Default rates are based on both historic and forecast data.

Concluding thoughts

Changing from the IAS 39 incurred loss model to the IFRS 9 expected loss model will likely result in earlier impairment recognition, and the recognition of greater levels of impairment over the life of financial assets.In preparation for the implementation of IFRS 9, accounting teams will need to ensure that their financial reporting systems and processes are equipped to calculate impairment based on the new requirements.

For more on the above, please contact your local BDO representative.

Subscribe to receive the latest BDO News and Insights

Subscribe