Determining the transaction price under IFRS 15

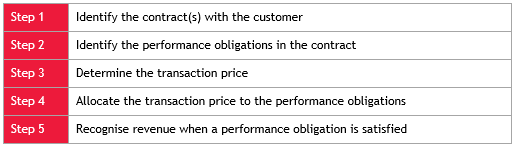

We continue to discuss the five step model for revenue recognition introduced by IFRS 15 Revenue from Contracts with Customers:| Step 1 | Identify the contract(s) with the customer |

| Step 2 | Identify the performance obligations in the contract |

| Step 3 | Determine the transaction price |

| Step 4 | Allocate the transaction price to the performance obligations |

| Step 5 | Recognise revenue when a performance obligation is satisfied |

In this article, we look at some examples of how step three of the IFRS 15 five-step model works.

Determining the transaction price in a contract with a customer

As outlined more fully in the November 2018 edition of Accounting Alert, the transaction price is the “amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties”.The consideration promised in a contract with a customer may include fixed amounts, variable amounts, or both. When determining the transaction price, the entity needs to consider the effects of variable consideration, the existence of a significant financing component in the contract, non-cash consideration, and consideration payable to a customer.

Variable consideration

As outlined more fully in the November 2018 edition of Accounting Alert, the amount of consideration can vary:- Due to a number of factors, including discounts, rebates, bonuses and penalties and other similar items

- If an entity’s entitlement to the consideration is contingent on the occurrence or non-occurrence of a future event (for example, if a product was sold with a right of return).

- The expected value method (i.e. the sum of probability-weighted amounts)

- The most likely amount (i.e. the single most likely outcome of the contract).

The following examples illustrate how some types of variable consideration are accounted for under IFRS 15.

Variable consideration – right of return (based on IFRS 15, Illustrative Example 22)

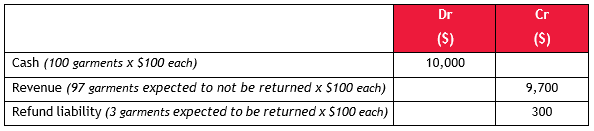

During December 2018, Chain Store sells 100 pairs of jeans to customers for $100 each. Total consideration is consequently $10,000. Cash is received when control of the garments transfer (i.e. at point of sale). Chain Store’s terms and conditions of sale allow customers to return any unworn garments within 30 days and receive a full refund. Chain Store’s cost for each garment is $60.IFRS 15 permits an entity to account for a group of contracts with similar characteristics as a portfolio of contracts, rather than as individual contracts, if the effects on the financial statements of applying IFRS 15 to the portfolio would not differ materially from applying IFRS 15 to the individual contracts. When accounting for a portfolio, an entity must use estimates and assumptions that reflect the size and composition of the portfolio. In this instance, as the product being sold is the same in each transaction, Chain Store can account for the contracts as a portfolio.

The expected value method for estimating variable consideration is generally used where an entity has a large number of contracts with similar characteristics. It is therefore the most appropriate method to use in this instance. Using that method, Chain Store estimates that three of the 100 garments sold will be returned.

In addition, Chain Store:

- Estimates that the costs of recovering the products will be immaterial, and

- Expects that the returned garments can be resold at a profit.

Variable consideration – volume discount (based on IFRS 15, Illustrative Example 24)

Widget Co enters into a contract with a customer on 1 January 2018 to sell Widget A for $100 per unit. If the customer purchases more than 1,000 units of Widget A in a calendar year, the contract specifies that the price per unit is retrospectively reduced to $90 per unit. Consequently, the consideration in the contract is variable.For the first quarter of the calendar year (i.e. to 31 March 2018), Widget Co sells 75 units of Widget A to the customer. Widget Co estimates that the customer’s purchases will not exceed the 1,000-unit threshold required for the volume discount in the calendar year and consequently concludes that it is highly probable that a significant reversal in the cumulative amount of revenue recognised (i.e. $100/unit) will not occur when the uncertainty is resolved (i.e. when the total amount of purchases for the calendar year is known).

As a result of these considerations, Widget Co recognises revenue of $7,500 (75 units × $100/unit) for the quarter ended 31 March 2018.

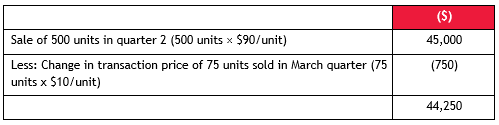

In May 2018 the customer acquires another company and in the second quarter of the calendar year (i.e. the quarter ended 30 June 2018) Widget Co sells an additional 500 units of Widget A to the customer. In the light of this new fact, Widget Co estimates that the customer’s purchases will exceed the 1,000-unit threshold for the calendar year and that it will therefore be required to retrospectively reduce the price to $90/unit.

As a result of these considerations, Widget Co recognises revenue of $44,250 for the quarter ended 30 June 2018. That amount is calculated as follows:

Concluding thoughts

In many instances, determining the transaction price in a contract with a customer is a relatively straightforward process. However, where there is variable consideration, finance teams will be required to apply considerable professional judgement, and the judgements made could significantly impact the timing of revenue recognition. In addition, revenue recognition is unlikely to match invoice amounts and accounting systems and processes need to be set up to account for these differences.For more on the above, please contact your local BDO representative.

Subscribe to receive the latest BDO News and Insights

Subscribe