Accounting for share-based payments

Accounting for share-based payments

Accounting for share-based payments (when an entity is obtaining goods or services in exchange for issuing its shares, or paying in cash where the cash payment is linked to the value of the entity’s shares) is an area that is often overlooked by entities, and it is also an area that can become very complex very quickly.

This article provides a very high-level summary of the accounting requirements when an entity has entered into share-based payment transactions.

Which Accounting Standard applies?

IFRS 2 Share-based Payment is the Accounting Standard that describes the requirements when accounting for share-based payment transactions, regardless of whether the entity can identify specific goods and services received in return. Goods received could include inventories, consumables, property, plant and equipment, intangible assets, and other non-financial assets.

In scope

Under IFRS 2, share-based payment transactions include:

- Equity-settled

- Cash-settled

- Those where the entity or the supplier of goods and services can choose whether the entity settles the transaction in cash or by issuing equity instruments.

IFRS 2 also covers share-based payments settled by another group entity. This may occur, for example, where a parent entity (or shareholder) grants share options to employees of one of its subsidiaries.

Not in scope

The following types of transactions are not within the scope of IFRS 2, and therefore not accounted for as share-based payment transactions:

- Transactions with employees or other parties, in their capacity as a shareholder, for example, if an employee participates in a rights issue to purchase shares of its employer at a discount to fair value

- Shares issued as consideration to acquire a business accounted for under IFRS 3 Business Combinations

- The entity acquires goods or services within the scope of IAS 32 Financial Instruments: Presentation or IFRS 9 Financial Instruments.

What is a share-based payment transaction?

The definition of a ‘share-based payment transaction’ includes goods or services received by an entity in a ‘share-based payment arrangement’. It also covers situations where an entity may not receive goods or services itself but incurs an obligation to settle a transaction with the supplier for goods or services provided to another group entity.

A transaction in which the entity:

- receives goods or services from the supplier of those goods or services (including an employee) in a share-based payment arrangement, or

- incurs an obligation to settle the transaction with the supplier in a share-based payment arrangement when another group entity receives those goods or services.

Definition of ‘share-based payment transaction’ in IFRS 2.

The consideration ‘paid’ to the supplier of goods or services in a ‘share-based payment arrangement’ is always based on the price or value of equity instruments of the entity, or another group entity. ‘Payment’ can either be made in cash (cash-settled) or by issuing equity instruments (equity-settled).

An agreement between the entity (or another group entity or any shareholder of any group entity) and another party (including an employee) that entitles the other party to receive:

- cash or other assets of the entity for amounts that are based on the price (or value) of equity instruments (including shares or share options) of the entity or another group entity, or

- equity instruments (including shares or share options) of the entity or another group entity,

provided the specified vesting conditions are met.

Definition of ‘share-based payment arrangement’ in IFRS 2.

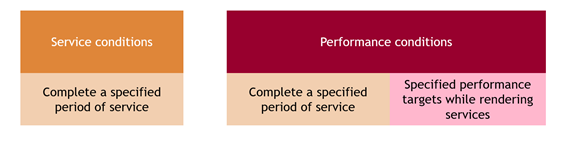

What are vesting conditions?

Vesting conditions determine whether the entity receives the goods or services that entitle the counterparty (supplier/employee) to receive the cash or equity instruments under the share-based payment arrangement. A vesting condition is either a service condition or a performance condition.

Performance targets can be based on:

- The entity’s own operations or those of another group entity, such as revenue or profit targets (non-market conditions), or

- The price of the entity’s or another group entity’s share price (market conditions).

Sometimes share-based payment arrangements contain ‘non-vesting conditions’ because there is no specified service period, or because the performance targets do not relate to either market conditions or non-market conditions as explained above (e.g., a target commodity price).

This distinction is important because it drives measurement of share-based payment expenses, which are discussed further below.

Equity-settled share-based payment transactions

An entity must always recognise an equity-settled share-based payment transaction in its books if it receives the goods or services. It does not matter if the entity issues its own equity instruments in return, or whether it has no obligation because it has been assumed by another group entity.

Cash-settled share-based payment transactions

Cash-settled share-based payment transactions must also be recognised under IFRS 2. These occur where an entity receives good or services and incurs a liability to the supplier that is based on the price (or value) of the entity’s equity instruments, or that of another group entity.

Basic recognition principles

Goods acquired in a share-based payment transaction are recognised when the entity obtains control of the goods.

Services are recognised as the services are received.

The ‘credit side’ of the entry is recognised in equity for an equity-settled share-based payment transaction or as a liability for a cash-settled share-based payment transaction.

The debit side is recognised as an expense, unless it qualifies for recognition as an asset under other accounting standards (e.g., shares issued to purchase property, plant and equipment recognised under IAS 16 Property, Plant and Equipment).

Measuring equity-settled share-based payment transactions

There is a rebuttable presumption that the goods and services received, and the corresponding increase in equity, are measured directly at the fair value of the goods and services received. If this value cannot be estimated reliably, their value is measured indirectly by reference to the fair value of the equity instruments granted.

For employee services, the fair value of services received is measured by reference to the fair value of equity instruments granted, i.e. the presumption of using the fair value of goods and services received is rebutted. This is because it is not usually possible to reliably estimate the fair value of employee services received.

Example

Entity ABC acquires inventories with a fair value of $100 and issues 100 shares to its supplier as consideration. The inventories are received by Entity ABC on 1 April 2022 when Entity ABC’s share price is $1.20.

Entity ABC recognises the following journal entry on 1 April 2022:

Dr Inventories $100

Cr Equity $100

However, if the presumption is rebutted because Entity ABC cannot reliably estimate the fair value of the inventories on 1 April 2022, Entity ABC would recognise the following journal entry on 1 April 2022:

Dr Inventories $120

Cr Equity $120

When to recognise expense for services received in an equity-settled share-based payment transaction

Immediate vesting

Equity instruments granted for services received may vest immediately because they are for past services provided to the entity, and the employee or service provider is not required to complete a specified period of service. In such cases, an expense is recognised in full on ‘grant date’, with a corresponding increase in equity.

Delayed vesting

If the equity instruments do not vest until the counterparty completes a specified period of service, it is assumed that the entity receives the services in future, during the ‘vesting period’. The entity therefore recognises the expense over the vesting period, at the fair value on grant date.

If Entity DEF grants 100 share options to an employee with a three-year service condition, the vesting period is three years. If the fair value of the options on grant date is $150, Entity DEF would recognise the following journal entry for each year of the service period (assuming the share options are granted on the first day of the financial year):

Dr Share-based payment expense $50

Cr Equity $50.

Sometimes the vesting period will be variable. For example, when an employee is required to achieve certain performance conditions while remaining in the entity’s employment, the vesting period will end once the performance condition in satisfied. In such cases, the entity will need to determine the expected vesting period at grant date, based on the most likely timing the performance condition will be met.

If the performance condition is a ‘market condition’, the vesting period must be consistent with assumptions used to estimate the fair value of the options granted and is not subsequently updated. However, for ‘non-market conditions’, the vesting period length is updated, which means the share-based payment expense measured at grant date is ultimately recognised over a longer or shorter period than first anticipated.

How to measure fair value by reference to the fair value of equity instruments granted

IFRS 2, Appendix B1-B41 contains detailed guidance on how to determine fair value for equity instruments granted. The following option-pricing models are often used in practice, but others should be considered in certain circumstances.

| Type of option | Features | Option pricing model |

| European options | Can only exercise on an agreed future date at a pre-agreed price | Black-Scholes |

| American options | Can exercise at any date before the expiration date at a pre-agreed price |

Binomial |

Fair value is determined at grant date. The table below shows how vesting conditions do/do not impact the fair value of the equity instruments granted.

| Market Conditions (e.g. certain share price is achieved) |

Non-market conditions (e.g. certain revenue or profit targets) |

Non-vesting conditions (e.g. target commodity price) |

| Take the conditions into account when determining fair value at grant date | Ignore when determining fair value at grant date | Take the conditions into account when determining fair value at grant date |

| Expense recognised over vesting period, even if condition not met | If condition not met – ‘true up’ (reverse) cumulative expense recognised | Expense recognised over vesting period, even if condition not met |

| Do not revise number of instruments expected to vest | Revised number of instruments expected to vest | Do not revise number of instruments expected to vest |

What happens after vesting date to share-based payment reserve?

After recognising and measuring share-based payment transactions as described above, if equity instruments (options/rights) lapse unexercised, the balance in the share-based payment reserve (equity) is not reversed in profit or loss. However, an entity can choose to make a transfer within equity to transfer the balance to another reserve.

Modifications and cancellations – cannot ‘set and forget’

It is important to note that once you have established the appropriate accounting treatment for your equity-settled share-based payments at grant date, it’s not just a case of ‘set and forget’. IFRS 2, paragraphs 26-29 and B42-B44, contains complex requirements when accounting for cancellations and modifications of share-based payment arrangements. Working out how to account for these may require expert advice.

Cancellations are generally treated as an acceleration of vesting, and any ‘unamortised grant date expense’ is recognised immediately. For example, if equity instruments have a $150 fair value at grant and vest over three years, the annual expense is $50. However, if the arrangement is cancelled after one year, an immediate write-off of the remaining $100 is required.

Modifications can be more complicated. The general principle is that when a share-based payment arrangement is modified, the minimum expense recognised over the vesting period is the original fair value. If the modification increases fair value to the recipient (e.g., by reducing the exercise price with all other facts remaining the same), that additional fair value is recognised over the remaining vesting period.

In some cases, cancellations of share-based payment arrangements can be accounted for as modifications where an entity identifies replacement equity instruments at the same time as it cancels the original instruments.

The accounting for anything other than ‘vanilla’ cancellations and modifications can be very complicated. Please speak to a member of BDO’s IFRS Advisory team if you require assistance.

Recognising and measuring cash-settled share-based payment transactions

Cash-settled share-based payment transactions are recognised in a similar manner to equity-settled share-based payments, i.e., when control is obtained of goods, or over the period when services are received. The main difference is that fair value recognised as a credit to equity for equity-settled share-based payments is set at grant date and not changed, whereas the cash-settled share-based payment liability (credit entry) is continually updated to fair value at each reporting date until the liability is settled. Changes to the fair value of this liability are recognised in profit or loss (even though the liability may relate to the purchase of an asset).

Share-based payments with cash alternatives

IFRS 2 contains further detail where share-based payment transactions provide the counterparty, or the entity, with a choice of settlement. Please refer to IFRS 2, paragraphs 34 to 43.

Share-based payment transactions amongst group entities

Where entities in a group produce separate (individual) financial statements, they need to ensure they have accounted for all share-based payment transactions. It is easy for such entities to forget to include these because they may be receiving services (e.g., from employees) but not paying for them because the parent entity is picking up the tab and issuing its own shares to the subsidiary’s employees.

Entity receiving goods or services

If an entity receives goods or services, IFRS 2, paragraph 43B requires it to recognise an equity-settled share-based payment transaction, even if it does not issue any of its own equity instruments. Expenses recognised are then only reversed if a non-market condition fails to be met.

As an example, if Parent grants 100 equity instruments (fair value $300) to Sub A’s employees if they remain employed for a three-year period, Sub A recognises the following journal entry in each of the three years:

Dr Share-based payment expense $100

Cr Equity $100.

This entry is regardless of intragroup payment arrangements that require a different settlement amount between group entities.

Entity settling the obligation

The entity settling a share-based payment transaction when another group entity receives the goods or services recognises an equity-settled share-based payment if it will settle the obligation by issuing its own instruments, otherwise its obligation is a cash-settled share-based payment liability.

Following on from our example above, Parent entity would recognise the following journal entry in each of the three years:

Dr Investment in Sub A $100

Cr Share-based payments reserve $100.

More information and assistance

Our IFRS in Practice provides examples of common errors we encounter in practice where entities fail to identify share-based payments or apply inappropriate accounting.

Please contact BDO’s IFRS Advisory team if you require assistance with your organisation’s share-based payment accounting.

For more on the above, please contact your local BDO representative.

This publication has been carefully prepared, but is general commentary only. This publication is not legal or financial advice and should not be relied upon as such. The information in this publication is subject to change at any time and therefore we give no assurance or warranty that the information is current when read. The publication cannot be relied upon to cover any specific situation and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact the BDO member firms in New Zealand to discuss these matters in the context of your particular circumstances.

BDO New Zealand and each BDO member firm in New Zealand, their partners and/or directors, employees and agents do not give any warranty as to the accuracy, reliability or completeness of information contained in this article nor do they accept or assume any liability or duty of care for any loss arising from any action taken or not taken by anyone in reliance on the information in this publication or for any decision based on it, except in so far as any liability under statute cannot be excluded. Read full Disclaimer.

Subscribe to receive the latest BDO News and Insights

Subscribe