Accounting for financial guarantees under IFRS 9

In the October 2018 edition of Accounting Alert we examined accounting for financial liabilities under the requirements of IFRS 9 Financial Instruments (“IFRS 9”). In this article we look at financial guarantees, which under IFRS 9 are accounted for as financial liabilities, as they were under IAS 39 Financial Instruments: Recognition and Measurement (“IAS 39”). Note that, under IFRS 9, an entity that has previously explicitly asserted that it considers and accounts for financial guarantees as insurance contracts can elect to apply IFRS 4 Insurance Contracts instead of IFRS 9 (this was also the case under IAS 39).Initial recognition

A financial guarantee contract is initially recognised at fair value. If the guarantee is issued to an unrelated party on a commercial basis, the initial fair value is likely to equal the premium received. If no premium is received (which is often the case in intra-group situations), the fair value must be determined using a method that quantifies the economic benefit of the guarantee to the holder.

| The fair value of a financial guarantee contract is calculated as the present value of the difference between the net contractual cash flows required under a debt instrument, and the net contractual cash flows that would have been required without the guarantee. |

Subsequent recognition

At the end of each subsequent reporting period, financial guarantees are measured at the higher of:- The amount of the loss allowance, and

- The amount initially recognised less cumulative amortisation, where appropriate.

Expected credit losses for a financial guarantee contract are the cash shortfalls adjusted by the risks that are specific to the cash flows. Cash shortfalls are the difference between:

- The expected payments to reimburse the holder for a credit loss that it incurs, and

- Any amount that an entity expects to receive from the holder, the debtor or any other party.

Example one

On 1 January 2019, Company A guarantees a $1,000 loan of Subsidiary B, which Bank XYZ has provided to Subsidiary B for three years at 7%.Interest payments are made at the end of each year and the principal is repaid at the end of the loan term.

If Company A had not issued a guarantee, Bank XYZ would have charged Subsidiary B an interest rate of 10%. Company A does not charge Subsidiary B for providing the guarantee.

On 31 December 2019, there is a 1% probability that Subsidiary B will default on the loan in the next 12 months. If Subsidiary B defaults on the loan, Company A does not expect to recover any amount from Subsidiary B.

On 31 December 2020, there is a 3% probability that Subsidiary B will default on the loan in the next 12 months. If Subsidiary B defaults on the loan, Company A does not expect to recover any amount from Subsidiary B.

1 January 2019

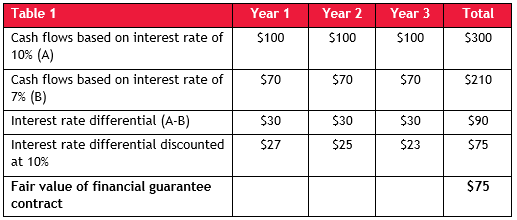

The guarantee must be recognised at fair value. The fair value of the guarantee will be the present value of the difference between the net contractual cash flows required under the loan, and the net contractual cash flows that would have been required without the guarantee.

| Table 1 | Year 1 | Year 2 | Year 3 | Total |

| Cash flows based on interest rate of 10% (A) | $100 | $100 | $100 | $300 |

| Cash flows based on interest rate of 7% (B) | $70 | $70 | $70 | $210 |

| Interest rate differential (A-B) | $30 | $30 | $30 | $90 |

| Interest rate differential discounted at 10% | $27 | $25 | $23 | $75 |

| Fair value of financial guarantee contract | $75 |

The difference between the two cash flows is $75 ($1,000 - $925), which is the fair value of the financial guarantee at inception.

The journal entry is:

| Dr ($) |

Cr ($) |

|

| Investment in subsidiary | 75 | |

| Financial guarantee (liability) | 75 |

If Subsidiary B was an unrelated party, the above journal entry would result in an expense in the books of Company A.

31 December 2019

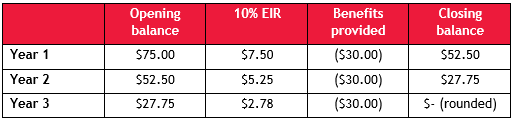

At 31 December 2019, there is 1% probability that Subsidiary B will default on the loan in the next 12 months. This is not a significant increase in the probability of default from 1 January 2019. If Subsidiary B defaults on the loan, Company A does not expect to recover any amount from Subsidiary B. The 12-month expected credit losses are therefore $10 ($1,000 x 1%).The initial amount recognised less amortisation is $52.50 ($75 + $7.50 [interest accrued at the 10% effective interest rate] – $30 [benefit of the guarantee in year 1], per the table below, which shows amortisation for the entire three years of the loan/guarantee. The unwound amount is recognised as income to Company A, as it is the benefit derived by Company A because Subsidiary B did not default on the loan during the period.

| Table 2 | Opening balance | 10% EIR | ‘Benefits’ provided | Closing balance |

| Year 1 | $75.00 | $7.50 | ($30.00) | $52.50 |

| Year 2 | $52.50 | $5.30 | ($30.00) | $27.80 |

| Year 3 | $27.80 | $2.78 | ($30.00) | $- |

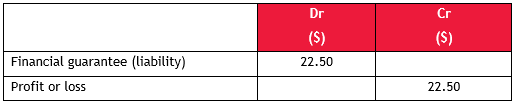

The carrying amount of the financial guarantee liability after amortisation is therefore $52, which is higher than the 12-month expected credit losses of $10. The liability is therefore adjusted to $52 (the higher of the two amounts) as follows:

| Dr ($) |

Cr ($) |

|

| Financial guarantee (liability) | 23 | |

| Profit or loss | 23 |

31 December 2020

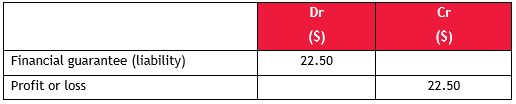

At 31 December 2020, there is 3% probability that Subsidiary B will default on the loan in the next 12 months, which is not a significant increase in the probability of default. If Subsidiary B defaults on the loan, Company A does not expect to recover any amount from Subsidiary B. The 12-month expected credit losses are therefore $30 ($1,000 x 3%).The initial amount recognised less amortisation is $27.75 (from the amortisation table above), which is lower than the 12-month expected credit losses ($30). The liability is therefore adjusted to $30 (the higher of the two amounts) as follows:

|

|

Dr ($) |

Cr ($) |

| Financial guarantee (liability) | 22 | |

| Profit or loss | 22 | |

|

Calculated as the carrying amount at the end of 31 December 2019 of $52 less 12-month expected credit losses of $30 |

||

Example two

Same facts as for Example one, except that at 31 December 2019 there is a significant increase in the risk that Subsidiary B will default on the loan.The probability of default over the remaining life of the loan (two years) is 60%.

If Subsidiary B defaults on the loan, Company A does not expect to recover any amount from Subsidiary B.

31 December 2019

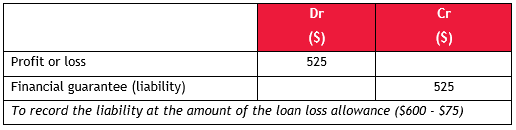

As Company A does not expect to recover any amount from Subsidiary B, the lifetime expected credit losses are $600 (60% x $1,000), and the carrying amount is adjusted as follows:

| Dr ($) |

Cr ($) |

|

| Profit or loss | 525 | |

| Financial guarantee (liability) | 525 | |

| To record the liability at the amount of the loan loss allowance ($600 - $75) | ||

Concluding thoughts

Careful monitoring of the loans for which financial guarantees have been provided is essential for both risk management and accounting purposes. Finance teams should ensure that they have processes in place to undertake such monitoring on a regular basis.Subscribe to receive the latest BDO News and Insights

Subscribe