Sale and lease back transactions – determining profit or loss on disposal of assets by seller-lessees is a complex process

In the May 2019 edition of Accounting Alert, we showed how the new leasing standard, IFRS 16 Leases (“IFRS 16”) has changed the accounting for sale and leaseback transactions (“SALTs”). While the current accounting is driven by the classification of the lease portion of the arrangement as an operating or finance lease, the IFRS 16 treatment depends on whether the transfer of the asset qualifies as a sale under IFRS 15 Revenue from Contracts with Customers ("IFRS 15"). Where the leaseback arrangement qualifies as a sale, the seller-lessee then recognises a profit or loss on disposal of the asset.

Profit or loss on disposal is not simply equal to fair value less carrying amount

Determining the profit or loss on disposal by the seller-lessee is a complex process.

The seller-lessee’s profit or loss on disposal will therefore not simply be equal to the fair value of the asset less its carrying amount, as it may have been under IAS 17 Leases (“IAS 17”). Instead, it is:

- The amount of consideration attributable to the portion of the asset for which control has passed to the buyer-lessor (i.e. monies received which do not have to be paid back to the lessor over the leaseback period), less.

- The portion of the asset’s carrying amount attributable to the period after the end of the leaseback, and for which control has passed to the buyer-lessor.

This complexity is best illustrated with an example.

Fact pattern

- Seller-lessee enters into a sale and leaseback transaction whereby it sells a property to a buyer-lessor for $2,000,000. Fair value (“FV”) of the property at the time of sale is $1,800,000.

- Simultaneously, the seller-lessee leases the property back from the buyer-lessor for a period of 18 years with annual lease payments at the end of each year of $120,000.

- The sale meets the criteria of IFRS 15 to be accounted for as a sale.

- There are no initial direct costs in the transaction.

- Before the transaction occurs, the property has a carrying value of $1,000,000.

- Discount rate is 4.5% p.a. determined by reference to the seller-lessee’s incremental borrowing rate (because the rate inherent in the lease is not readily determinable).

Step 1: Accounting for difference between FV and consideration as additional borrowings

Because the consideration of $2,000,000 exceeds the fair value of the property at time of sale ($1,800,000), the excess consideration of $200,000 is accounted for as additional financing provided by the buyer-lessor to the seller-lessee, and not consideration on the sale side of the transaction.

Step 2: Calculate lease liability for lease payments due

Using the 4.5% discount rate, the present value of the annual leaseback payments (18 payments of $120,000) is $1,459,200.

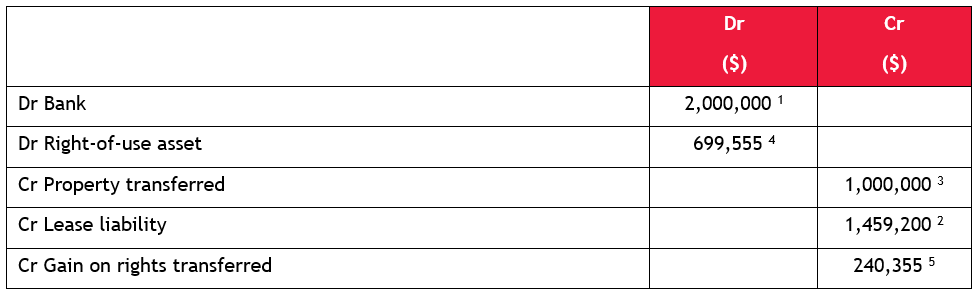

Step 3: Journal entries

The journal entry to record this transaction is as follows (see corresponding notes reconciling each component of the entry):

Notes:

- Total cash received from the buyer-lessor.

- Present value of future lease payments of $1,459,200 ($120,000 per year for 18 years discounted at 4.5%). This includes repayments for the additional borrowing of $200,000 determined in Step 1 above. If the proceeds on sale had been on-market at $1,800,000, then the present value of the leaseback payments would only have been $1,259,200 ($1,459,200 - $200,000). The proceeds above market on the sale side of the transaction are therefore treated as additional financing.

- The previous carrying value of the property is derecognised.

- The retained right-of-use of the asset sold is measured by reference to the previous carrying value of the property. The fair value of the property is $1,800,000, while the FV of the leaseback rental is $1,259,200 (refer note 2. above). Therefore, the cost of the property for which control has not passed to the buyer-lessor = $1,000,000 x $1,259,200/$1,800,000 = $699,555.

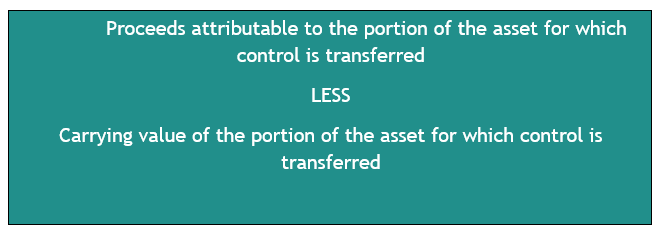

- The gain on sale is the balancing entry in the transaction, but can be reconciled as follows:

Proceeds attribute to the propoetion of the asset being disposed of is calculated as follows:

.png.aspx?lang=en-NZ)

Carrying value of the portion of the asset being sold is calculated as follows:

.png.aspx?lang=en-NZ)

The gain on disposial is therefore:

.png.aspx?lang=en-NZ)

Lower profit on disposal likely for real estate transactions

As noted above, the current accounting for SALTs required by IAS 17 varies depending on whether the leaseback qualifies as a finance or operating lease.

SALTs are common for transactions involving real estate, which normally resulted in the leaseback being classified as an operating lease by the seller-lessee under IAS 17. Due to the lessee now having to exclude from the calculation of profit on disposal the total consideration attributable to the financing received, the accounting required by IFRS 16 will typically result in smaller gains on disposal when recognising the sale side of the transaction. Taking the same facts as the example above, IAS 17 would have resulted in a profit on the sale side of the transaction of $800,000 (total proceeds of $2,000,000 less $200,000 to be deferred less asset’s carrying value of $1,000,000), which is significantly more than the $240,345 recognised under IFRS 16.

Don’t forget to remeasure carrying amount of asset being sold

It should be noted that the carrying value of the asset being sold and leased back must be at its appropriate amount following the application of other International Financial Reporting Standards prior to the SALT.

For example, if land had a carrying value of $100,000 immediately prior to a SALT, where the sales price (at the fair value of the land) was $90,000, the seller would have to apply IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations (“IFRS 5”) prior to accounting for the SALT. Applying IFRS 5, paragraph 15, the seller would measure the land at the lower of its carrying amount and fair value less costs to sell. As the SALT is about to take place, the lower of carrying amount ($100,000) and fair value less costs to sell ($90,000 from the SALT) is $90,000; therefore, the land should be written down prior to the SALT accounting.

For more on the above, please contact your local BDO representative.