More common errors when accounting for property, plant and equipment (IAS 16 and PBE IPSAS 17– Part 4)

IAS 16 Property, Plant and Equipment (or the equivalent PBE IPSAS 17 Property, Plant and Equipment for Public Benefit Entities (PBEs)) is a relatively simple standard to read and apply, yet it is a standard where preparers can easily make errors which affect amounts recognised as property, plant and equipment (PPE) in the statement of financial position.Over the last few months, we have explored common errors relating to:

- The scope of IAS 16 (April Accounting Alert)

- Measurement at cost or revalued amounts (May Accounting Alert), and

- Calculating depreciation, specifically errors made when determining useful lives and residual values (Mid June Accounting Alert).

Error 1 – Component assets with different useful lives

Expensive items of PPE sometimes include components of high value that need to be replaced more often than the main asset. For example, an aircraft body may have a longer useful life than the engines and the seats.IAS 16, paragraph 43 (PBE IPSAS 17, paragraph 59) requires that these complex assets be componentised. Parts of the asset with a significant cost relative to the total cost of the asset are to be separated and depreciated separately if they have a different useful life to the main asset.

| Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately. IAS 16, paragraph 43 PBE IPSAS 17, paragraph 59 |

Example

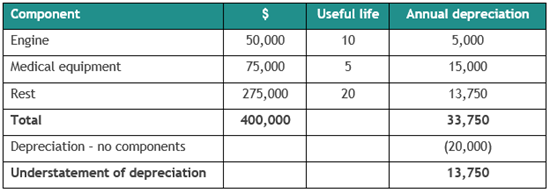

Flying Doctors purchases a helicopter for $400,000, which includes the:- Engine ($50,000 if purchased separately on acquisition date)

- Seats ($10,000 if purchased separately on acquisition date)

- Bespoke medical treatment equipment ($75,000 if purchased separately at acquisition date).

A common error occurs if Flying Doctor depreciates the $400,000 cost of the helicopter over 20 years, or $20,000 a year. IAS 16, paragraph 43 (PBE IPSAS 17, paragraph 59) tells us to split the cost down into significant component parts with different useful lives, and to depreciate each one separately.

In this scenario, if they have different useful lives, the engine and the bespoke medical equipment should be treated as separate significant components to the helicopter body (seats probably not) and depreciation is calculated as follows:

You can see from the above example that failing to separately identify components would result in the depreciation charge being understated by 40%.

Error 1Failing to separately identify significant components of assets and depreciate them using specific useful lives. |

Error 2 – Allocation of depreciation

The basic principle in IAS 16 and PBE IPSAS 17 is that depreciation is an expense to be recognised in profit or loss (surplus or deficit for PBEs). However, in some cases, it should form part of the cost of another asset which has been produced as a result of using the depreciable asset. For example, depreciation of machinery used to manufacture a widget will be capitalised as a conversion cost under IAS 2 Inventories (PBE IPSAS 12 Inventories), and if used to produce an intangible asset, will be included as part of the cost under IAS 38 Intangible Assets (PBE IPSAS 31 Intangibel Assets).| The depreciation charge for each period shall be recognised in profit or loss unless it is included in the carrying amount of another asset. IAS 16, paragraph 48 The depreciation charge for each period shall be recognised in surplus or deficit unless it is included in the carrying amount of another asset. PBE IPSAS 17, paragraph 64 |

Errors can be made in one of two ways with this IAS 16, paragraph 48 (PBE IPSAS 17, paragraph 64) requirement. Be careful not to allocate excessive amounts of depreciation expense to the cost of assets, and also remember that some portion of depreciation expense is to be allocated to the cost of manufactured inventories or internally generated intangible assets.

Error 2Failing to include depreciation expense as part of the cost of inventories (IAS 2/PBE IPSAS 12) and intangible assets (IAS 38/PBE IPSAS 31), or including too much depreciation. |

Error 3 – Failing to depreciate PPE because the item’s fair value is increasing

Except for most types of land with unlimited useful lives, other PPE items are always depreciated, regardless of whether the ‘cost’ or ‘revaluation’ model is applied. This is because they are assumed to have a finite life, and the economic benefits embodied in the asset are assumed to be ‘used up’ over the life of the asset (useful life). The only time we do not depreciate an asset is if its ‘residual value’ is equal to, or greater than its carrying amount.| No depreciation if: Residual value > Carrying amount |

You can see from the descriptions in the above table that:

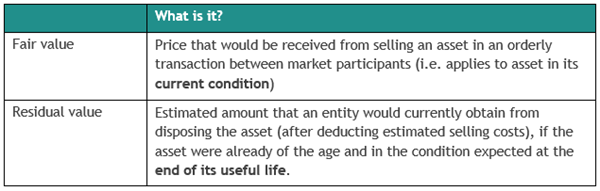

- ‘Fair value’ refers to the price you could obtain today if you sell the asset in its current condition, whereas

- ‘Residual value’ is the amount you could the sell the asset for today if it were already of the age and condition when you expect to sell it.

Example

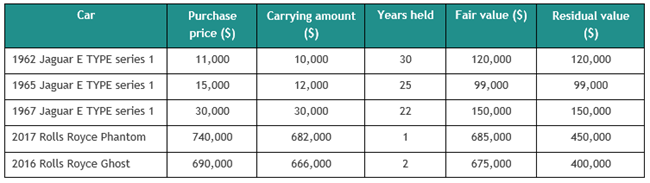

The Luxury Car Company rents out luxury and vintage cars on a short-term basis (e.g. for weddings and other functions). At 30 June 2018 it owned the following vehicles:

In all cases, the fair value is greater than the carrying amount, so you may be tempted to argue that no depreciation is required. However, as noted above, ‘fair value’ is the amount we would receive if we sell these cars in their current condition, but ‘residual value’ is the amount we would receive if we sold these assets and they were already of the age and condition when we intend to sell.

No depreciation is required for the E TYPE Jaguars because the residual values for all three exceed the carrying amount. This is due to the increasing residual values for vintage cars. However, even though the fair values for the two Rolls Royce models exceed the carrying amount, the residual value is expected to be less than carrying amount if Luxury Car Company intends to hold them for a number of years, and so depreciation is required over the expected useful life.

Error 3Incorrectly assuming that no depreciation is required where fair value exceeds carrying amount. |

Error 4 – Start depreciating PPE items too late

The ‘depreciable amount’ of PPE must be allocated on a systematic basis over its ‘useful life’ (IAS 16, paragraph 50 and PBE IPSAS 17, paragraph 66).Useful life is:

|

A common error is to start depreciating the asset after is becomes available for use, i.e. after it is in the location and condition necessary for it to be capable of operating in the manner intended by management. This means that if an asset is available for use, but management chooses to delay deploying the asset, it still needs to be depreciated from the date it was in the location and condition necessary to operate as management intended.

Error 4Depreciation on PPE items deferred until the asset is fully operational, i.e. after it is ‘available for use’. |

Error 5 – Stopping depreciation too early

As noted in Error 4 above, it is acceptable to depreciate PPE either during the period that the asset is expected to be ‘available for use’ by the entity (i.e. time-based method), or by referring to the number of production units expected to be obtained (i.e. usage method).Preparers are sometimes unaware of the requirements to continue depreciating PPE, even when the asset becomes idle or is retired from active use. This could result in an understatement of the depreciation charge, and an overstatement of profits, particularly where the depreciation method chosen is time-based. If a usage method of depreciation is applied, it is possible to have a lower, or NIL depreciation charge during the period when a machine is idle, or not operating at full capacity.

| Depreciation of an asset begins when it is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management. Depreciation of an asset ceases at the earlier of the date that the asset is classified as held for sale (or included in a disposal group that is classified as held for sale) in accordance with IFRS 5 and the date that the asset is derecognised. Therefore, depreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated. However, under usage methods of depreciation the depreciation charge can be zero while there is no production. IAS 16, paragraph 54 PBE IPSAS 17, paragraph 71 |

Note: Where assets become idle, this is an impairment indicator in IAS 36 Impairment of Assets, paragraph 12(f) (or PBE IPSAS 21 Impairment of Cash-Generating Assets, paragraph 27 and PBE IPSAS 26 Impairment of Cash-Generating Assets, paragraph 25), and an impairment test is required.

Error 5Cease depreciating PPE items when asset becomes idle or retired from active use. |

Error 6 – Some types of land do need to be depreciated

Land is generally considered to have an unlimited useful life, and is therefore not depreciated. However, for some types of land, such as quarries and sites used for landfill, the economic benefits will be consumed over a finite period. Failing to depreciate these land types could overstate profits during the asset’s life, and understate profits in the period in which the land is eventually impaired.

Error 6Not depreciating land with a finite life. |