NZ IFRS 18: A (re)focus on specified main business activities

NZ IFRS 18: A (re)focus on specified main business activities

Under NZ IFRS 18, all entities will have to change the way they classify expenses in the statement of profit or loss, allocating them to one of five categories: investing, financing, income taxes, discontinued operations and operating (click here for our initial March 2025 article for further information).

A full list of the previous articles in our NZ IFRS 18 series is provided at the end of this article.

In this month’s article, we have a further in-depth look at the concept of specified main business activities (‘SMBA’) introduced by NZ IFRS 18, including:

- What are SMBAs?

- Why is determining an entity’s SMBAs the first step in applying NZ IFRS 18?

- How are SMBAs determined?

- Where it can get complicated (i.e., large Groups with separate reporting obligations (in different jurisdictions)).

What are SMBAs?

This application area was addressed previously in our April 2025 article (click here), but in summary SMBA is a concept that is specific to NZ IFRS 18.

NZ IFRS 18 has a ‘general’ application requirement in terms of where items of income and expenditure are to be presented.

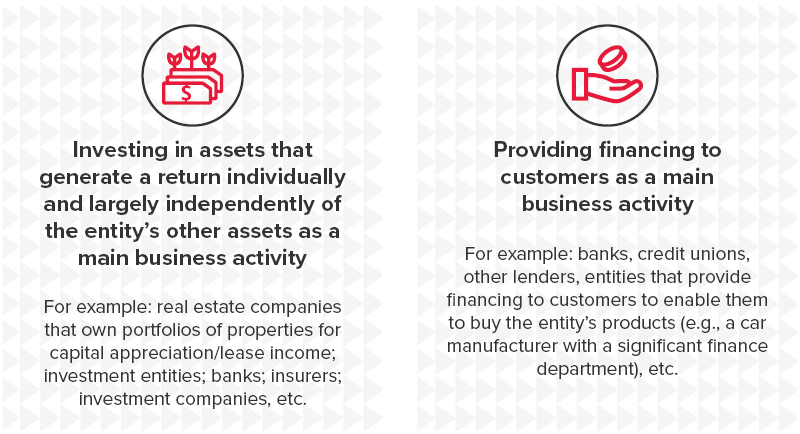

However, noting that all entities are not created (and assessed) equally, NZ IFRS 18 creates alternate presentation exceptions for certain types of entities – i.e., those that are determined to have one and/or two of the SMBA under NZ IFRS 18:

Why is determining an entity’s SMBAs the first step in applying NZ IFRS 18?

Once an entity has determined that is has a SMBA, there will be different parts of NZ IFRS 18 that will need to be applied to certain items.Therefore, an entity needs to know what parts of NZ IFRS 18 are relevant, and which parts need to be disregarded.

Applying the wrong parts of NZ IFRS 18 will most likely result in a materially misstated profit or loss statement.

How are SMBAs determined?

Whether or not an entity has a SMBA is not a option, or accounting policy choice.

NZ IFRS 18 makes it clear that whether (or not) and entity has an SMBA it is a matter of fact, and must be supported by evidence.

While a ‘main business activity’ is not defined in NZ IFRS 18, NZ IFRS 18 provides guidance to be considered, including the following two sources of evidence:

1. Use of subtotals as an indicator of operating performance (including indicators used outside of the financial statements)

- While NZ IFRS 18 does not prescribe specific subtotals that conclusively demonstrate the existence of a specified main business activity, nevertheless, subtotals similar to ‘gross profit’ are commonly used in some industries.

- For example, banking and lending institutions often use a subtotal of interest income less interest expense (commonly referred to as ‘net financial margin’ or ‘net interest income’).

- Similarly, subtotals such as net investment returns may indicate an entity’s focus on investing in particular classes of assets.

- The use of such subtotals in both external and/or internal communications may also indicate that an entity has SMBAs.

2. Operating segments (identified under NZ IFRS 8 Operating Segments)

| Note: While many Tier 2 NZ IFRS (RDR) reporters have an exemption from the disclosure requirements of NZ IFRS 8, the principles of NZ IFRS 8 must still be applied when determining an entity’s cash-generating-units for the purposes of impairment testing under NZ IAS 36 Impairment of Assets. (‘Each unit or group of units to which the goodwill is so allocated shall… not be larger than an operating segment as defined by paragraph 5 of NZ IFRS 8 Operating Segments before aggregation’) That is, NZ IFRS (RDR) reporters must still consider this source of information when determining whether they have SMBA. |

- If a reportable segment comprises a single business activity, this indicates that the performance of the reportable segment is an important indicator of the entity’s operating performance and that the business activity of the reportable segment is a main business activity.

- If an operating segment comprises a single business activity, this indicates that the business activity might be a main business activity of the entity if the performance of the operating segment is an important indicator of the entity’s operating performance.

Where it can get complicated in practice?

The assessment of SMBA is undertaken at the ‘reporting entity’ level.For some entities, particularly those, within a wider corporate group that undertakes similar business activities, the conclusion might be consistent across the group.

For others, however, the conclusion may change as the analysis moves up the corporate structure and incorporates additional entities.

Entities, therefore, need to be aware that:

- The group to which they belong may comprise different main business activities, some of which may be specified and some not, and

- Individual entities and subgroups within the wider corporate group may be required to present their profit or loss statement differently under NZ IFRS 18 as compared to the way the entire group presents its consolidated profit or loss statement under NZ IFRS 18.

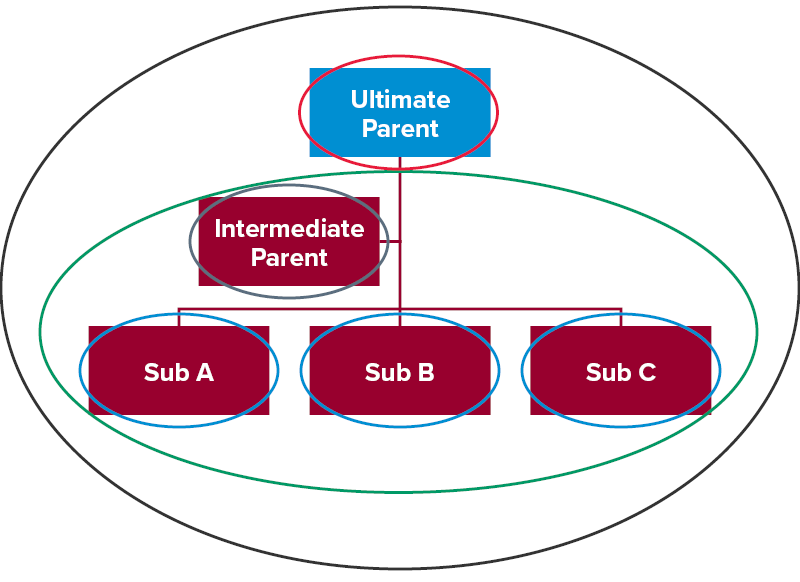

Step 1 – Identify reporting structureAs a first step in assessing specified main business activities, a group should identify its reporting structure and determine whether it prepares:

The adjacent diagram depicts the high-level implications of these decisions. Note that each circle represents a separate reporting entity, and therefore, a separate assessment of the entity’s main business activity is required for each. |

|

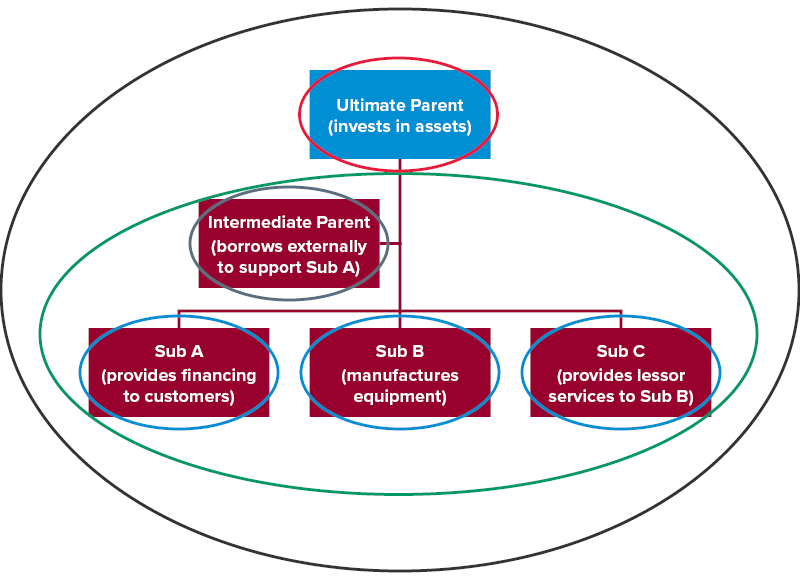

Step 2 – Identify SMBAs within the reporting structureHaving identified all reporting entities within the group, the next step is to assess whether any of those entities have one or both of the specified main business activities.Each circle in the following diagram represents a separate reporting entity, and therefore, a separate assessment of the relevant entity’s main business activity is required. |

|

Based on the diagram above, it might be concluded that:

- Sub A and Intermediate Parent both have the SMBA of providing financing to customers

- Sub B and Sub C have no specified main business activities

- Ultimate Parent has a specified main business activity of investing in subsidiaries.

- The sub-group comprising Intermediate Parent and its subsidiaries (i.e.: Sub A, Sub B and Sub C) does not have a SMBA because providing financing to customers is not currently considered to be an important component of the operating performance of the sub-group as a whole, and

- The group as a whole (i.e., the consolidated results from Ultimate Parent down) does not have a SMBA for the same reasons as outlined directly above.

This analysis can result in different presentation outcomes under NZ IFRS 18, including:

- Presenting different profit or loss statements for the Ultimate Parent, Intermediate Parent and Sub A as compared to Sub B and Sub C, and the group as a whole, and

- Restating the profit or loss presentations used by Ultimate Parent, Intermediate Parent and Sub A in line with those used by Sub B and Sub C and the group as a whole.

Note: For New Zealand entities (Groups) that:

It is important to note that this determination, at this level, may differ from the determination made by the New Zealand entity’s (Group’s) (ultimate) parent, at this level (as illustrated above). That is, a New Zealand entity (Group) should simply not default the SMBA assessment undertaken at the (ultimate) parent, and must always undertake (and document) their own SMBA assessment. Vice versa, this is the same for New Zealand entities (Groups) that have foreign subsidiaries that have their own IFRS 18 (equivalents) reporting in their home jurisdiction. That is, as detailed above, it is possible that there may be different outcomes to the assessment of whether (or not) SMBA are present at the foreign subsidiary(ies) level, and the New Zealand entity (Group) level. |

Why do you need to consider NZ IFRS 18 now?

| Transitioning your financial statement presentation from NZ IAS 1 to NZ IFRS 18 is not a simple exercise. NZ IFRS 18 is not just about reclassifying line items. While this may be the result, how and why an entity gets to those reclassifications is challenging because NZ IFRS 18 is a long and complex standard. Addressing the how and why involves entities making judgements regarding specified main business activities and income and expense categories. These judgements must be documented, supportable and evidenced. In addition, system changes will be required to appropriately tag expenses to the five new categories. Entities should, therefore, start their NZ IFRS 18 implementation projects now in order to be ready to retrospectively restate comparatives from 1 January 2026. Our comprehensive In Practice will help you on your NZ IFRS 18 implementation journey. For more details, including our ‘Six steps to a successful adoption of NZ IFRS 18’, please refer to our Adopting NZ IFRS 18 page. |

Our previous articles on our NZ IFRS 18 series

In our previous articles in our NZ IFRS 18 series, we have looked at application areas related to:- Introduction: what will your profit or loss statement look like under NZ IFRS 18 (click here).

- What is meant by SMBA, and how entities will need to approach making this first, critical determination in applying NZ IFRS 18 (click here).

- How the new investing category in profit or loss of an entity with a SMBA differs from entities with that have no SMBA (click here).

- How the new financing category in profit or loss of an entity with a SMBA of providing financing to customers differs from other entities (click here).

- How foreign exchange gains or losses will need to be disaggregated between the three new categories to be presented in an entity’s Statement of Profit or Loss (i.e., operating, investing, financing) (click here).

- Example of how the Statement of Profit or Loss could look like for a typical retail, wholesale, manufacturer, or service business with no SMBA (click here).

- Illustrative examples: Entities that have a SMBA that is asset investment (click here).

- Illustrative examples: Entities that have a SMBA that is providing finance to customers (click here).

- How entities will be required to reassess how they aggregate, disaggregate, and label line items in the financial statements and notes (click here).

- How entities will be able to present their expenses under NZ IFRS 18, compared to the current requirements under NZ IAS 1 (click here).

Need help

Please contact our Financial Reporting Advisory team for assistance in your entity’s adoption journey of NZ IFRS 18.

For more on the above, please contact your local BDO representative.

This article has been based on an article that originally appeared on BDO Australia, read the original article here.