NZ IFRS 18: How the statement of profit or loss differs when expenses are presented by nature, function, or both

NZ IFRS 18 Presentation and Disclosure in Financial Statements is a new financial statements presentation standard that replaces NZ IAS 1 Presentation of Financial Statements, and is effective for the first time for annual periods beginning on or after 1 January 2027 (with prior periods restated).

Under NZ IFRS 18, all entities will have to change the way they classify expenses in the statement of profit or loss, allocating them to one of five categories: investing, financing, income taxes, discontinued operations and operating (click here for our initial March 2025 article for further information).

A full list of the previous articles in our NZ IFRS 18 series is provided at the end of this article. This includes an article from March 2026 which introduced the feature of NZ IFRS 18 that formally introduces the concept of being able to (in certain circumstances) being able to present expenses both on a by-Function and by-Nature basis (i.e., Hybrid basis)

In this month’s article, we provide further details and examples of this feature of NZ IFRS 18.

Presenting expenses in the operating category by Nature, Function, or both

Unlike NZ IAS 1 Presentation of Financial Statements, NZ IFRS 18 permits a mixed presentation of expenses in the operating category.Entities must classify and present expenses in separate line items to provide the most useful structured summary.

This can be done using one or both of the following characteristics:

- Nature of the expenses, or

- Function of the expenses within the entity.

Example illustrating expenses by nature, by function, or using a mixed presentation

Example 4.4-2 in BDO’s comprehensive In Practice publication shows how the operating category in the statement of profit or loss will differ, depending on whether the entity determines that a by nature, function, or mixed presentation format provides the most useful structured summary of expenses.

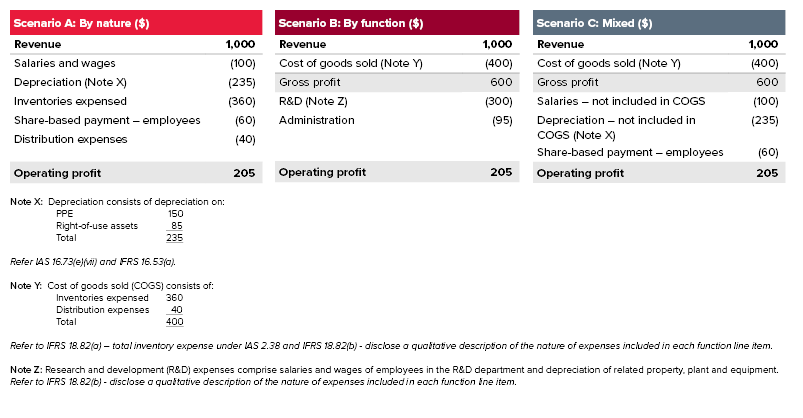

Fact pattern

Retail Entity D has applied the classification requirements of NZ IFRS 18 and classified the following expenses into the operating category (all amounts in thousands of $):- Salaries and wages (NZ IAS 19) 100

- Depreciation (NZ IAS 16) 150

- Inventories expensed (NZ IAS 2): 360

- Distribution expenses (shipping goods to customers): 40

- Share-based payments to employees (NZ IFRS 2): 60

- Depreciation of right-of-use assets (NZ IFRS 16): 85

Entity D also earned $1,000 of Revenue.

Analysis

The diagram below reflects a summary of the operating category in the statement of profit loss, under three mutually exclusive scenarios:- Scenario A: All expenses are presented by nature

- Scenario B: All expenses are presented by function

- Scenario C: Cost of goods sold is presented by function, with all other expenses presented by nature.

|

Note: Retail Entity D does not have a free choice of which presentation method to use. |

There are a few key observations to note regarding the above three scenarios:

- Operating profit is always the same at an amount of $205

- Gross profit in Scenario B and Scenario C is also the same, as that section of the operating category is presented by function in both instances

- Gross profit is an optional additional sub-total. Only ‘operating profit or loss’ is mandatory under paragraph 69(a) of NZ IFRS 18

- Salaries, depreciation and share-based payment expense are the same across both Scenario A and Scenario C, as that section of the operating category is presented by nature in both cases

- As Retail Entity D is a retail entity, it is assumed that ‘cost of goods sold’ comprises the only purchase cost of finished goods inventories ($360) as well as distribution expenses ($40). In other words, there is no manufacturing, and therefore, no allocation of salaries and depreciation to the ‘cost of goods sold’ expense.

Additional points to note - Scenario A: All expenses by nature

The following additional disclosures are required by other NZ IFRS Accounting Standards (if material):- NZ IAS 16 Property, Plant and Equipment, paragraph 73(e)(vii): Disaggregated information about the depreciation expense for each class of property, plant and equipment. Refer to Note X in the diagram above. This is not an IFRS 18 requirement

- NZIAS 2 Inventories, paragraph 36(d): Amount of inventories recognised as an expense during the period (this has been shown on the face of the statement of profit or loss).

However, the disclosures in paragraphs 82 and 83 of NZ IFRS 18 are not required because Retail Entity D is not presenting any line items in the operating category that comprise expenses classified by function.

Additional points to note - Scenario B: All expenses by function

In this scenario, Retail Entity D discloses all its expenses by function, so it must also disclose:- In the ‘cost of goods sold’ line in the statement of profit or loss, the total of inventory expense described in paragraph 38 of NZ IAS 2 (refer paragraph 82(a) of NZ IFRS 18).

- This is the total of:

- Costs previously included in the measurement of inventory that have now been sold.

- Unallocated production overheads and abnormal amounts of production costs of inventories (N/A in this case, as Retail Entity D does not manufacture goods).

- If the circumstances warrant, other amounts, such as for distribution costs

- This is the total of:

- A qualitative (narrative) description of the nature (types) of expenses included in each function line item required by paragraph 82(b) of NZ IFRS 18 (refer to Note Y for the cost of goods sold function and Note Z for the R&D function)

- In a single note, the total for each of the following expenses recognised in the operating category for each function: i.e.

- Depreciation;

- Amortisation;

- Employee benefits;

- Impairment losses and reversals; and

- Write-downs of inventories and reversals.

This disclosure is required by paragraph 83 of NZ IFRS 18 but has not been illustrated here.

Additional points to note - Scenario C: Mixed presentation

If applicable, the relevant additional disclosures referred to in Scenario A and Scenario B must be included, for example:- Total inventory expense and a narrative description of the nature of expenses included in the cost of goods sold function (refer to Note Y above)

- Depreciation disclosures required by NZ IAS 16 (refer Note X above).

However, as Retail Entity D is a retail entity, and it is assumed that there is no manufacturing, and therefore, no allocation of salaries and depreciation to the ‘cost of goods sold’ expense, the additional by nature disclosure of salaries, depreciation, etc. in a single note (paragraph 83) is not required because there is no allocation of these expenses across functions.

Why do you need to consider NZ IFRS 18 now?

|

Transitioning your financial statement presentation from NZ IAS 1 to NZ IFRS 18 is not a simple exercise. |

Previous articles on our NZ IFRS 18 series

In our previous articles in our NZ IFRS 18 series, we have looked at application areas related to :- Introduction: what will your profit or loss statement look like under NZ IFRS 18 (click here).

- What is meant by SMBA, and how entities will need to approach making this first, critical determination in applying NZ IFRS 18 (click here).

- How the new investing category in profit or loss of an entity with a SMBA differs from entities with that have no SMBA (click here).

- How the new financing category in profit or loss of an entity with a SMBA of providing financing to customers differs from other entities (click here).

- How foreign exchange gains or losses will need to be disaggregated between the three new categories to be presented in an entity’s Statement of Profit or Loss (i.e., operating, investing, financing) (click here).

- Example of how the Statement of Profit or Loss could look like for a typical retail, wholesale, manufacturer, or service business with no SMBA (click here).

- Illustrative examples: Entities that have a SMBA that is asset investment (click here).

- Illustrative examples: Entities that have a SMBA that is providing finance to customers (click here).

- How entities will be required to reassess how they aggregate, disaggregate, and label line items in the financial statements and notes (click here).

- How entities will be able to present their expenses under NZ IFRS 18, compared to the current requirements under NZ IAS 1 (click here).

- A (re)focus on Specified main business activities (click here).

Need help

Please contact our Financial Reporting Advisory team for assistance in your entity’s adoption journey of NZ IFRS 18.For more on the above, please contact your local BDO representative.

This article has been based on an article that originally appeared on BDO Australia, read the original article here.