Getting your functional currency right

Getting your functional currency right

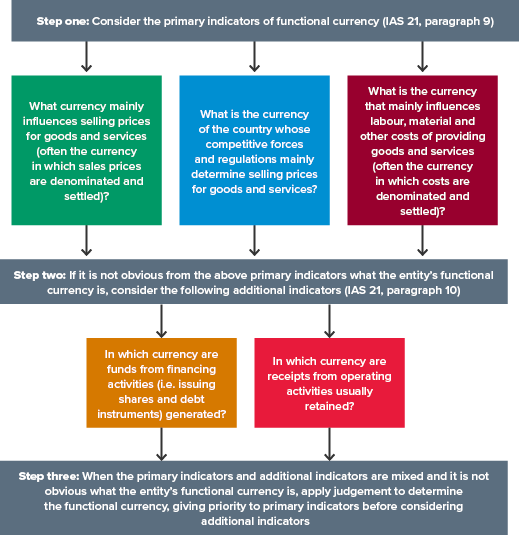

NZ IAS 21 The Effects of Changes in Foreign Exchange Rates requires that each entity to determine its functional currency, whether this be:

- A standalone entity

- An entity with foreign operations (such as a parent), or

- A foreign operation (such as a subsidiary or branch).

Accordingly, NZ IAS 21 requires that for accounting purposes foreign currency items are then translated into the entity’s functional currency.

If however, an entity chooses a presentation currency different from its functional currency (as is permitted by NZ IAS 21), transactions and balances are translated again (i.e., from the functional currency into the presentation currency.

It is important to also note that (consolidated) ‘Groups’ do not have a functional currency.

Rather, their financial statements are presented in their presentation currency, which may or may not be the same as the parent’s functional currency.

With some foreign currency translation differences recognised in profit or loss, and others in other comprehensive income (i.e., foreign currency translation reserves), using an incorrect functional currency can have a significant impact on an entity’s reported results.

In group financial statements, the results and financial position of each individual entity must be translated from their functional currency into the group’s presentation currency.

In this month’s article, we illustrate with examples the application areas that must be considered when an entity is determining the functional currency of an entity:

- Example 1: Functional currency of an individual entity (overseas operations).

- Example 2: Functional currency of an individual entity (local operations).

- Example 3: Functional currency of group entities (Parent holding company with a subsidiary with overseas operations).

- Example 4: Functional currency of an entity that denominates its sales in a foreign currency.

Get in touch with our Financial Reporting Advisory team for assistance

Contact us