When is the appropriate time to derecognise trade receivables and payables settled via electronic b

When is the appropriate time to derecognise trade receivables and payables settled via electronic b

IFRS 9 Financial Instruments, as currently written, is silent on when to initially recognise or derecognise financial assets and liabilities that are not acquired or disposed of in a ‘regular way purchase or sale’. Consequently, there is some diversity in practice as to when an entity should derecognise financial assets and liabilities not disposed of in a regular way sale, with different interpretations as to when the right to receive cash flows has expired, or when an obligation has been discharged.

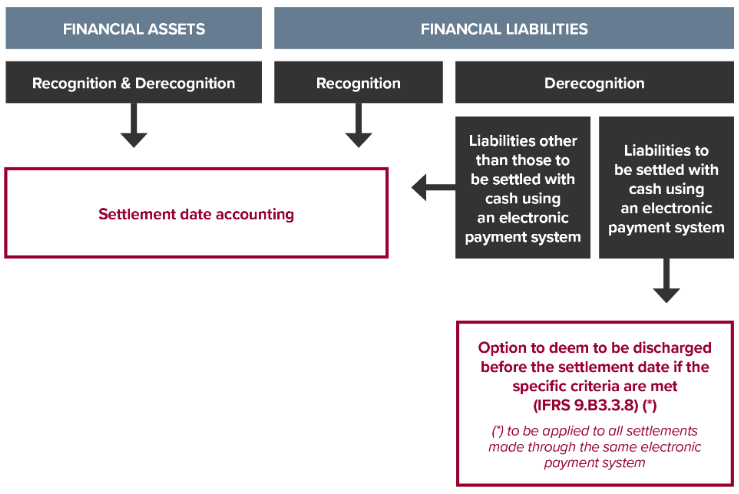

Settlement date will be the date for determining recognition and derecognition

Proposed amendments to IFRS 9 (IASB Exposure Draft: Amendments to the Classification and Measurement of Financial Instruments) clarify that ‘settlement date’ must be used for all acquisitions and disposals of financial assets and financial liabilities that are not acquired or disposed of in a regular way purchase or sale, except when specified criteria are met and the entity elects to apply the exception when derecognising financial liabilities.

1. The recognition of an asset on the day it is received by the entity, and

2. The derecognition of an asset and recognition of any gain or loss on disposal on the day that it is delivered by the entity.

In the case of an entity receiving cash to settle a trade receivable, settlement date would be the date it receives the cash in its bank account, which is the date that the recipient’s rights to the receivable expire.

Similarly, if an entity is paying cash to settle a trade payable, settlement date would be the date when the asset – cash – is credited into the supplier’s bank account, which is the date that the entity’s obligation is extinguished.

The above proposal will result in symmetrical accounting between a debtor and a creditor for the same transaction.

What is the proposed exception for derecognising financial liabilities?

An entity can choose not to apply settlement date accounting, and therefore deem financial liabilities that will be settled with cash using an electronic payment system to be discharged before the settlement date, if all of the following criteria apply:

- The entity has no ability to withdraw, stop or cancel the payment instruction

- The entity has no practical ability to access the cash to be used for settlement as a result of the payment instruction, and

- The settlement risk associated with the electronic payment systems is insignificant.

The diagram below summarises the proposed requirements for derecognising financial assets and financial liabilities.

Implications for entities using an electronic payment system

We do not anticipate significant impacts for entities receiving and paying cash via electronic payments in New Zealand because the clearing system is efficient, and for New Zealand dollar transfers between New Zealand financial institutions, usually settles the same or the following business day. However, we may see asymmetrical accounting between the debtor and creditor as follows:

- The debtor must wait until cash is in its bank account to derecognise the receivable and recognise cash

- The creditor, if they meet the criteria for the exception to settlement date accounting described above, may be able to derecognise the trade payable and corresponding cash balance once the electronic payment has been made.

More information

Please refer to our IFR Bulletin for more information on these proposed amendments to IFRS 9.

Need help?

Please contact our IFRS Advisory team if you require assistance in this regard, or wish to provide comments on these proposals.

For more on the above, please contact your local BDO representative.