Issue 3: Relationships with other entities

In the March 2021 edition of Accounting Alert we started our new series on the top ten financial reporting issues that directors need to consider by examining how to account for unusual events with substantial impacts (such as COVID-19). In the April 2021 edition of Accounting Alert we looked at the second issue, which was selecting accounting policies.

In this article we turn our attention to the third of the ten issues that will typically require the greatest attention by directors – classification of relationships with other entities.

Issue number 3 – relationships with other entities

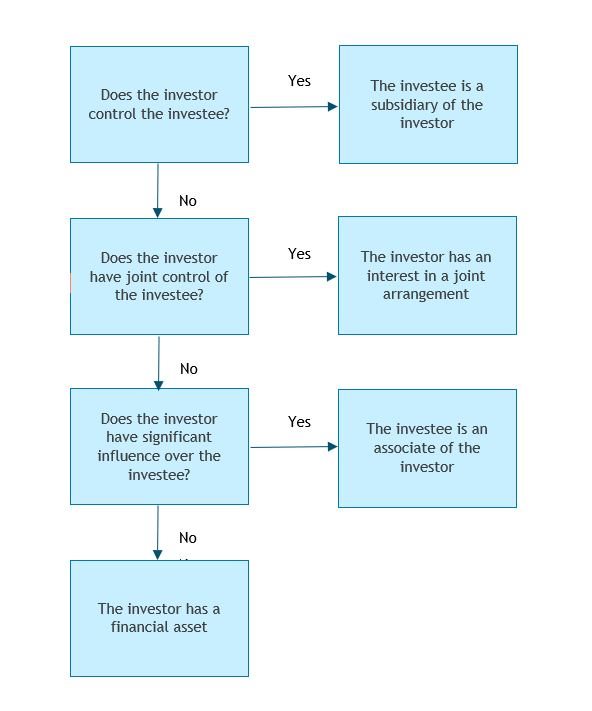

If one entity owns an equity interest in another entity, that equity interest in the other entity can only be accounted for in one of four ways:

- As a subsidiary

- As a joint arrangement

- As an associate

- As a financial asset.

Subsidiaries

When an entity acquires an equity interest in another entity, the first thing that it needs to do is determine whether it controls that entity.

NZ IFRS 10 Consolidated Financial Statements (“NZ IFRS 10”) states that an investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. This means that an investor must have three key things to control an investee:

- Power over the investee

- Exposure, or rights, to variable returns from its involvement with the investee

- The ability to use its power over the investee to affect the amount of the investor’s returns.

An investor has power over an investee when the investor has existing rights that give it the current ability to direct the activities that significantly affect the investee’s returns (which are referred to as the relevant activities).

Examples of relevant activities include:

- Selling and purchasing of goods or services

- Managing financial assets during their life (including upon default)

- Selecting, acquiring or disposing of assets

- Researching and developing new products or processes

- Determining a funding structure or obtaining funding.

Examples of decisions about relevant activities include:

- Establishing operating and capital decisions of the investee, including budgets

- Appointing and remunerating an investee’s key management personnel or service providers and terminating their services or employment.

In assessing whether an investor has power over an investee, the following considerations are relevant:

- An investor does not have to have exercised its power to direct the relevant activities for that power to exist

- Power arises from rights - sometimes assessing power is straightforward (such as when power over an investee is obtained directly and solely from voting rights granted by equity instruments), but in other cases the assessment will be more complex and require more than one factor to be considered (for example, where there are contractual arrangements that are relevant to the consideration of whether power exists)

- An investor that holds only protective rights does not have power over an investee.

Protective rights relate to fundamental changes to the activities of an investee, or apply in exceptional circumstances only. Examples of protective rights include:

- A lender’s right to restrict a borrower from undertaking activities that could significantly change the credit risk of the borrower to the detriment of the lender

- The right of a party holding a non-controlling interest in an investee to approve capital expenditure greater than that required in the ordinary course of business, or to approve the issue of equity or debt instruments

- The right of a lender to seize the assets of a borrower if the borrower fails to meet specified loan repayment conditions).

Where an investor controls an investee, the investee is the investor’s subsidiary and the investor must prepare consolidated financial statements.

Joint arrangements

Where an investor does not control an investee, it must consider if it has joint control of the investee.

NZ IFRS 11 Joint Arrangements states that joint control is the contractually agreed sharing of control of an arrangement by two or more parties and that it exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control. For the purposes of considering whether control exists, the definition of control is the definition that is provided in NZ IFRS 10 (see above).

An arrangement can be a joint arrangement even though not all of its parties have joint control of the arrangement. In such circumstances, joint control only exists where the parties that have joint control are specified. This means, for example, that where there are five parties to an arrangement and four must agree to all decisions made regarding the relevant activities, joint control only exists where the parties that must agree are specified - joint control does not exist where the agreement of any four of the five parties to the arrangement is required for a decision to be made.

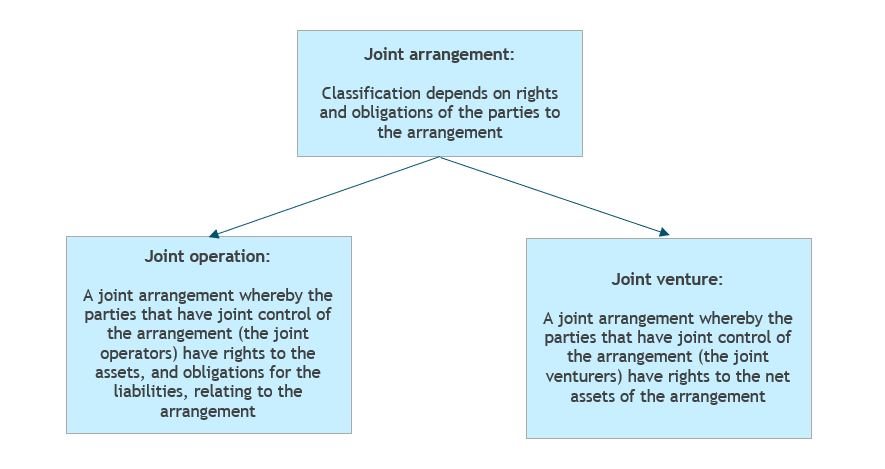

If an investor has determined that it has an interest in a joint arrangement, it must determine whether that joint arrangement is a joint operation or a joint venture. Classification depends on the rights and obligations of the parties to the arrangement, as shown in the diagram below:

- When an entity has rights to the assets, and obligations for the liabilities, relating to the arrangement, the arrangement is a joint operation

- When an entity has rights to the net assets of the arrangement, the arrangement is a joint venture.

When assessing their rights and obligations under an arrangement, the parties to the arrangement should consider the structure of the joint arrangement (i.e. whether it is a separate vehicle). A joint arrangement that is not structured through a separate vehicle is a joint operation.

When a joint arrangement is structured through a separate vehicle, the joint arrangement can be either a joint operation or a joint venture. In such instances, parties to the joint arrangement must also examine the following to determine how the joint arrangement should be classified:

- The legal form of that separate vehicle

- The terms of the binding arrangement

- Where relevant, other facts and circumstances.

The purpose of undertaking such an examination is to determine if the factors outlined above:

| Give the parties to the agreement: | If they do, the arrangement is a: |

| Rights to the assets, and obligations for the liabilities, relating to the arrangement | Joint operation |

| Rights to the net assets of the arrangement | Joint venture |

If a joint arrangement is a joint operation, in its financial statements an investor recognises the following in relation to its interest in the joint operation:

- Its assets, including its share of any assets held jointly

- Its liabilities, including its share of any liabilities incurred jointly

- Its revenue from the sale of its share of the output arising from the joint operation

- Its share of the revenue from the sale of the output by the joint operation

- Its expenses, including its share of any expenses incurred jointly.

If the joint arrangement is a joint venture, the investor accounts for it using equity accounting.

Associates

Where an investor has determined that it does not control, or jointly control, an investee, it must consider if it has significant influence over the investee.

NZ IAS 28 Investments in Associates and Joint Ventures states that significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control of those policies.

If an investor holds, directly or indirectly, 20% or more of the voting power of an investee, it is presumed that the entity has significant influence, unless it can be clearly demonstrated that it does not. Conversely, if the investor holds, directly or indirectly, less than 20% of the voting power of the investee, it is presumed that the investor does not have significant influence, unless such influence can be clearly demonstrated.

The existence of significant influence by an investor is usually evidenced in one or more of the following ways:

- Investor representation on the board of directors or equivalent governing body of the investee

- Investor participation in policy-making processes of the investee, including participation in decisions about dividends or other distributions

- Material transactions between the investor and the investee

- Interchange of managerial personnel between the investor and the investee

- Provision of essential technical information between the investor and the investee.

If the investor has significant influence over the investee the investee is an associate of the investor. An investor accounts for its interest in an associate using equity accounting.

Financial assets

In the investor has determined that its equity investment in an investee does not result in it having control of, joint control of, or significant influence over, the investee, the investment is accounted for as a financial asset.

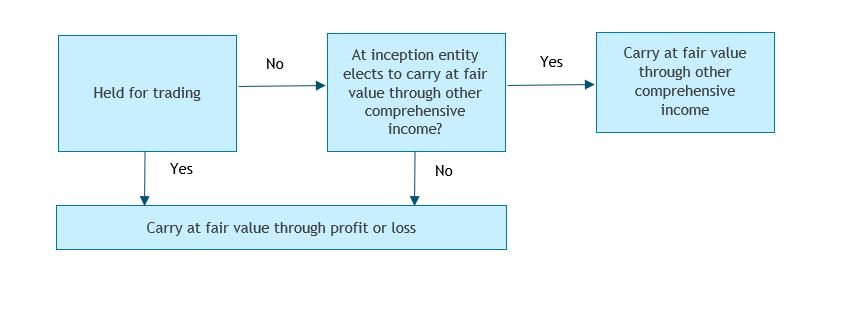

Under NZ IFRS 9 Financial Instruments, where a financial asset is an equity instrument, the default measurement approach is fair value through profit or loss. However, measurement at fair value through other comprehensive income is permitted if the investment is not held for trading and the investor makes an irrevocable election at initial acquisition to classify the instruments as fair value through other comprehensive income.

The following flow chart shows how financial assets that are equity instruments are classified under NZ IFRS 9:

Summary

The following flowchart summarises the manner in which an investor classifies an equity investment in an investee:

In many instances, the determination of the nature of a relationship between an investor and its investee is straightforward. However, in some instances it can be complex and the classification of that relationship can require the extensive analysis of all facets of the relationship between the two parties and the application of considerable professional judgement.

In future editions of Accounting Alert, we’ll continue with our examination of the top 10 issues that directors need to consider.

For more information on the above, please contact your local BDO representative.

This publication has been carefully prepared, but is general commentary only. This publication is not legal or financial advice and should not be relied upon as such. The information in this publication is subject to change at any time and therefore we give no assurance or warranty that the information is current when read. The publication cannot be relied upon to cover any specific situation and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact the BDO member firms in New Zealand to discuss these matters in the context of your particular circumstances.

BDO New Zealand and each BDO member firm in New Zealand, their partners and/or directors, employees and agents do not give any warranty as to the accuracy, reliability or completeness of information contained in this article nor do they accept or assume any liability or duty of care for any loss arising from any action taken or not taken by anyone in reliance on the information in this

Subscribe to receive the latest BDO News and Insights

Subscribe