Is this relevant to me

This “Cheat Sheet” will be relevant to you if:

- Your entity is a for-profit entity

- Your entity currently prepares (or will be required to prepare) financial statements under NZ IFRS, or NZ IFRS (RDR)

- Your entity has revenue streams that are required to be recognised over-time, relating to items that are being constructed under existing, or anticipated, sales contracts with customers.

- Borrowing costs have historically been capitalised to such items being constructed (i.e. work-in-progress).

What might the Cheat Sheet might reveal?

This “Cheat Sheet” might reveal that:

- Your entity may no longer be permitted to capitalise borrowing costs to such items upon transition to the new revenue standard, applying NZ IFRS 15 Revenue from Contracts with Customs (NZ IFRS 15).

- Consequentially, in applying NZ IFRS 15 Revenue from Contracts with Customs for the first time, you may have to “unpick” previous periods accounting treatment – i.e. where borrowing costs were previously capitalised.

If the numbers in the financial statements are required to change, management will need to consider the consequential impacts to areas such as bank covenants, staff bonuses, and earn-out clauses etc.

Need Assistance with assessing the impact?

BDO IFRS Advisory is a dedicated service line available to assist entities in transitioning to new accounting standards. Further details are provided on the following pages for your information.

Background

In March 2019, BDO released a Cheat Sheet detailing the impending impact of NZ IFRS 15 with respect to over-time recognition.

One of the key changes highlighted was that under NZ IFRS 15, the recognition of work-in-progress assets (representing deferred construction and other input costs) will in most cases fall away, as the previous percentage-of-completion method of accounting is not carried over in NZ IFRS 15. This means that in most cases the only assets that an entity would have on its balance sheet relating to over-time revenue streams would be receivable balances due from the customer.

Subsequent to the release of this Cheat Sheet, the IFRS Interpretations Committee (IFRIC) issued a decision regarding the treatment of borrowing costs related to items that are being constructed under existing, or anticipated, sales contracts, which are required to be recognised over-time under NZ IFRS 15.

The decision as issued has a significant impact on an entity’s ability to capitalise borrowing costs under such contracts.

As NZ IFRS 15 is required to be applied retrospectively, this decision may require an entity “unpick” its previous accounting treatment of capitalising borrowing costs when in transitions to NZ IFRS 15.

So what has changed and what do I need to be aware of?

Borrowing costs are only able to be capitalised to “qualifying asset [1]”, as defined by NZ IAS 23 Borrowing Costs.

However when revenue is recognised over-time under NZ IFRS 15, the only “assets” in the balance sheet are trade receivables, and perhaps a contract asset (representing the difference where the aggregate Revenue recognised to-date exceeds the aggregate Trade receivables recognised to-date).

The question put to the IFRIC was, in this situation, do the assets recognised in the balance sheet related to these contracts meet the definition of a “qualifying asset”, such that borrowing costs can (continue to be) capitalised?

Without getting into the technical “nitty gritty” the answer of the IFRIC was “No, they are not”.

This decision even extends to, for example, the construction of property where the entity’s business operation is to enter into sale and purchase agreements (S&PA) for the sale of property under construction, even if the S&PA is entered into mid-construction (i.e. when the construction costs would have been recognised as Inventory (WIP) in the balance sheet up until this point in time).

So what is the impact really?

The impact of this decision is significant.

It essentially means that:

- Borrowing costs for such arrangements are recognised as a financing expense (outside of gross margin), rather than being capitalised and eventually recognised with cost of sales (i.e. within gross margin).

This will impact an entities EBIT and EBITDA numbers, and as such management will need to consider the consequential impacts to areas such as bank covenants, staff bonuses, and earn-out clauses, etc. - When transitioning to NZ IFRS 15 for the first time, as many entities will be doing this year, previously capitalised interest for such arrangements will need to be “unpicked” from comparative periods.

This may require significant time and cost for management and finance teams to execute.

Also, in instances where the entity elects to transition to NZ IFRS 15 using the Cumulative Effect Method (i.e. where comparatives are not restated) there is an additional transition disclosure requirement to present what the current year numbers would have been under the previous treatment (i.e. where WIP was being recognised, and borrowing costs capitalised to these).

Again, this may require significant time and cost for management and finance teams to execute.

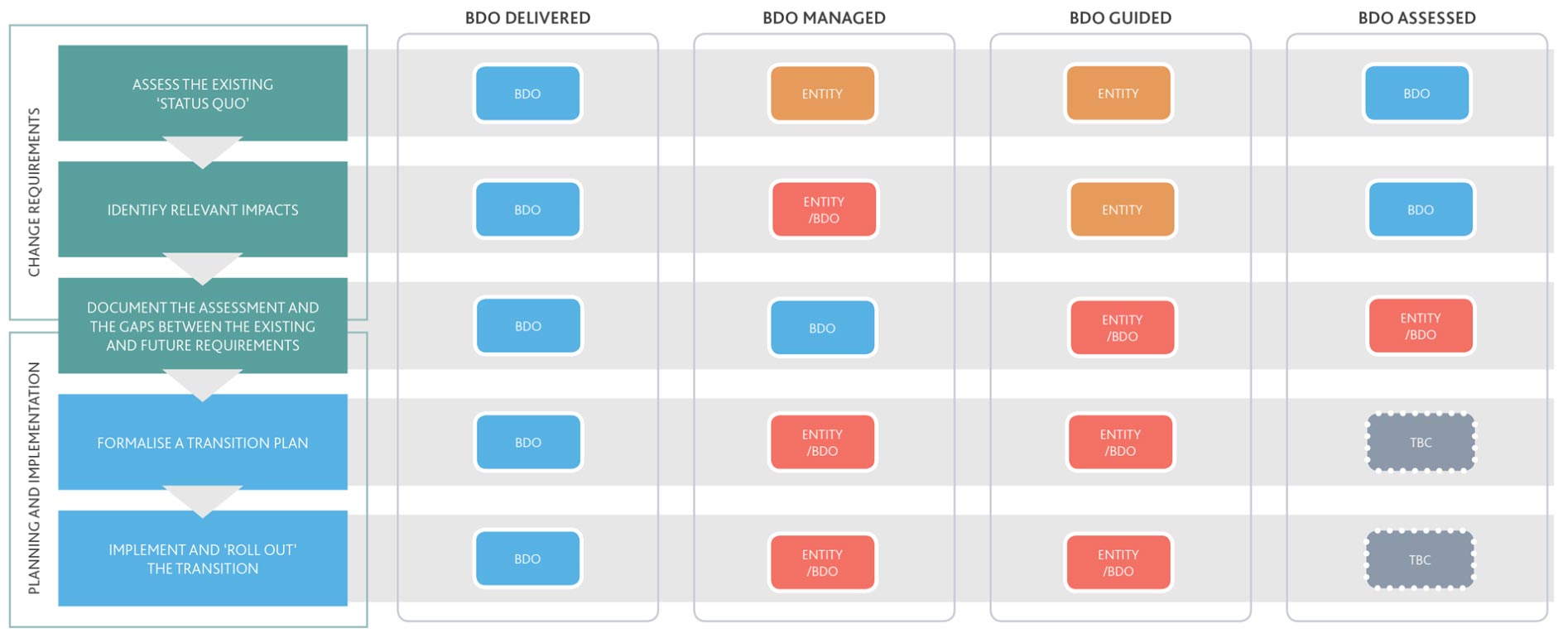

BDO IFRS Advisory – Tailored Transition Assistance

BDO’s adopts a flexible approach to assisting entities with their transition to new accounting standards and pronouncements, meaning we can be as involved as an entity requires, based on their own in-house resourcing and expertise at their disposal.

Often entities don’t know exactly where to start or focus their energies, and just want to get the ball rolling.

We have found our BDO Guided and BDO Assessed approaches fit well to accommodate this, whilst also retaining the ability to scale up involvement quickly if need be – either way, we work WITH you.

For more information as to how BDO IFRS Advisory might assist with assessing the impact of your transition to NZ IFRS and any other new accounting standards please contact James Lindsay or visit our IFRS Advisory homepage.

[1] Qualifying assets are assets that necessarily takes a substantial period of time to get ready for its intended use or sale (NZ IAS 23 para 5)