For reporting dates 31 December 2019 and onwards, including the upcoming 31 March 2020 and 30 June 2020 reporting season, the long awaited new accounting standard on leases (NZ IFRS 16 Leases) comes into effect for for-profit entities who apply NZ IFRS.

As we have covered in previous Cheat Sheets, NZ IFRS 16 results in a fundamental change in the way that lessees will need to account for most of their lease agreements.

In our experience, one often overlooked area of the new requirements is how to account for s leases that have been acquired in business combinations.

This is because this accounting treatment is not detailed in NZ IFRS 16. Instead you need to look to the updated version of NZ IFRS 3 Business Combinations (paragraphs 28A and 28B) to account for the acquired leases.

This Cheat Sheet has been produced as a high-level overview of the requirements of the “reset accounting” that must be applied to leases that have been acquired in a business combination.

Need assistance with your adoption of NZ IFRS 16?

BDO IFRS Advisory is a dedicated service line available to assist entities in adopting NZ IFRS 16, contact our team to see how we can help.

What is covered in the Cheat Sheet?

In order to navigate through this area of lease accounting, this Cheat Sheet is broken down into the following sections:

"Business combinations” and acquiring lease

“Business combinations” are transactions that gives one party (the acquirer) control of a “business” (as defined by NZ IFRS 3).

Broadly speaking, these transactions take one of two forms:

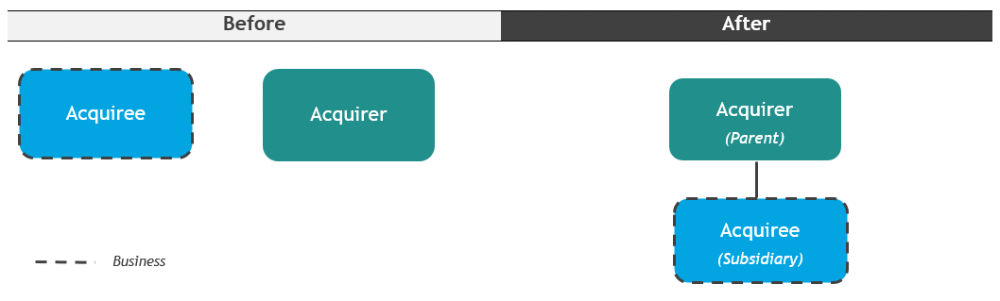

- Majority share buy-outs: Acquisition of the majority of an entity’s[1] (acquiree’s) voting interests (i.e. shares), such the entity continues on as a going concern in its original form as a controlled entity (subsidiary) of the acquirer.

Contracts and agreements associated with the acquired business (including leases) remain in the name of the acquiree (now a subsidiary of the acquirer)

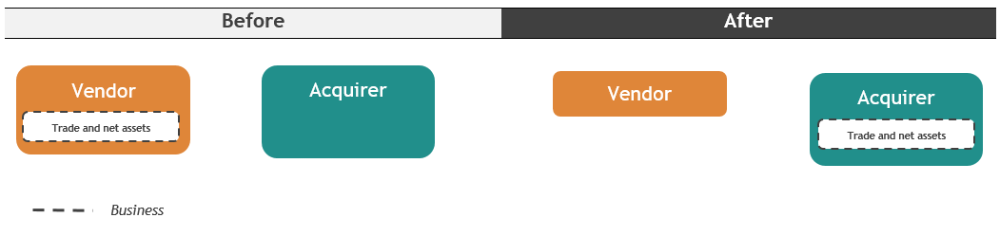

- Trade and net-asset buy-outs: Acquisition of an existing entity’s (vendor’s) trade and net assets - that is, the “business” is carved out of the vendor and re-established in the acquirer.

Contracts and agreements associated with the acquired business (including leases) must be (legally) assigned over to be in the name of the acquirer, from previously being in the name of the vendor.

[1] Provided that the entity itself meets the definition of a “business”, per NZ IFRS 3 – not all entities meet the definition of a business, particularly those that have no (or limited) inputs and/or processes (such as “shell companies”).

What are the key accounting areas to address with leases acquired in a business combination?

When leases are acquired in a business combination, their accounting treatment is “reset” as if they were brand new leases as at acquisition date in the (consolidated) financial statements of the acquirer.

This means that any previous lease liability or right-of-use assets previously recognised by the acquiree/vendor is not simply “rolled up” into the acquirer.

To explain further, the areas of the “reset accounting” that acquirers will need to take note of are detailed below.

(a) Discount rate (used to present value future lease payments)

From our previous Cheat Sheet Applying Discount Rates under the New Lease Standard (NZ IFRS 16) you will recall that the discount rate is determined at a lease’s commencement date (or adoption date[1]), and must incorporate four key parameters: (i) jurisdiction; (ii) asset type; (iii) lease term; and, (iv) amount.

Accordingly, the application of “reset accounting” for acquired leases may mean that discount rates that may have been previously determined and applied by the acquiree/vendor may no longer be appropriate.

(i) As at what date?

“Reset accounting” requires the discount rate to be (re)determined as at the acquisition date.

Therefore, the economic conditions present at acquisition date may have changed from those that existed at the date the original discount rate was previously determined (i.e. commencement (adoption) date).

(ii) What lease term- and amount - parameters are used?

“Reset accounting” requires the discount rate to be determined based on the remaining lease term (iii) and remaining lease payments (iv) from acquisition date, rather than the original lease term and original lease payments that existed at commencement (adoption) date.

Because leases will be part way through their terms as at acquisition date, both (iii) and (iv) will have changed, and this must be taken into account when the discount rate is determined at acquisition date - depending on whether the acquirer determines it is likely to make use of renewal options that the acquiree/vendor did (or did not) include in determining the lease term.

(iii) Whose discount rate is determined?

The discount rate is based on the entity that is the contractual lessee subsequent to the business combination.

Accordingly, the “form” that the business combination takes will determine which entity’s discount rate is being determined at acquisition date:

- Majority share buy-out: The acquiree’s

- Trade and net asset buy-out: The acquirer’s.

(b) Adjustments for favourable or unfavourable lease terms

As has been previously required under NZ IFRS 3, an acquirer is required to recognise amounts that reflect the inherent benefit (or not) of when the terms of acquired leases are more (or less) favourable than that of market lease terms that exist as at acquisition date.

However, rather than recognising this as a separate item in the acquirer’s balance sheet as has been done previously, any such amounts are now recognised as adjustments against the right-of-use asset as at acquisition date.

[1] Or, the date of adoption to NZ IFRS 16 if the acquiree/vendor previously utilised the Modified Retrospective Method when adopting to NZ IFRS 16.

What are the practical consequences of “reset accounting”?

(a) Discount rates to be used

From the above, it should be clear that (for various reasons) the discount rates that may have previously been applied to acquired leases by the acquiree/vendor will likely no longer be appropriate when the acquirer applies “reset accounting”.

(b) Impact to goodwill that arises in a business combination

The good news is that NZ IFRS 16 does not introduce any new impacts to goodwill arising in a business combination that did not already exist previously.

Accordingly, provided that there is no adjustments for favourable or unfavourable lease terms as at acquisition date, the lease liability or right-of-use assets are recognised in equal and opposite amounts, meaning that there will be no net impact to goodwill.

(c) Multiple “lease books” required (for majority share buy-outs)

“Reset accounting” is only applied in the (consolidated) financial statements of the acquirer.

Accordingly, when the business combination takes the form of a majority share buy-out, the accounting previously applied by the acquiree continues in the acquiree’s own financial statements (i.e. the accounting is not “reset” at this level of the reporting group).

This means that the acquirer will need to establish a separate lease schedule to reflect the “reset accounting”, to be incorporated into its consolidated financial statements as an on-going consolidation adjustment (i.e. backing-out the acquiree’s lease accounting treatment, and (re)inserting the “reset accounting” treatment).

BDO IFRS Advisory – Tailored Adoption Assistance

BDO adopts a flexible and fully customisable approach to assisting entities with their adoption of new accounting standards. This allows us to be as involved as an entity requires, so that this can be built around an entity’s own existing in-house resourcing and expertise.

Often entities have an idea of what needs to be done, but don’t know exactly where to start or focus their energies, and just want to get the ball rolling.

We have found our BDO Guided and BDO Assessed approaches fit well to accommodate this, whilst also retaining the ability to scale up involvement quickly if need be – either way, we work WITH you.

Members of BDO’s IFRS Advisory department come ready with real life experience in adopting NZ IFRS 16 and are therefore well placed to provide entities with the expertise and assistance they require.

For more information as to how BDO IFRS Advisory might assist with assessing the impact of your adoption to new accounting standards please contact James Lindsay at BDO IFRS Advisory and visit our IFRS Advisory page.