Convertible notes - Are you accounting for these correctly (Part 8)?

In the current economic climate, we continue to see different types of convertible note arrangements, typically entered into by companies needing to offer attractive returns in order to obtain funds from lenders and investors.

Over the past few months we have been looking at some practical aspects regarding accounting for convertible notes, including:

- An overview of the requirements (in the April 2018 edition of Accounting Alert)

- A detailed example of a convertible note classified as a compound financial instrument (in the May 2018 edition of Accounting Alert)

- A detailed example of a convertible note with an embedded derivative liability (in the mid-June edition of Accounting Alert)

- Common scenarios encountered in practice where conversion features either meet or fail equity classification (in the July 2018 edition of Accounting Alert)

- A detailed example of a convertible note converting into a variable number of shares based on the issuer’s share price at conversion date (in the August 2018 edition of Accounting Alert).

- A detailed example of a convertible note issued in a currency other than the issuer’s functional currency (in the September 2018 edition of Accounting Alert).

- A detailed example of a convertible note with a feature that allows the issuer to repay (call) the note early (in the October 2018 edition of Accounting Alert).

As noted in these previous articles, in order for a conversion feature to be classified as equity, the fixed for fixed test in IAS 32 Financial Instruments: Presentation (“IAS 32”) must be met (i.e. at initial recognition, the conversion feature gives the holder of the convertible note the right to convert into a fixed number of equity securities of the issuer).

|

This month we look at a detailed example of a convertible note with an early repurchase option. |

Summary

Some convertible notes allow the issuer to repurchase the note before its stated maturity date, if certain events occur. If the issuer does elect to repurchase the note before its stated maturity date, IAS 32 requires the consideration paid (i.e. repurchase price) to be allocated to the liability and equity components. This is achieved by:

- Determining the fair value of the liability at the repurchase date

- The residual amount is attributed to the equity component, and

- The difference between the carrying amount and the fair value of the liability at the repurchase date is accounted for as the cost of redeeming the liability.

The example below illustrates this approach in more detail.

Example: Early repurchase of bonds

XYZ Limited issues a convertible note with a face value $10,000, maturing three years from its date of issue.

The note pays a 10% annual coupon and, on maturity, the holder has an option either to receive cash of $10,000 or 10,000 XYZ Limited shares.

At the end of Year 2, XYZ Limited is subject to a takeover offer and elects to repurchase the note for $11,000. Assume the following:

- Carrying value of the note at the end of Year 2 is $9,840

- The market interest rate for a note without a conversion feature at the end of Year 2 is 10%.

Analysis – initial recognition

This convertible note is accounted for as a compound financial instrument because the conversion feature gives the holder of the convertible note the right to convert into a fixed number of equity securities of the issuer (refer to the example in the May 2018 edition of Accounting Alert).

Analysis – early repurchase

Paragraph AG33 of IAS 32 requires an entity to allocate the consideration paid for the repurchase to the liability and equity components using the same allocation method as the method for allocating the initial transaction price (i.e. determine the fair value of the liability component, with the residual amount being allocated to equity).

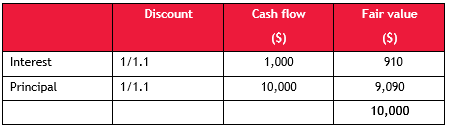

The fair value of the outstanding liability at the end of year 2, after payment of interest for that year, is set out in the table below. It is calculated as the present value of the outstanding cash flows (for one remaining year) at the market interest rate at the end of year 2 (i.e. 10%).

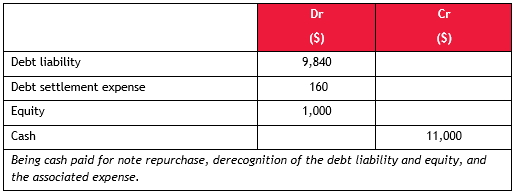

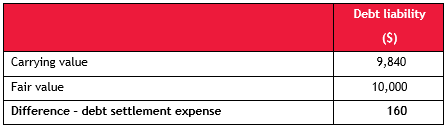

The repurchase consideration paid to the holder is $11,000 and the fair value of the liability component is $10,000 as determined above, therefore the value assigned to the equity component is $1,000.

The difference between the carrying value and the fair value of the debt liability at the end of year 2 is accounted for as the cost of redeeming the debt.

The journal entry on repurchase of the note at the end of Year 2 is: