Common errors when accounting for property, plant and equipment (IAS 16 and PBE IPSAS 17 – Part 2)

Even though IAS 16 Property, Plant and Equipment (“IAS 16”), for Tier 1 and Tier 2 for-profit entities, and PBE IPSAS 17 Property, Plant and Equipment (“PBE IPSAS 17”), for Tier 1 and Tier 2 public benefit entities (“PBEs”), are “easy” standards to apply, last month our Common Errors article identified nine common errors preparers could make when determining which types of property, plant and equipment (“PPE”) fall within the scope of IAS 16/PBE IPSAS 17, which are instead accounted for under other accounting standards, and when working out the cost of an item of PPE.

This month we continue with IAS 16/ PBE IPSAS 17 and look at typical mistakes made when measuring PPE using either the cost or revaluation model for subsequent measurement.

Common error 1 – Cost or revaluation models not applied consistently across classes of PPE

After initial recognition, IAS 16, paragraph 29 (PBE IPSAS 17, paragraph 42) allows you to measure items of PPE using either the cost or revaluation model as your accounting policy. However, the caveat is that the particular policy chosen must be applied consistently to an entire class of PPE.

|

An entity shall choose either the cost model in paragraph 30 or the revaluation model in paragraph 31 as its accounting policy and shall apply that policy to an entire class of property, plant and equipment. IAS 16, paragraph 29 PBE IPSAS 17, paragraph 42

IAS 16, paragraph 37

PBE IPSAS 17, paragraph 52 |

Paragraph 37 of IAS 16 (paragraph 52 of PBE IPSAS 17) explains that a class of PPE is a grouping of assets of a similar nature and use in the entity’s operations, and provides some examples of what is meant by a class of PPE; however, it is not precise and judgement must be applied.

The rule of thumb is that a class is generally the level at which separate disclosures are provided about the items in the financial statements.

Example:

Entity A has the following buildings:

-

Office premises

-

Manufacturing facility in Auckland, and

-

Warehouse and distribution facilities in the North Island and the South Island.

While these buildings may have a similar nature, they each have a different use in the business and therefore it could be argued that there are three classes of buildings. However, it is unlikely that the geographic dispersion of the warehouse and distribution facilities would result in the facility in each island being considered to be a separate class of building.

Identifying classes of PPE at too low a level could result in inconsistent accounting of similar items, with some being measured at cost and some at fair value.

|

Common error 1 Identifying classes of PPE at too low a level, resulting in a mix of measurement models being used for items with a similar nature and use. |

Common error 2 – Not keeping revaluations up to date

Once the revaluation model has been chosen for a particular asset class, IAS 16 and PBE IPSAS 17 require that revaluations are kept up to date so that at each reporting date, there is no material difference between carrying amount and fair value.

|

After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluations shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period/at the reporting date. IAS 16, paragraph 31; PBE IPSAS 17, paragraph 44 |

This does not necessarily mean that an external, independent valuation need be performed at each reporting date. However, directors and preparers need to satisfy themselves, based on current information available to market participants, that fair value has not moved by a material amount. A common error occurs when directors and preparers assume that there are no revaluation movements to be recognised between the dates of external valuations.

|

Common error 2 Applying a fixed schedule of independent revaluations (say every three to five years) without further consideration of movements in asset fair values. |

Common error 3 – Recognising revaluation increments in profit or loss

While not as common because it is spelt out so clearly in the standard, we have seen common errors where revaluation increments are recognised in profit or loss/surplus or deficit instead of other comprehensive income/comprehensive revenue and expense (asset revaluation surplus) when they are not reversing a previous revaluation decrement. This is a very obvious, biased error, and can significantly overstate profits of an entity.

|

If an asset’s carrying amount is increased as a result of a revaluation, the increase shall be recognised in other comprehensive income and accumulated in equity under the heading of revaluation surplus. However, the increase shall be recognised in profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognised in profit or loss. IAS 16, paragraph 39 PBE IPSAS 17, paragraph 54 |

Directors and preparers should perform a sanity check on revaluation movements recognised in profit or loss/surplus or deficit and reconcile all credits to profit or loss/surplus or deficit against previous decrements.

|

Common error 3 Recognising revaluation increments (credits) in profit or loss/surplus or deficit when they do not reverse a previous revaluation decrement. |

Common error 4 – Offsetting revaluation increments and decrements across a class of assets

IAS 16, paragraphs 39 and 40 make it clear that increases and decreases in the fair value of an item of PPE measured using the revaluation model can only be offset for the particular asset, and not within the class of assets being revalued.

|

If an asset’s carrying amount is increased as a result of a revaluation, the increase shall be recognised in other comprehensive income and accumulated in equity under the heading of revaluation surplus. However, the increase shall be recognised in profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognised in profit or loss. IAS 16, paragraph 39 IAS 16, paragraph 40 |

In Common error 1 above we explained that a class of assets is a grouping of assets with a similar nature and use to the entity.

Example

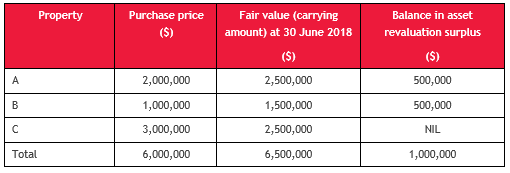

XYZ Entity acquired three properties (A, B and C) in 2017 and these fall into the class called “Land and buildings”.

For the year ended 30 June 2018, the fair values of property A and B increase, but fair value for property C.

A common error occurs if we assume that the excess fair value for the class of $500,000 ($6,500,000 - $6,000,000) is the balance in the asset revaluation surplus. IAS 16, paragraph 39 requires the increments in fair value for properties A and B to be recognised in other comprehensive income (asset revaluation surplus) and the decrement for property C to be recognised in profit or loss. Fixed asset registers therefore need to track, for each asset, movements into and out of the revaluation reserve.

|

Common error 4 Offsetting revaluation increments and decrements across a class of assets rather than for each individual asset. |

*Note for public benefit entities:

Accounting for revaluation increments and decrements is different for public benefit entities. PBE IPSAS 17 requires revaluation increments and decrements to be offset within a class of assets (paragraphs 54 to 56). Offsetting between classes of assets is, however, forbidden (PBE IPSAS 17, paragraph 56).

Common error 5 – Recycling the balance in the asset revaluation reserve to profit or loss/surplus or deficit when the asset is sold

A common error occurs where the balance in the asset revaluation reserve is derecognised via profit or loss/surplus or deficit when the underlying asset is sold.

|

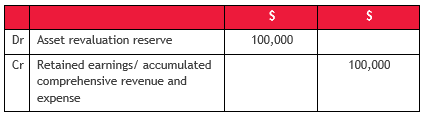

The revaluation surplus included in equity in respect of an item of property, plant and equipment may be transferred directly to retained earnings when the asset is derecognised. This may involve transferring the whole of the surplus when the asset is retired or disposed of. However, some of the surplus may be transferred as the asset is used by an entity. In such a case, the amount of the surplus transferred would be the difference between depreciation based on the revalued carrying amount of the asset and depreciation based on the asset’s original cost. Transfers from revaluation surplus to retained earnings are not made through profit or loss. |

Although some standards require the balance of a reserve within equity to be recycled through profit or loss/surplus or deficit on disposal of the underlying asset (e.g. available for sale financial assets and foreign currency translation reserves), IAS 16 and PBE IPSAS 17 do not permit this. It is, however, permissible to transfer the balance to retained earnings/accumulated comprehensive revenue and expense when the asset is derecognised, but this transfer cannot be made by recycling the balance through profit or loss/surplus or deficit. Assuming the balance in the asset revaluation reserve is $100,000 when the underlying is sold, the journal entry for such a transfer would be as follows:

|

Common error 5 Recycling previous revaluation increments recognised in other comprehensive income/other comprehensive revenue and expense as a gain on disposal in profit or loss/surplus or deficit. |

Common error 6 – Excessive gains or losses on disposal of revalued assets

As noted in common error 2 above, revaluations are to be performed regularly for assets measured using the revaluation model so that there is no material difference between the carrying amount of the asset and its fair value at the reporting date.

Following on from this, and the concept in common error 5 that revaluation increments not be recycled through profit or loss/surplus or deficit when the asset is sold, we should not expect to see material amounts recognised in profit or loss/surplus or deficit as “gains on disposal of revalued PPE”. A common error often occurs where either:

-

There was an error in the valuation methodology used at the previous reporting date, or

-

Directors and preparers failed to consider whether the fair value had, in fact, changed at the previous reporting date (common error 2).

Unless there has been a significant change in circumstances relating to the asset since the previous revaluation, any large gain on disposal in profit/ surplus is usually a red flag that there could have been an error in a previous revaluation, or that there was insufficient consideration at the previous reporting date whether the fair value had indeed changed by a material amount.

|

Common error 6 Inadequate valuations resulting in excessive gains on disposal being recognised in profit or loss. |

Common error 7 – Changing accounting policy from the cost to the revaluation model and vice versa

Although not specifically addressed in IAS 16/PBE IPSAS 17, once you have chosen the cost model for a particular class of assets, as discussed in common error 1, it is possible, depending on the facts and circumstances, to change policies and revalue the class of assets, provided the new policy is then applied across all assets in the class. However, the opposite is not usually the case.

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors (PBE IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors) allows voluntary changes in accounting policies if they will result in more reliable/ faithfully representative and relevant information being provided in the financial statements.

|

An entity shall change an accounting policy only if the change:

IAS 8, paragraph 14 An entity shall change an accounting policy only if the change:

PBE IPSAS 3, paragraph 17 |

It is generally accepted that moving from the cost to the revaluation model provides users with more reliable/ faithfully representative and relevant information, particularly where historical costs of assets are outdated. However, the argument may not hold the other way around. It would be incorrect to assume that moving in both directions is always possible. Each case needs to be considered based on its specific facts and circumstances to ensure that both the reliable/ faithfully representative and relevant tests in IAS 8/PBE IPSAS 3 have been met.

Common error 7Changing from the revaluation to the cost model where reliable fair valuations are available or determinable. |

Common error 8 – Restating comparatives when changing from the cost to the revaluation model

Another common error occurs when an entity changes it measurement model (accounting policy) for a class of assets from the cost basis to the revaluation basis. Many preparers automatically assume that the usual retrospective restatement rules for voluntary changes in accounting policies apply. This is not correct.

When changing accounting policies because a new accounting standard has been issued, or because the requirements of an existing accounting standard have changed, we would usually restate comparatives (adjust retrospectively) unless we are told otherwise. If the new or amending standard is silent on what to do on transition, it means we need to restate comparatives (refer IAS 8, paragraph 19(b) and PBE IPSAS 3, paragraph 24(b)).

Paragraph 19(b) of IAS 8 (paragraph 24(b) of PBE IPSAS 3) also tells us to restate comparatives when we change accounting policies voluntarily, i.e. we must apply the change retrospectively.

|

Subject to paragraph 23:

IAS 8, paragraph 19

PBE IPSAS 3, paragraph 24 |

However, you can imagine that trying to obtain valuations at the comparative reporting date, and the opening balance sheet date for PPE items is likely to be a difficult exercise to perform, and likely to be biased so as to include the benefit of hindsight. As such, IAS 8/PBE IPSAS 3 make specific exemptions regarding retrospective restatement of comparatives where an entity decides to change its accounting policy from cost to revaluation. The say that we deal with the initial adjustments as a revaluation under IAS 16/PBE IPSAS 17 (see IAS 8, paragraph 17 and PBE IPSAS 3, paragraph 22), and they also clarify that the usual requirements for retrospective restatement and disclosures for voluntary changes in accounting policies in IAS 8, paragraphs 19-31/PBE IPSAS 3, paragraphs 24-36 do not apply.

|

The initial application of a policy to revalue assets in accordance with IAS 16 Property, Plant and Equipment or IAS 38 Intangible Assets is a change in an accounting policy to be dealt with as a revaluation in accordance with IAS 16 or IAS 38, rather than in accordance with this Standard. IAS 8, paragraph 17 IAS 8, paragraph 18

PBE IPSAS 3, paragraph 22 PBE IPSAS 3, paragraph 23 |

Common error 8Restating comparatives when changing from the cost to the revaluation model for a class of PPE. |

Next month:

Next month, our common errors series continues with common errors when depreciating PPE.

For more on the above, please contact your local BDO representative.