Common errors in accounting for impairment: Part 4- Not testing impairment at the correct unit of account

In this month’s common errors article, we continue our series on errors that can be made in applying the requirements of NZ IAS 36 Impairment of Assets, focusing on errors that can be made by not testing impairment at the correct ‘unit of account’.

When there is an indicator that an asset or group of assets is impaired, that asset (or group of assets) must be tested for impairment. Determining the level at which impairment testing takes place (the ‘unit of account’) involves significant judgement. However, there are clear ‘rules’ set out in NZ IAS 36 Impairment of Assets that, if not followed, can result in errors, such as:

- Testing impairment as part of a cash-generating unit (CGU), rather than as an individual asset

- Testing an asset for impairment at the individual asset level, rather than as part of a CGU

- Incorrectly identifying an entity’s CGUs, including CGUs being too large or too small

- Incorrectly determining a CGU at too high a level because the outputs from a CGU are consumed by other CGUs within the business

- Not consistently identifying CGUs from period to period for the same asset (or types of assets) where no change is justified

- Incomplete disclosure about changes to CGU composition.

It must also be recognised that special rules apply to the impairment testing of goodwill in respect of CGUs and groups of CGUs. The notion of testing impairment at a group of CGUs is specific to goodwill. Again, this can cause confusion in the correct application of NZ IAS 36.

A commonly used term in the application of NZ IAS 36 is ‘top down AND bottom up’ impairment testing. The ‘top down’ refers to the impairment testing of goodwill, the ‘bottom up’ refers to the impairment testing at an individual asset level, working up to a group of assets, then to a CGU.

The resulting common errors are discussed in more detail below.

Testing impairment as part of a cash-generating unit (CGU), rather than as an individual asset

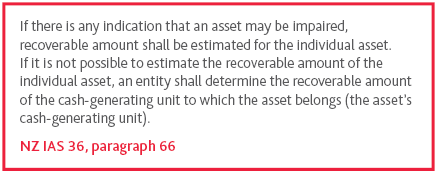

The basic requirement of NZ IAS 36 is that impairment testing should be performed at the individual asset level. If there is any indication that an asset may be impaired, that asset’s recoverable amount shall be determined.

Only where it is not possible to estimate the recoverable amount of the individual asset, can an entity switch to determine the recoverable amount of the CGU to which the asset belongs, i.e. this is the ‘bottom up’ approach, starting at the individual asset and working up to the CGU. The main reason for it not being possible to determine an individual asset’s recoverable amount is where ‘the asset does not generate cash inflows that are largely independent of those from other assets’ (NZ IAS 36, paragraph 67(e)).

One of the specified indicators of impairment in NZ IAS 36, paragraph 12(e), is ‘evidence is available of obsolescence or physical damage of an asset’. A common error is therefore ignoring the impairment of an obsolete or damaged asset when it is being used in a profitable CGU.

Example 1

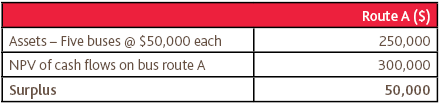

Company A operates a profitable bus route, bus route A. It uses five buses to service bus route A, each with a carrying value of $50,000. One bus is found to have major problems with its motor failing to pass the Council’s revised safety standards for buses. The bus is therefore not being used.

Company A tests for impairment at the CGU level, being the bus route, as follows:

Company A incorrectly concludes that there is no impairment charge to recognise because the recoverable amount of the CGU ($300,000) exceeds its carrying amount ($250,000).

The impairment test should have been performed at the asset level, with the bus that is not being used being impaired, and its recoverable amount likely to be determined using its fair value less costs of disposal (FVLCD).

Testing an asset for impairment at the individual asset level, rather than as part of a CGU

A mirror of Common Error 1 is the case where an asset’s recoverable amount cannot be determined, but is tested at the individual asset level.

Example 2

A mining company owns a private railway to support its mining activities. The private railway could be sold only for scrap value, and it does not generate cash inflows that are largely independent of the cash inflows from the other assets of the mine.

The mining company concludes that because the railway does not generate cash, it is impaired and it is written down to its scrap value (FVLCD).

This is a common error because it is not possible to estimate the recoverable amount of the private railway by itself because it does not generate its own cash flows (therefore value in use is nil). The mining company should therefore estimate the recoverable amount of the CGU to which the private railway belongs, i.e. the mine as a whole.

Incorrectly determining the CGU, including CGUs being too large or too small

.PNG.aspx?lang=en-NZ)

This basic definition can lead to two common errors as follows:

- CGUs being too small (the group of assets are not independent) - likely to result in impairment charges being excessive, or

- CGUs being too large - likely to result in impairment charges being understated.

When considering the use of CGUs in impairment testing under NZ IAS 36, confusion arises from the special rules on impairment testing for goodwill in paragraph 80 (to be discussed in next month’s Common Errors article) and the testing of individual assets (other than goodwill) for impairment. Impairment testing for goodwill introduces the concept of testing impairment at a level of a ‘group of CGUs’. This is a special rule for goodwill, and impairments of assets other than goodwill must be performed at the CGU level (not for a group of CGUs).

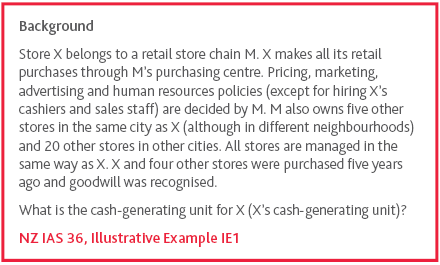

It is worth considering Illustrative Example, IE1, in NZ IAS 36.

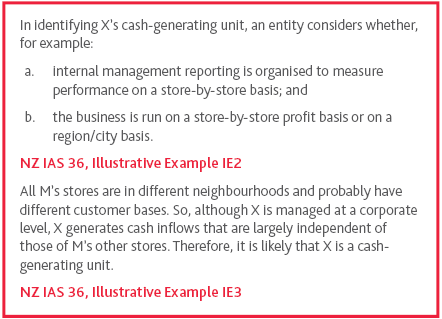

The analysis in IE2 – IE4 states:

CGU too small

If the impairment test is performed at a level such that the CGU is too small, it is likely that the entity will recognise excessive impairment charges. This can arise when the group of assets are not independent of other assets in generating cash, for example, where various services are bundled to derive revenue or income from a customer.

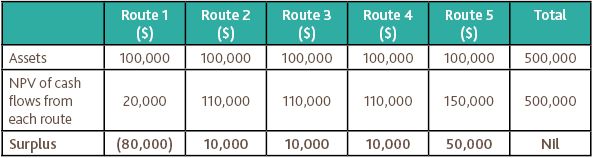

Example 3

A bus company provides services under a contract with a municipality that requires minimum service on each of five separate bus routes.

Assets devoted to each route, and the cash flows from each route, can be identified separately.

One of the routes operates at a significant loss.

The entity tests the assets associated with the loss making route for impairment and incorrectly recognises an impairment loss of $80,000. Although separate cash flows can be identified with each bus route, the requirement in the contract to provide a minimum service on each route means that the CGU (smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets) is the total of all bus routes because the cash flows for loss-making route 1 are dependent on the cash flows of the sum of all routes.

CGU too large

If the impairment test is performed at a level such that the CGU is too large, it is likely that the entity will understate its impairment charge. This can arise when the group of assets are independent of other assets in generating cash, and the entity wrongly combines cash flows instead of disaggregating them.

When CGUs are too large, this common error typically results in:

- Cash flows from profitable operations supporting the carrying amounts of assets from unprofitable operations, or

- Cash flows from fully depreciated assets, or assets with low carrying amounts on the balance sheet, supporting the carrying amount of significant assets that generate minimal cash flows.

Example 4

A bus company provides services under contract with a municipality.

It operates five key arterial routes. Assets devoted to each route, and the cash flows from each route, can be identified separately.

One of the routes operates at a significant loss.

Because the entity has the option to curtail any one bus route, the lowest level of identifiable cash inflows that are largely independent of the cash inflows from other assets (or groups of assets), is the cash inflows generated by an individual route. For the purpose of impairment testing, it would be therefore wrong to aggregate all five routes into a single CGU.

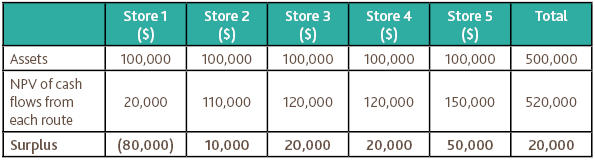

Example 5

A retailer operates five separate stores in a particular city.

The assets which are dedicated to each store, and the cash flows from each store, can be identified separately.

One of the stores operates at a significant loss.

For the purpose of impairment testing, it would be wrong to aggregate all five stores into a single CGU. The assets associated with the loss making store should be tested for impairment against the cash flows generated from that store.

The entity performs the impairment test at the group of CGUs (each store is a CGU and records no impairment loss, having determined the recoverable amount to be $520,000 compared to a carrying amount of $500,000).

Application of NZ IAS 36 would require the recording of an impairment loss of $80,000 for Store 1.

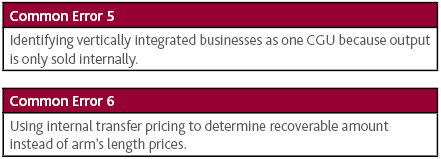

Incorrectly determining a CGU at too high a level because the outputs from a CGU are consumed by other CGUs within the business

Another common error arises where an entity is a vertically integrated business, and it incorrectly views the vertically integrated operation as a single CGU. If the operation is capable of producing outputs that can be consumed by third parties, this is likely to represent a separate CGU, regardless of whether all of its output is consumed internally.

Examples of such situations might include:

- Vertical integration of producing oil wells with a refining operation - most likely the production activity is a separate CGU from the refining operation

- A refining operation and a retail chain of service stations - most likely these are two separate CGUs

- A package tour operator, operating aircraft and hotels

- A steel producer operating coal mines to provide material to be consumed in its steel furnaces, and

- A retail operation having its own farms or manufacturing facilities.

Example 6

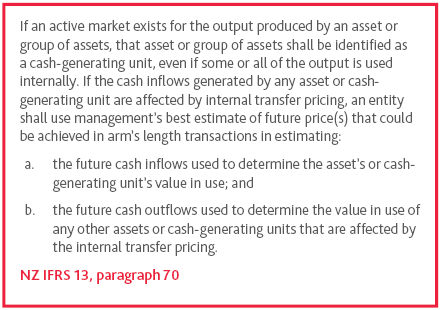

Company B is a steel manufacturer that operates one steel mill and also owns two coal mines, one produces coking coal, the other thermal coal. All of the mines’ output is consumed in the steel mill.

If Company B determined the CGU to be the steel business as a whole, it would result in Company B incorrectly recognising no impairment charge, rather than the impairment charge of $29 million, using arm’s length prices, required by NZ IAS 36, paragraph 70.

Similarly, if Company B determined that the steel mill should be impaired, and an impairment loss of $11 million was recognised based on internal transfer pricing, this would not comply with NZ IAS 36, paragraph 70.

This example illustrates the need to determine a CGU’s recoverable amount using arm’s length prices, rather than internal transfer prices that can be used to ‘share’ profits around the entity’s various CGUs.

Not consistently identifying CGUs from period to period for the same asset (or types of assets) where no change is justified

As described above, there is a degree of professional judgement involved in both determining:

- Whether an asset should be tested for impairment at the asset level or CGU level, and

- The allocation of assets to CGUs and the determination of what represents a CGU.

It is essential that these judgements are applied consistently, and if not, that fact is disclosed. There is a tendency for allocation of assets to drift towards those CGUs that are generating the most cash flows. This can arise as business models and markets evolve over time.

Example 7

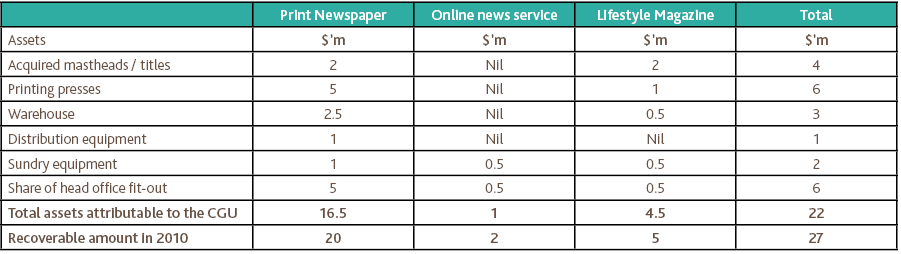

Media Co operates three CGUs, namely a hard print newspaper, an online news subscription website, and a monthly lifestyle magazine.

The print business is more asset intensive, involving printing presses, warehousing and distribution equipment. Each business has its own sales and marketing teams, as well as a standalone editorial team.

Performance of the CGUs in 2010 was as follows.

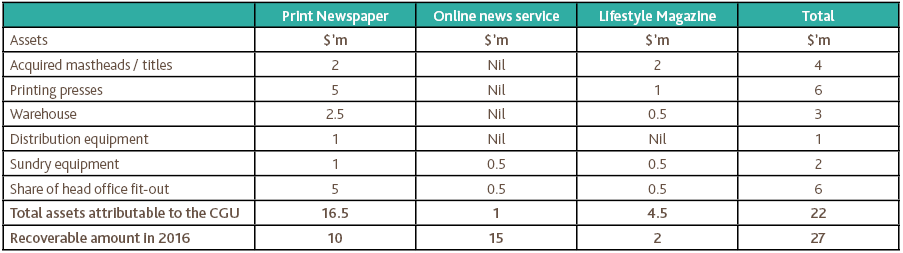

The nature of the media industry has changed significantly over the past six years, with a significant increase in online business, and a significant retraction in the print business (both newspapers and magazines). As a result, the workforce has been rationalised to one back office, reducing the workforce by 60%. The organisation still produces financial results for each of the three businesses based on the achieved sales and advertising revenue.

Had a consistent method of allocating assets been applied to the CGUs, the following recoverable amounts shown in 2016 would be:

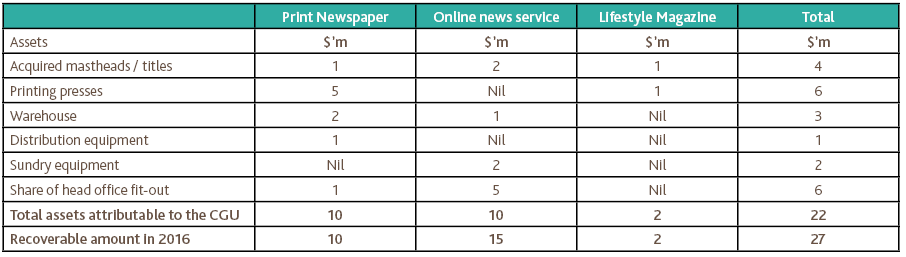

Media Co proposes to re-determine the allocation of assets as follows:

A common error would be to conclude, based on this inconsistent allocation of assets to the three CGUs, that there is no impairment charge to recognise. Based on the consistent allocation of assets, an impairment charge of $9 million would be recognised ($6.5 million for print newspaper and $2.5 million for magazines).

As an alternative, Media Co now determines that it only has one CGU, being its media business, and determines that there is no impairment charge as the recoverable amount of $27 million exceeds the carrying value the CGU of $22 million.

Incomplete disclosure about changes to CGU composition

Where the composition of a CGU has changed since the previous reporting period (e.g. certain assets moved from one CGU to another), and an impairment loss has been recognised or reversed for that CGU during the current reporting period, all the detailed impairment disclosures in NZ IAS 36, paragraph 130 must be included by Tier 1 reporters.

Next month

In next month’s article we look at common errors made when testing goodwill for impairment, including ‘the top down’ issue when not applying the appropriate unit of account.

For more on the above, please contact your local BDO representative