Convertible notes - Are you accounting for these correctly (Part 9)?

In the current economic climate, we continue to see different types of convertible note arrangements, typically entered into by companies needing to offer attractive returns in order to obtain funds from lenders and investors.Over the past few months we have been looking at some practical aspects regarding accounting for convertible notes, including:

- An overview of the requirements (in the April 2018 edition of Accounting Alert)

- A detailed example of a convertible note classified as a compound financial instrument (in the May 2018 edition of Accounting Alert)

- A detailed example of a convertible note with an embedded derivative liability (in the mid-June edition of Accounting Alert)

- Common scenarios encountered in practice where conversion features either meet or fail equity classification (in the July 2018 edition of Accounting Alert)

- A detailed example of a convertible note converting into a variable number of shares based on the issuer’s share price at conversion date (in the August 2018 edition of Accounting Alert).

- A detailed example of a convertible note issued in a currency other than the issuer’s functional currency (in the September 2018 edition of Accounting Alert).

- A detailed example of a convertible note with a feature that allows the issuer to repay (call) the note early (in the October 2018 edition of Accounting Alert).

- A detailed example of a convertible note with an early repurchase option (in the November 2018 edition of Accounting Alert).

This month we look at a detailed example of a mandatorily convertible note.

SummaryIn some circumstances, convertible notes mandatorily convert after a fixed period of time, but pay a contractual coupon up to the point of conversion. Provided that the conversion feature results in the conversion of a fixed functional currency amount of the notes into a fixed number of shares, the conversion feature of the mandatorily convertible component is classified as equity.

The liability component consists only of the cash flows associated with the contractually required coupon payments. This treats the note effectively as prepaid equity and results in significantly more equity upon initial recognition than would be the case with a conventional convertible note with a conversion option. Interest expense recognised at the effective interest rate would also be significantly lower than a conventional convertible note.

Example: Mandatorily convertible note

ABC Limited issues a convertible note with a face value of $1,000,000.

The note matures three years from its date of issue and pays a 10% annual coupon.

On maturity, the note mandatorily converts into 1,000,000 ordinary shares of ABC Limited.

The market interest rate for a note without a conversion feature would have been 12% at the date of issue.

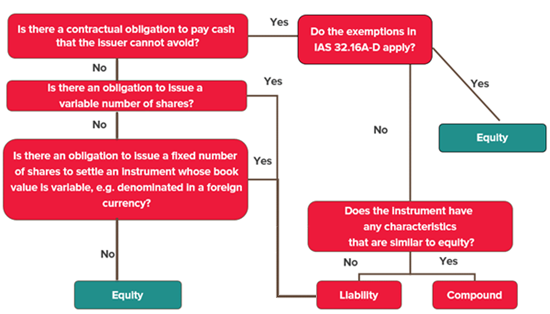

Analysis – Entire note

Using the above flowchart for the entire instrument, it is assessed as being a compound financial instrument because:

- ABC Limited (the issuer) has a contractual obligation to pay cash that it cannot avoid (i.e. the annual cash coupon)

- The exceptions in paragraphs IAS 32.16A-D do not apply; and

- The instrument has characteristics that are similar to equity (i.e. it contains an option to be converted into equity instruments).

Analysis – conversion feature

The mandatory conversion feature is then assessed on a stand-alone basis. Starting with the box at the top left hand side of the diagram:

- There is no contractual obligation to pay cash that ABC Limited cannot avoid. The equity conversion feature can only be settled through the issue of equity shares in ABC Limited, otherwise it will simply expire unexercised.

- There is no obligation to issue a variable number of shares. The note mandatorily converts into 1,000,000 shares of ABC Limited on maturity.

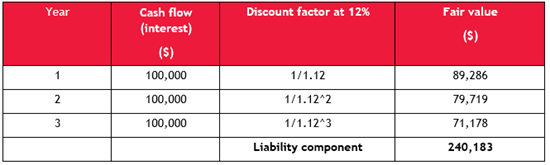

The fair value of the liability component is calculated as follows:

The residual equity component is calculated in the table below:

The accounting for a mandatorily convertible note therefore results in significantly more equity than a conventional convertible note with a convertible option and effectively treats the note as prepaid equity. Interest expense recognised at the effective interest rate is significantly lower than a conventional convertible note because it is only calculated based on a substantially lower liability balance.

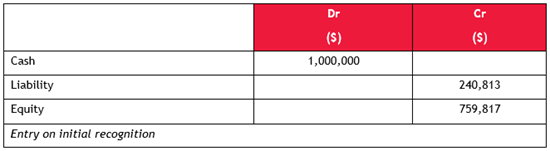

Journal entries

The journal entry recognised by ABC Limited on initial recognition of the mandatorily convertible note is:

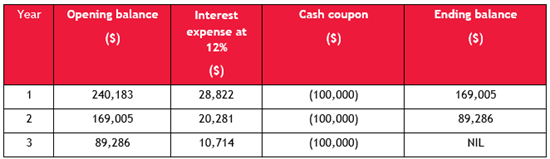

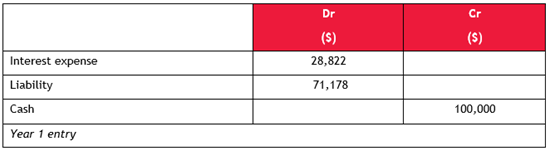

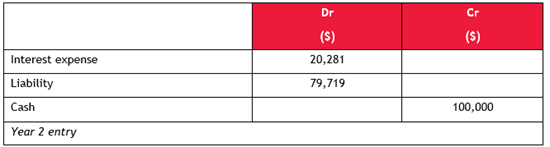

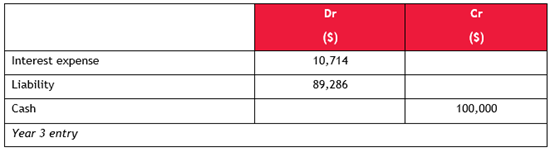

The liability component will then amortise over the three-year life of the note, from inception until maturity, as follows:

The journal entries recognised in years 1, 2 and 3, respectively, are as follows:

For more on the above, please contact your local BDO representative.