Common errors in accounting for impairment: Part 5 – Testing goodwill for impairment

Background

The nature of goodwill leads to a number of complex rules as to how it should be treated for impairment testing. This in turn leads to a number of potential common errors that could lead to a material misstatement.

Goodwill acquired in a business combination does not in itself generate cash flows, otherwise it would most likely have been classified as an identifiable intangible asset. In theory, goodwill represents synergies and an assembled workforce that only generates cash flows in association with other assets. It is not amortised but is subject to an annual impairment test, and must, in addition to the annual test, be tested for impairment if there has been an impairment trigger.

There are special impairment rules around allocating goodwill to cash generating units (CGUs) which are designed to simplify impairment testing for goodwill, and to minimise the need to change reporting information. Unfortunately these rules can cause errors to arise, both when testing goodwill for impairment, and when testing other assets for impairment.

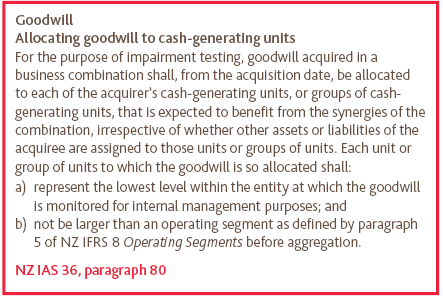

Allocating goodwill to cash-generating units

The principles for allocating goodwill acquired in a business combination to CGUs or groups of CGUs for the purpose of impairment testing are described in NZ IAS 36 Impairment of Assets, paragraph 80.

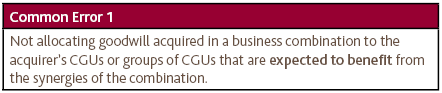

Allocation based on expected synergies

The first principle in paragraph 80 is that goodwill acquired in a business combination must be allocated to CGUs or groups of CGUs that are expected to benefit from the synergies of the combination.

Example 1

Professional Practice Firm has a tax division, assurance division and a consulting division, with a centralised back office to support administration, HR and marketing. Each division represents a CGU.

Professional Practice Firm acquires Small Firm, resulting in goodwill of $2 million. The acquired firm’s revenue derives 90% from the tax division and 10% from assurance, with no consulting division. Part of the business rationale for the acquisition of Small Firm is to sell additional assurance services and consulting services to Small Firm’s ‘tax’ client base.

Professional Practice Firm allocates all of the goodwill to the tax GCU.

This is an error as some of the goodwill should have been allocated to both the assurance CGU, and the consulting CGU.

Allocation to lowest level at which goodwill is monitored for internal management purposes

The second principle in paragraph 80 is that goodwill must be allocated to CGUs or groups of CGUs that represent the lowest level within the entity/group at which goodwill is monitored by internal management.

Example 2

Bus Company A acquires Small City Bus Co, a local company (business) in Small City. Bus Company A had never previously operated in Small City.

Small City Bus Co has five bus routes. Each bus route is likely to be a separate CGU, but for the purpose of management reporting, the performance of the acquisition is measured based on the profitability from the whole operation in Small City.

It would therefore be reasonable to test goodwill for impairment at the Small City Bus Co level, i.e. all five bus routes on an aggregated basis.

Example 3

Bus Company B acquires Small City Bus Co, a local bus company in Small City.

Bus Company B has an existing operation in Small City, running ten bus routes.

Small City Bus Co operates five bus routes. Each bus route is likely to be a separate CGU, but for the purpose of management reporting, the performance of the acquisition is measured based on the profitability from the whole operation in Small City.

It would therefore be reasonable to test goodwill for impairment at the Small City level, i.e. all 15 bus routes on an aggregated basis.

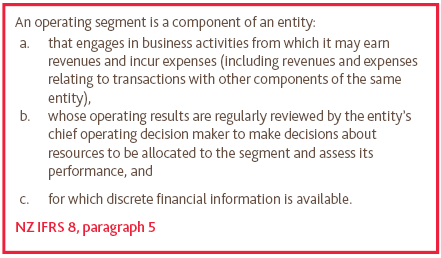

Allocation not higher than an operating segment, before aggregation

Lastly, paragraph 80 requires that each CGU or group of CGUs to which goodwill is allocated cannot be larger than an operating segment as defined in paragraph 5 of NZ IFRS 8 Operating Segments.

Points worth noting:

- An operating segment (before aggregation) is typically represented by ‘a column’ in management accounts presented to the chief operating decision maker (CODM). If, for example, operating reports/management accounts presented to the CODM of a chain of shoe stores includes separate columns for each store, each store would typically be a separate CGU, and also an operating segment (before aggregation). While all shoe stores may share similar economic characteristics, and therefore be aggregated when presenting segment disclosures in the financial statements, goodwill will need to be allocated to each shoe store when performing the annual impairment test.

- This requirement applies equally to private companies that are not required to present the segment disclosures in NZ IFRS 8. This means that you would need to first identify all your operating segments (before aggregation) prior to allocating goodwill.

Example 4

Bus Company C, historically based in Wellington, has created a national business through acquisitions and now operates in Auckland, Christchurch and the Hawkes Bay. For the purpose of reporting under NZ IFRS 8, it aggregates all of its operating segments because they share similar economic characteristics.

Bus Company C tests goodwill for impairment at the New Zealand level.

This is an error because each region is likely to meet the definition of an operating segment.

Example 5

Bus Company D, historically based in Wellington, has created a national business through acquisitions and now operates in Auckland, Christchurch and the Hawkes Bay. Bus Company D is not required to report under NZ IFRS 8 Segment Reporting.

Bus Company D tests goodwill for impairment at the New Zealand level.

Again, this is an error because each region is likely to meet the definition of an operating segment. The requirement in NZ IAS 36 to test at a level no larger than an operating segment applies, regardless of whether the entity is required to report under NZ IFRS 8.

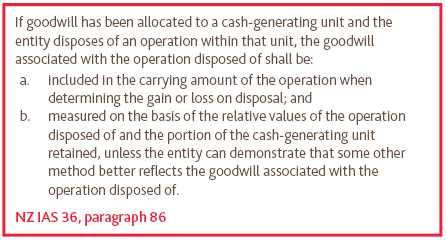

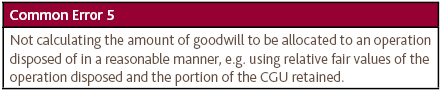

Disposals

When an entity disposes of part of a business operation making up a CGU, paragraph 86 requires that goodwill associated with the operation disposed must be measured and allocated to the carrying amount of net assets sold. This will result in a reduction in the gain, or increase in loss, on disposal of the operation.

Example 6

An entity sells an operation for $100,000 that was part of a CGU to which goodwill has been allocated. The goodwill allocated to the unit cannot be identified or associated with an asset group at a level lower than that CGU, except arbitrarily. The recoverable amount of the portion of the CGU retained is $300,000.

Scenario A

Entity attributes no goodwill to the disposed of operation.

This is a common error, resulting in an overstatement of the gain on disposal.

25% of the goodwill ($100,000/$400,000 based on relative fair values of operations disposed of and portion of CGU retained) should have been allocated to the disposal group.

Scenario B

Entity attributes 10% of the goodwill to the operation disposed of.

This is also a common error, resulting in an overstatement of the gain on disposal.

25% of the goodwill ($100,000/$400,000) should have been allocated to the disposal group.

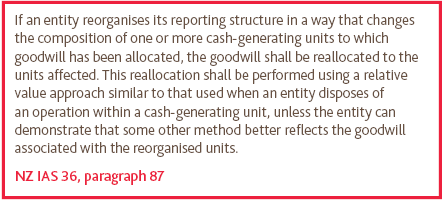

Reorganisations

NZ IAS 36, paragraph 87 also includes requirements for reallocation of goodwill when an entity reorganises its reporting structure so that there is a change in the composition of CGUs to which goodwill has been allocated.

Example 7

Historically, Bus Company E operates 20 bus routes across various cities in New Zealand. The operation comprises 20 CGUs and has been monitored on a city basis.

In a reorganisation, the operation is now to be operated as three separate divisions (groups of CGUs):

- Urban (ten CGUs)

- Rural (six CGUs), and

- A separate education transport unit (school buses) (four CGUs).

This new structure reflects Bus Company E’s national reporting structure, and no financial reporting will be produced based on city results.

Bus Company E does not allocate goodwill to these three new units. This is a common error as the three new units have no goodwill allocated.

Example 8

Goodwill had previously been allocated to CGU A. The goodwill allocated to CGU A cannot be identified or associated with an asset group at a level lower than CGU A, except arbitrarily.

CGU A is to be divided and integrated into three other CGUs: B, C and D.

The entity allocates all the goodwill to CGU B.

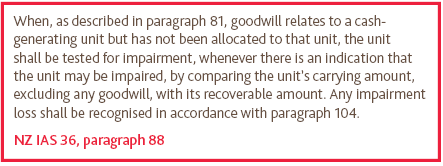

Bottom up - top down assessment

As described in last month’s Accounting Alert article, a common cause of errors is preparers not distinguishing between the special rules that apply to testing goodwill in respect of allocating to a CGU or a group of CGUs, and the basic requirement to test assets, other than goodwill, for impairment.

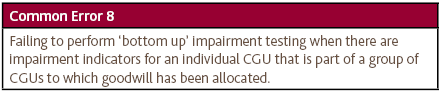

Example 9

Big Co has three operating divisions: Division A, Division B and Division C, which are all a group of CGUs. Division A sells Samsung Galaxy 7s.

Big Co is unable to allocate goodwill to each division (CGU), except arbitrarily. Goodwill is therefore allocated to the group of CGUs (Divisions A, B and C) and impairment testing performed at the level of the A-B-C group.

During the year, iPhone 7 was released and Division A will need to heavily discount its large stocks of Samsung Galaxy 7s, resulting in reduced expected sales in Division A.

Big Co continues to test impairment only at the level of the A-B-C group. This is a common error because Big Co has failed to comply with the requirement in paragraph 88 to perform ‘bottom up’ impairment testing.

Timing of impairment tests

A goodwill impairment test must be performed at least once a year. It can be performed at any time during the year, but at the same time each year.

Example 10

Entity F has a 30 June year end.

Entity F only tests goodwill for impairment at year end because it assumes that testing must take place at the end of the reporting period. This places significant stress on the reporting process and risks delays in producing its annual financial statements.

This is another common error because impairment testing can be performed at any time during an annual period, provided the test is performed at the same time every year.

Example 11

Entity G has a 30 June year end.

In 2016, it tested its goodwill for impairment in May 2016. It proposes to update the impairment model in July 2016, in order to meet the requirement for impairment testing for 2017.

This is a common error because impairment testing must be performed at the same time every year. Changing the timing of impairment testing is not permitted in NZ IAS 36.

Example 12

Entity H has a 30 June year end.

It acquires a business in May 2016, and does not test this goodwill for impairment for its 30 June 2016 financial report.

This is a common error because goodwill must be tested for impairment even if it arises from an acquisition in the year.

Example 13

Entity I has a 30 June year end. It tests its goodwill for impairment in May each year.

Entity I performed its impairment test in May 2016 and concluded there was no impairment because its market capitalisation was $200 million at 31 May 2016, compared with a net asset position of $180 million.

At 30 June 2016, Entity I’s market capitalisation had fallen to $120 million. It did not reperform its impairment testing at 30 June 2016.

This is a common error because goodwill must be tested for impairment when there is an impairment indicator, regardless if it has been tested earlier as part of the annual impairment testing cycle.

Example 14

Entity J A has a 30 June year end and has half-year reporting obligations at 31 December each year.

It tests its goodwill for impairment in May each year.

Entity J performed its impairment test in May 2016 and concluded there was no impairment because its market capitalisation was $200 million at 31 May 2016 compared with a net asset position of $180 million.

At 31 December 2016, Entity J’s market capitalisation had fallen to $120 million. It did not perform its impairment testing, arguing that goodwill was not due for testing until May 2017.

This is a common error because goodwill must be tested for impairment when an impairment event has occurred, regardless if it will be tested later as part of the annual impairment testing cycle.

Testing individual assets for impairment first

Where there are impairment indicators for assets in a CGU, other than goodwill, paragraph 98 requires that these assets are tested for impairment, and written down if necessary, prior to conducting the impairment test on the whole CGU, or group of CGUs.

Example 15

Bus Company K runs a bus route which is operated using three buses.

The carrying value of the buses is $750,000 ($250,000 each). The bus route represents a CGU to which $1 million of goodwill has been allocated.

One of the buses is not performing to required standards on safety and omissions and is idol. It is estimated the bus will be sold for $50,000 and that a new replacement bus will cost $300,000.

The recoverable amount of the CGU, taking into account the need to replace the one bus, is $1.6 million. Assuming the carrying amount of the CGU is $1.75 million, comprising goodwill of $1 million and property, plant and equipment (PPE) of $750,000, Bus Company K recognises an impairment loss of $150,000 against goodwill.

This is a common error and an impairment loss of $200,000 should have first been recognised in respect of the underperforming bus (i.e. $250,000 carrying value less $50,000 recoverable amount). Therefore the impairment test in respect of goodwill should have been $1.6 million compared to a CGU with a value of $1.55 million (goodwill of $1 million plus PPE of $550,000).

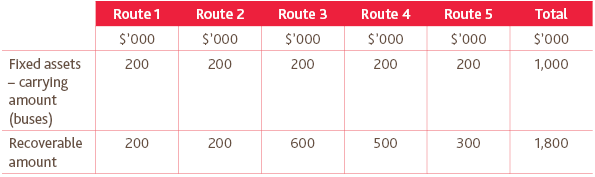

Example 16

Bus Company L operates five bus routes (each represents a separate CGU). Goodwill of $1 million has not been allocated to individual routes.

The table above shows that none of the buses are impaired because their recoverable amounts exceed fair value.

The total carrying amount of assets for impairment testing of the combined group is $2 million, being $1 million goodwill plus $1 million for the buses.

Bus Company L recognises an impairment loss of $200,000 ($2 million -$1.8 million) for the group and allocates it against each of the CGUs assets (buses).

This is a common error. The $200,000 impairment loss should have been recognised against goodwill and not the fixed assets as none of the fixed assets are impaired.

Summary

This concludes our series of common articles on impairment of non-financial assets.

You can access all the previous common error impairment articles on our website:

Part 1 – Common errors in accounting for impairment (July 2016)

Part 2a – Common errors in accounting for impairment (August 2016)

Part 2b – Common errors in accounting for impairment (September 2016)

Part 2c – Errors in determining the discount rate (November 2016)

Part 3 – Errors when determining ‘fair value less costs of disposal’ (December 2016)

Part 4 – Not testing impairment at the correct unit of account (January 2017)

For more on the above, please contact your local BDO representative.